NICKEL109Nickel prices were adversely affected by the global economic recession in 2008 <strong>and</strong> 2009. In March 2009, the LondonMetal Exchange (LME) cash mean for 99.8%-pure nickel bottomed out at $9,693 per metric ton after a 22-monthdecline. The cash price gradually recovered <strong>and</strong> returned to above $19,000 per metric ton in March 2010. Theaverage monthly LME cash price for November 2010 was $22,905 per ton. In July, a multinational joint venture beganmining the large Ambatovy laterite deposit in east-central Madagascar. The ore was being slurried <strong>and</strong> piped to theventure’s pressure leach plant <strong>and</strong> refinery near Toamasina. The Toamasina complex was designed to produce60,000 tons per year of nickel <strong>and</strong> was expected to be in the early stages of commissioning at the beginning of <strong>2011</strong>.New mines also were being developed at several locations in Brazil, Southeast Asia, <strong>and</strong> the Pacific. In August, the$4.5 billion Goro laterite project in New Caledonia began producing a nickel-cobalt intermediate for export. Goro wasscheduled to reach full production in 2013 with a production capacity of 60,000 tons per year of nickel. The OncaPuma project in Brazil’s Para State began producing ferronickel from laterite in December. Enhancement workcontinued at the new Ravensthorpe Mine in Western Australia at a cost of $190 million. The global automotiveindustry is using more <strong>and</strong> more nickel as the popularity <strong>and</strong> familiarity of electric <strong>and</strong> hybrid vehicles increase.Collaboration between battery manufacturers <strong>and</strong> the U.S. Department of <strong>Energy</strong> has enabled the startup of at leastthree facilities designed to mass produce advanced cathode materials, several of which contain nickel.World Mine Production <strong>and</strong> Reserves: Estimates of reserves for Brazil, China, Indonesia, <strong>and</strong> 18 other countrieswere revised based on new mining industry information from published sources.Mine production Reserves 52009 2010 eUnited States — — —Australia 165,000 139,00024,000,000Botswana 28,600 32,400 490,000Brazil 54,100 66,200 8,700,000Canada 137,000 155,000 3,800,000China 79,400 77,000 3,000,000Colombia 72,000 70,200 1,600,000Cuba 67,300 74,000 5,500,000Dominican Republic — 3,100 960,000Indonesia 203,000 232,000 3,900,000Madagascar — 7,500 1,300,000New Caledonia 7 92,800 138,000 7,100,000Philippines 137,000 156,000 1,100,000Russia 262,000 265,000 6,000,000South Africa 34,600 41,800 3,700,000Venezuela 13,200 14,300 490,000Other countries 51,700 77,8004,500,000World total (rounded) 1,400,000 1,550,000 76,000,000World Resources: Identified l<strong>and</strong>-based resources averaging 1% nickel or greater contain at least 130 million tons ofnickel. About 60% is in laterites <strong>and</strong> 40% is in sulfide deposits. In addition, extensive deep-sea resources of nickel arein manganese crusts <strong>and</strong> nodules covering large areas of the ocean floor, particularly in the Pacific Ocean. The longtermdecline in discovery of new sulfide deposits in traditional mining districts has forced companies to shiftexploration efforts to more challenging locations like the Arabian Peninsula, east-central Africa, <strong>and</strong> the Subarctic.Substitutes: To offset high <strong>and</strong> fluctuating nickel prices, engineers have been substituting low-nickel, duplex, orultrahigh-chromium stainless steels for austenitic grades in construction applications. Nickel-free specialty steels aresometimes used in place of stainless steel within the power-generating <strong>and</strong> petrochemical industries. Titanium alloyscan substitute for nickel metal or nickel-based alloys in corrosive chemical environments. Cost savings inmanufacturing lithium-ion batteries allow them to compete against nickel-metal hydride in certain applications.e Estimated. W Withheld to avoid disclosing company proprietary data. — Zero.1 Scrap receipts – shipments by consumers + exports – imports + adjustments for consumer stock changes.2 Apparent primary consumption + reported secondary consumption.3 Stocks of producers, agents, <strong>and</strong> dealers held only in the United States.4 Defined as imports – exports + adjustments for Government <strong>and</strong> industry stock changes.5 See Appendix C for resource/reserve definitions <strong>and</strong> information concerning data sources.6 For Australia, Joint Ore Reserves Committee (JORC) compliant reserves were only 4.7 million tons.7 Overseas territory of France.U.S. Geological Survey, <strong>Mineral</strong> <strong>Commodity</strong> <strong>Summaries</strong>, January <strong>2011</strong>

