OECD Economic Outlook 69 - Biblioteca Hegoa

OECD Economic Outlook 69 - Biblioteca Hegoa

OECD Economic Outlook 69 - Biblioteca Hegoa

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

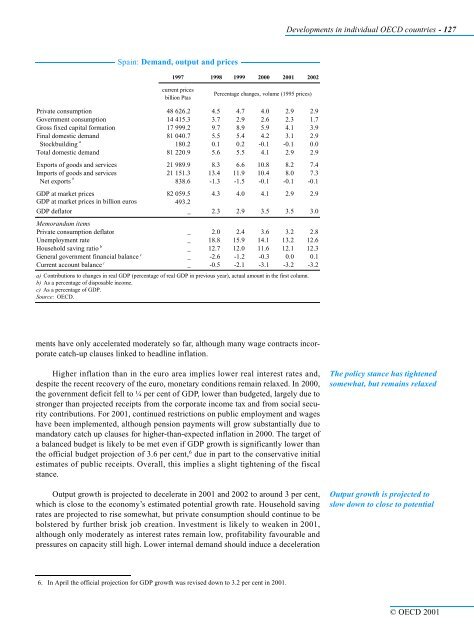

Spain: Demand, output and prices<br />

1997 1998 1999 2000 2001 2002<br />

current prices<br />

billion Ptas<br />

Percentage changes, volume (1995 prices)<br />

Private consumption 48 626.2 4.5 4.7 4.0 2.9 2.9<br />

Government consumption 14 415.3 3.7 2.9 2.6 2.3 1.7<br />

Gross fixed capital formation 17 999.2 9.7 8.9 5.9 4.1 3.9<br />

Final domestic demand 81 040.7 5.5 5.4 4.2 3.1 2.9<br />

a<br />

Stockbuilding 180.2 0.1 0.2 -0.1 -0.1 0.0<br />

Total domestic demand 81 220.9 5.6 5.5 4.1 2.9 2.9<br />

Exports of goods and services 21 989.9 8.3 6.6 10.8 8.2 7.4<br />

Imports of goods and services 21 151.3 13.4 11.9 10.4 8.0 7.3<br />

a<br />

Net exports 838.6 -1.3 -1.5 -0.1 -0.1 -0.1<br />

GDP at market prices 82 059.5 4.3 4.0 4.1 2.9 2.9<br />

GDPatmarketpricesinbillioneuros 493.2<br />

GDP deflator<br />

Memorandum items<br />

_ 2.3 2.9 3.5 3.5 3.0<br />

Private consumption deflator _ 2.0 2.4 3.6 3.2 2.8<br />

Unemployment rate _ 18.8 15.9 14.1 13.2 12.6<br />

b<br />

Household saving ratio _ 12.7 12.0 11.6 12.1 12.3<br />

c<br />

General government financial balance _ -2.6 -1.2 -0.3 0.0 0.1<br />

c<br />

Current account balance _ -0.5 -2.1 -3.1 -3.2 -3.2<br />

a) Contributions to changes in real GDP (percentage of real GDP in previous year), actual amount in the first column.<br />

b) As a percentage of disposable income.<br />

c) As a percentage of GDP.<br />

Source: <strong>OECD</strong>.<br />

ments have only accelerated moderately so far, although many wage contracts incorporate<br />

catch-up clauses linked to headline inflation.<br />

Higher inflation than in the euro area implies lower real interest rates and,<br />

despite the recent recovery of the euro, monetary conditions remain relaxed. In 2000,<br />

the government deficit fell to ¼ per cent of GDP, lower than budgeted, largely due to<br />

stronger than projected receipts from the corporate income tax and from social security<br />

contributions. For 2001, continued restrictions on public employment and wages<br />

have been implemented, although pension payments will grow substantially due to<br />

mandatory catch up clauses for higher-than-expected inflation in 2000. The target of<br />

a balanced budget is likely to be met even if GDP growth is significantly lower than<br />

the official budget projection of 3.6 per cent, 6 due in part to the conservative initial<br />

estimates of public receipts. Overall, this implies a slight tightening of the fiscal<br />

stance.<br />

Output growth is projected to decelerate in 2001 and 2002 to around 3 per cent,<br />

which is close to the economy’s estimated potential growth rate. Household saving<br />

rates are projected to rise somewhat, but private consumption should continue to be<br />

bolstered by further brisk job creation. Investment is likely to weaken in 2001,<br />

although only moderately as interest rates remain low, profitability favourable and<br />

pressures on capacity still high. Lower internal demand should induce a deceleration<br />

6. In April the official projection for GDP growth was revised down to 3.2 per cent in 2001.<br />

Developments in individual <strong>OECD</strong> countries - 127<br />

The policy stance has tightened<br />

somewhat, but remains relaxed<br />

Output growth is projected to<br />

slow down to close to potential<br />

© <strong>OECD</strong> 2001