GAMMON INDIA LIMITED

GAMMON INDIA LIMITED

GAMMON INDIA LIMITED

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

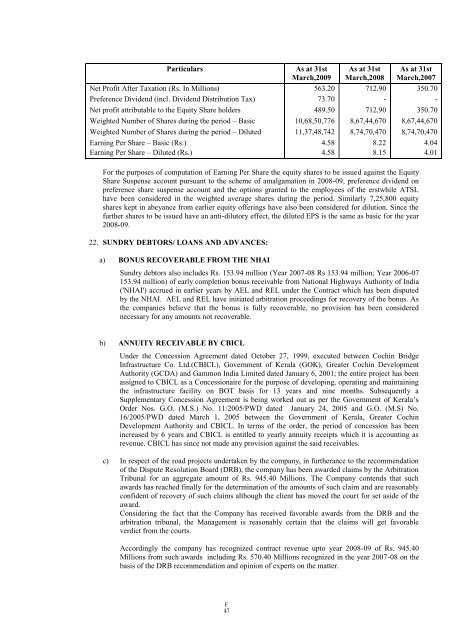

Particulars As at 31st<br />

March,2009<br />

As at 31st<br />

March,2008<br />

As at 31st<br />

March,2007<br />

Net Profit After Taxation (Rs. In Millions) 563.20 712.90 350.70<br />

Preference Dividend (incl. Dividend Distribution Tax) 73.70 - -<br />

Net profit attributable to the Equity Share holders 489.50 712.90 350.70<br />

Weighted Number of Shares during the period – Basic 10,68,50,776 8,67,44,670 8,67,44,670<br />

Weighted Number of Shares during the period – Diluted 11,37,48,742 8,74,70,470 8,74,70,470<br />

Earning Per Share – Basic (Rs.) 4.58 8.22 4.04<br />

Earning Per Share – Diluted (Rs.) 4.58 8.15 4.01<br />

For the purposes of computation of Earning Per Share the equity shares to be issued against the Equity<br />

Share Suspense account pursuant to the scheme of amalgamation in 2008-09, preference dividend on<br />

preference share suspense account and the options granted to the employees of the erstwhile ATSL<br />

have been considered in the weighted average shares during the period. Similarly 7,25,800 equity<br />

shares kept in abeyance from earlier equity offerings have also been considered for dilution. Since the<br />

further shares to be issued have an anti-dilutory effect, the diluted EPS is the same as basic for the year<br />

2008-09.<br />

22. SUNDRY DEBTORS/ LOANS AND ADVANCES:<br />

a) BONUS RECOVERABLE FROM THE NHAI<br />

Sundry debtors also includes Rs. 153.94 million (Year 2007-08 Rs 153.94 million; Year 2006-07<br />

153.94 million) of early completion bonus receivable from National Highways Authority of India<br />

('NHAI') accrued in earlier years by AEL and REL under the Contract which has been disputed<br />

by the NHAI. AEL and REL have initiated arbitration proceedings for recovery of the bonus. As<br />

the companies believe that the bonus is fully recoverable, no provision has been considered<br />

necessary for any amounts not recoverable.<br />

b) ANNUITY RECEIVABLE BY CBICL<br />

Under the Concession Agreement dated October 27, 1999, executed between Cochin Bridge<br />

Infrastructure Co. Ltd.(CBICL), Government of Kerala (GOK), Greater Cochin Development<br />

Authority (GCDA) and Gammon India Limited dated January 6, 2001; the entire project has been<br />

assigned to CBICL as a Concessionaire for the purpose of developing, operating and maintaining<br />

the infrastructure facility on BOT basis for 13 years and nine months. Subsequently a<br />

Supplementary Concession Agreement is being worked out as per the Government of Kerala‟s<br />

Order Nos. G.O. (M.S.) No. 11/2005/PWD dated January 24, 2005 and G.O. (M.S) No.<br />

16/2005/PWD dated March 1, 2005 between the Government of Kerala, Greater Cochin<br />

Development Authority and CBICL. In terms of the order, the period of concession has been<br />

increased by 6 years and CBICL is entitled to yearly annuity receipts which it is accounting as<br />

revenue. CBICL has since not made any provision against the said receivables.<br />

c) In respect of the road projects undertaken by the company, in furtherance to the recommendation<br />

of the Dispute Resolution Board (DRB), the company has been awarded claims by the Arbitration<br />

Tribunal for an aggregate amount of Rs. 945.40 Millions. The Company contends that such<br />

awards has reached finally for the determination of the amounts of such claim and are reasonably<br />

confident of recovery of such claims although the client has moved the court for set aside of the<br />

award.<br />

Considering the fact that the Company has received favorable awards from the DRB and the<br />

arbitration tribunal, the Management is reasonably certain that the claims will get favorable<br />

verdict from the courts.<br />

Accordingly the company has recognized contract revenue upto year 2008-09 of Rs. 945.40<br />

Millions from such awards including Rs. 570.40 Millions recognized in the year 2007-08 on the<br />

basis of the DRB recommendation and opinion of experts on the matter.<br />

F<br />

47