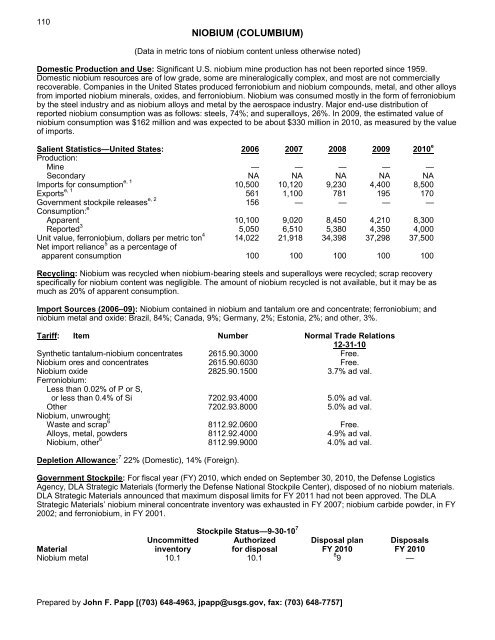

110NIOBIUM (COLUMBIUM)(Data in metric tons of niobium content unless otherwise noted)Domestic Production <strong>and</strong> Use: Significant U.S. niobium mine production has not been reported since 1959.Domestic niobium resources are of low grade, some are mineralogically complex, <strong>and</strong> most are not commerciallyrecoverable. Companies in the United States produced ferroniobium <strong>and</strong> niobium compounds, metal, <strong>and</strong> other alloysfrom imported niobium minerals, oxides, <strong>and</strong> ferroniobium. Niobium was consumed mostly in the form of ferroniobiumby the steel industry <strong>and</strong> as niobium alloys <strong>and</strong> metal by the aerospace industry. Major end-use distribution ofreported niobium consumption was as follows: steels, 74%; <strong>and</strong> superalloys, 26%. In 2009, the estimated value ofniobium consumption was $162 million <strong>and</strong> was expected to be about $330 million in 2010, as measured by the valueof imports.Salient Statistics—United States: 2006 2007 2008 2009 2010 eProduction:Mine — — — — —Secondary NA NA NA NA NAImports for consumption e, 1 10,500 10,120 9,230 4,400 8,500Exports e, 1 561 1,100 781 195 170Government stockpile releases e, 2 156 — — — —Consumption: eApparent 10,100 9,020 8,450 4,210 8,300Reported 3 5,050 6,510 5,380 4,350 4,000Unit value, ferroniobium, dollars per metric ton 4 14,022 21,918 34,398 37,298 37,500Net import reliance 5 as a percentage ofapparent consumption 100 100 100 100 100Recycling: Niobium was recycled when niobium-bearing steels <strong>and</strong> superalloys were recycled; scrap recoveryspecifically for niobium content was negligible. The amount of niobium recycled is not available, but it may be asmuch as 20% of apparent consumption.Import Sources (2006–09): Niobium contained in niobium <strong>and</strong> tantalum ore <strong>and</strong> concentrate; ferroniobium; <strong>and</strong>niobium metal <strong>and</strong> oxide: Brazil, 84%; Canada, 9%; Germany, 2%; Estonia, 2%; <strong>and</strong> other, 3%.Tariff: Item Number Normal Trade Relations12-31-10Synthetic tantalum-niobium concentrates 2615.90.3000 Free.Niobium ores <strong>and</strong> concentrates 2615.90.6030 Free.Niobium oxide 2825.90.1500 3.7% ad val.Ferroniobium:Less than 0.02% of P or S,or less than 0.4% of Si 7202.93.4000 5.0% ad val.Other 7202.93.8000 5.0% ad val.Niobium, unwrought:Waste <strong>and</strong> scrap 6 8112.92.0600 Free.Alloys, metal, powders 8112.92.4000 4.9% ad val.Niobium, other 6 8112.99.9000 4.0% ad val.Depletion Allowance: 7 22% (Domestic), 14% (Foreign).Government Stockpile: For fiscal year (FY) 2010, which ended on September 30, 2010, the Defense LogisticsAgency, DLA Strategic Materials (formerly the Defense National Stockpile Center), disposed of no niobium materials.DLA Strategic Materials announced that maximum disposal limits for FY <strong>2011</strong> had not been approved. The DLAStrategic Materials’ niobium mineral concentrate inventory was exhausted in FY 2007; niobium carbide powder, in FY2002; <strong>and</strong> ferroniobium, in FY 2001.Stockpile Status—9-30-10 7Uncommitted Authorized Disposal plan DisposalsMaterial inventory for disposal FY 2010 FY 2010Niobium metal 10.1 10.18 9 —Prepared by John F. Papp [(703) 648-4963, jpapp@usgs.gov, fax: (703) 648-7757]

