Update on Merger with Polymetals - Notice of Meeting

Update on Merger with Polymetals - Notice of Meeting

Update on Merger with Polymetals - Notice of Meeting

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Gearing<br />

Before WACC can be determined, the proporti<strong>on</strong> <strong>of</strong> funding provided by debt and equity (i.e., gearing<br />

ratio) must be determined. The gearing ratio adopted should represent the level <strong>of</strong> debt that the asset<br />

can reas<strong>on</strong>ably sustain (i.e., the higher the expected volatility <strong>of</strong> cash flows, the lower the debt levels<br />

which can be supported). The optimum level <strong>of</strong> gearing will differentiate between assets and will include:<br />

• the variability in earnings streams;<br />

• working capital requirements;<br />

• the level <strong>of</strong> investment in tangible assets; and<br />

• the nature and risk pr<strong>of</strong>ile <strong>of</strong> the tangible assets.<br />

As described earlier, we understand the capital <strong>of</strong> structure <strong>of</strong> the Merged Entity to be made up <strong>of</strong><br />

approximately 65% debt and 35% equity. We have used a cost <strong>of</strong> debt in the range <strong>of</strong> 7.50% to 8.50% based<br />

<strong>on</strong> the indicative debt funding <strong>of</strong>fers received by SXG and PLY.<br />

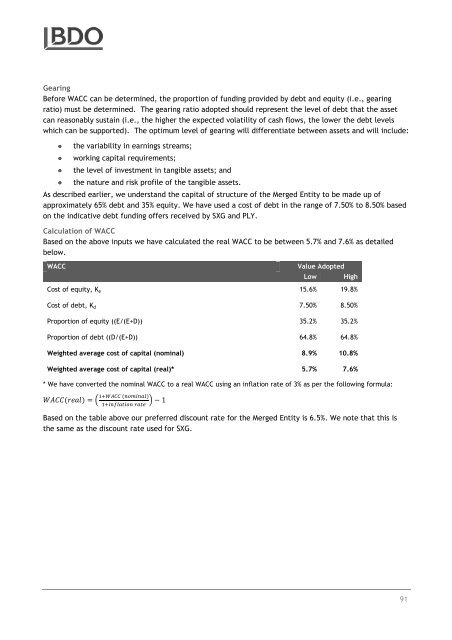

Calculati<strong>on</strong> <strong>of</strong> WACC<br />

Based <strong>on</strong> the above inputs we have calculated the real WACC to be between 5.7% and 7.6% as detailed<br />

below.<br />

WACC<br />

Value Adopted<br />

Low<br />

High<br />

Cost <strong>of</strong> equity, K e 15.6% 19.8%<br />

Cost <strong>of</strong> debt, K d 7.50% 8.50%<br />

Proporti<strong>on</strong> <strong>of</strong> equity ((E/(E+D)) 35.2% 35.2%<br />

Proporti<strong>on</strong> <strong>of</strong> debt ((D/(E+D)) 64.8% 64.8%<br />

Weighted average cost <strong>of</strong> capital (nominal) 8.9% 10.8%<br />

Weighted average cost <strong>of</strong> capital (real)* 5.7% 7.6%<br />

* We have c<strong>on</strong>verted the nominal WACC to a real WACC using an inflati<strong>on</strong> rate <strong>of</strong> 3% as per the following formula:<br />

()<br />

( ) = − 1<br />

<br />

Based <strong>on</strong> the table above our preferred discount rate for the Merged Entity is 6.5%. We note that this is<br />

the same as the discount rate used for SXG.<br />

91