- Page 3:

U.S. Department of the InteriorKEN

- Page 6 and 7:

INTRODUCTION3Each chapter of the 20

- Page 8 and 9:

5NET EXPORTS OF MINERALRAW MATERIAL

- Page 10 and 11:

SIGNIFICANT EVENTS, TRENDS, AND ISS

- Page 12 and 13:

mineral materials valued at $1.30 b

- Page 14 and 15:

11MAJOR METAL-PRODUCING AREASAuB2P1

- Page 16 and 17:

13MAJOR INDUSTRIAL MINERAL-PRODUCIN

- Page 18 and 19:

ABRASIVES (MANUFACTURED)15Events, T

- Page 20 and 21:

ALUMINUM17The United States continu

- Page 22 and 23:

ANTIMONY19Events, Trends, and Issue

- Page 24 and 25:

ARSENIC21According to university me

- Page 26 and 27:

ASBESTOS23Events, Trends, and Issue

- Page 28 and 29:

BARITE25Nationally, the rig count o

- Page 30 and 31:

BAUXITE AND ALUMINA27Events, Trends

- Page 32 and 33:

BERYLLIUM29Events, Trends, and Issu

- Page 34 and 35:

BISMUTH31Events, Trends, and Issues

- Page 36 and 37:

BORON33Events, Trends, and Issues:

- Page 38 and 39:

BROMINE35Events, Trends, and Issues

- Page 40 and 41:

CADMIUM37NiCd battery use in consum

- Page 42 and 43:

CEMENT39The manufacture of clinker

- Page 44 and 45:

CESIUM41Events, Trends, and Issues:

- Page 46 and 47:

CHROMIUM43Stockpile Status—9-30-1

- Page 48 and 49:

CLAYS45Tariff: Item Number Normal T

- Page 50 and 51:

COBALT47Events, Trends, and Issues:

- Page 52 and 53:

COPPER49Events, Trends, and Issues:

- Page 54 and 55:

DIAMOND (INDUSTRIAL)51Events, Trend

- Page 56 and 57:

DIATOMITE53Events, Trends, and Issu

- Page 58 and 59:

FELDSPAR55Feldspar use in tile and

- Page 60 and 61:

FLUORSPAR57with planned output of 1

- Page 62 and 63: GALLIUM59In response to the unprece

- Page 64 and 65: GARNET (INDUSTRIAL)61Events, Trends

- Page 66 and 67: GEMSTONES63Events, Trends, and Issu

- Page 68 and 69: GERMANIUM65Events, Trends, and Issu

- Page 70 and 71: GOLD67With the increase in price of

- Page 72 and 73: GRAPHITE (NATURAL)69Events, Trends,

- Page 74 and 75: GYPSUM71Through 2010, more than 3,6

- Page 76 and 77: HELIUM73Events, Trends, and Issues:

- Page 78 and 79: INDIUM75China’s 21 indium produce

- Page 80 and 81: IODINE77Events, Trends, and Issues:

- Page 82 and 83: IRON AND STEEL79Events, Trends, and

- Page 84 and 85: IRON AND STEEL SCRAP81Tariff: Item

- Page 86 and 87: IRON AND STEEL SLAG83Events, Trends

- Page 88 and 89: IRON ORE85In 2009, China imported a

- Page 90 and 91: IRON OXIDE PIGMENTS87Events, Trends

- Page 92 and 93: KYANITE AND RELATED MATERIALS89Even

- Page 94 and 95: LEAD91caused by underground fires a

- Page 96 and 97: LIME93The lime industry is facing p

- Page 98 and 99: LITHIUM95market, and a facility at

- Page 100 and 101: MAGNESIUM COMPOUNDS97In Australia,

- Page 102 and 103: MAGNESIUM METAL99U.S. magnesium con

- Page 104 and 105: MANGANESE101Government Stockpile:St

- Page 106 and 107: MERCURY103Events, Trends, and Issue

- Page 108 and 109: MICA (NATURAL)105Depletion Allowanc

- Page 110 and 111: MOLYBDENUM107Events, Trends, and Is

- Page 114 and 115: NIOBIUM (COLUMBIUM)111Events, Trend

- Page 116 and 117: NITROGEN (FIXED)—AMMONIA113Accord

- Page 118 and 119: PEAT115Events, Trends, and Issues:

- Page 120 and 121: PERLITE117Events, Trends, and Issue

- Page 122 and 123: PHOSPHATE ROCK119Events, Trends, an

- Page 124 and 125: PLATINUM-GROUP METALS121Events, Tre

- Page 126 and 127: POTASH123Events, Trends, and Issues

- Page 128 and 129: PUMICE AND PUMICITE125Events, Trend

- Page 130 and 131: QUARTZ CRYSTAL (INDUSTRIAL)127Event

- Page 132 and 133: RARE EARTHS129Events, Trends, and I

- Page 134 and 135: RHENIUM131Events, Trends, and Issue

- Page 136 and 137: RUBIDIUM133Events, Trends, and Issu

- Page 138 and 139: SALT135Many chefs have advocated us

- Page 140 and 141: SAND AND GRAVEL (CONSTRUCTION)137Ev

- Page 142 and 143: SAND AND GRAVEL (INDUSTRIAL)139The

- Page 144 and 145: SCANDIUM141Scandium’s use in meta

- Page 146 and 147: SELENIUM143Events, Trends, and Issu

- Page 148 and 149: SILICON145Events, Trends, and Issue

- Page 150 and 151: SILVER147Silver was used as a repla

- Page 152 and 153: SODA ASH149A Wyoming soda ash produ

- Page 154 and 155: SODIUM SULFATE151Events, Trends, an

- Page 156 and 157: STONE (CRUSHED)153Events, Trends, a

- Page 158 and 159: STONE (DIMENSION)155Events, Trends,

- Page 160 and 161: STRONTIUM157Events, Trends, and Iss

- Page 162 and 163:

SULFUR159World sulfur production in

- Page 164 and 165:

TALC AND PYROPHYLLITE161Events, Tre

- Page 166 and 167:

TANTALUM163Events, Trends, and Issu

- Page 168 and 169:

TELLURIUM165Events, Trends, and Iss

- Page 170:

THALLIUM167Beginning in 2009, there

- Page 173 and 174:

170TIN(Data in metric tons of tin c

- Page 175 and 176:

172TITANIUM AND TITANIUM DIOXIDE 1(

- Page 177 and 178:

174TITANIUM MINERAL CONCENTRATES 1(

- Page 179 and 180:

176TUNGSTEN(Data in metric tons of

- Page 181 and 182:

178VANADIUM(Data in metric tons of

- Page 183 and 184:

180VERMICULITE(Data in thousand met

- Page 185 and 186:

182WOLLASTONITE(Data in metric tons

- Page 187 and 188:

184YTTRIUM 1(Data in metric tons of

- Page 189 and 190:

186ZEOLITES (NATURAL)(Data in metri

- Page 191 and 192:

188ZINC(Data in thousand metric ton

- Page 193 and 194:

190ZIRCONIUM AND HAFNIUM(Data in me

- Page 195 and 196:

192APPENDIX AAbbreviations and Unit

- Page 197 and 198:

194Demonstrated.—A term for the s

- Page 199 and 200:

196Part B—Sources of Reserves Dat

- Page 201:

198Europe and Central Eurasia—con