CEIOPS' Advice for Level 2 Implementing ... - EIOPA - Europa

CEIOPS' Advice for Level 2 Implementing ... - EIOPA - Europa

CEIOPS' Advice for Level 2 Implementing ... - EIOPA - Europa

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

∑ − n 1<br />

s=<br />

k<br />

SCR<br />

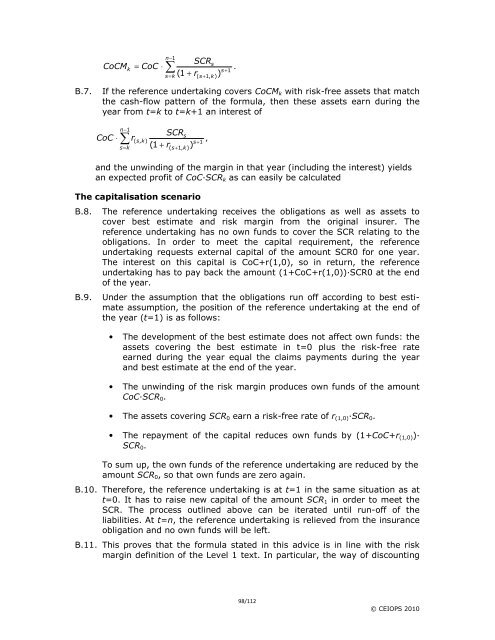

CoCM k = CoC ⋅<br />

.<br />

( 1 + r<br />

s<br />

s+<br />

1<br />

( s+<br />

1,<br />

k)<br />

)<br />

B.7. If the reference undertaking covers CoCMk with risk-free assets that match<br />

the cash-flow pattern of the <strong>for</strong>mula, then these assets earn during the<br />

year from t=k to t=k+1 an interest of<br />

∑ − n 1<br />

s=<br />

k<br />

SCR<br />

CoC ⋅ r(<br />

s,<br />

k)<br />

,<br />

( 1 + r<br />

s<br />

s+<br />

1<br />

( s+<br />

1,<br />

k)<br />

)<br />

and the unwinding of the margin in that year (including the interest) yields<br />

an expected profit of CoC·SCRk as can easily be calculated<br />

The capitalisation scenario<br />

B.8. The reference undertaking receives the obligations as well as assets to<br />

cover best estimate and risk margin from the original insurer. The<br />

reference undertaking has no own funds to cover the SCR relating to the<br />

obligations. In order to meet the capital requirement, the reference<br />

undertaking requests external capital of the amount SCR0 <strong>for</strong> one year.<br />

The interest on this capital is CoC+r(1,0), so in return, the reference<br />

undertaking has to pay back the amount (1+CoC+r(1,0))·SCR0 at the end<br />

of the year.<br />

B.9. Under the assumption that the obligations run off according to best estimate<br />

assumption, the position of the reference undertaking at the end of<br />

the year (t=1) is as follows:<br />

• The development of the best estimate does not affect own funds: the<br />

assets covering the best estimate in t=0 plus the risk-free rate<br />

earned during the year equal the claims payments during the year<br />

and best estimate at the end of the year.<br />

• The unwinding of the risk margin produces own funds of the amount<br />

CoC·SCR0.<br />

• The assets covering SCR0 earn a risk-free rate of r(1,0)·SCR0.<br />

• The repayment of the capital reduces own funds by (1+CoC+r(1,0))·<br />

SCR0.<br />

To sum up, the own funds of the reference undertaking are reduced by the<br />

amount SCR0, so that own funds are zero again.<br />

B.10. There<strong>for</strong>e, the reference undertaking is at t=1 in the same situation as at<br />

t=0. It has to raise new capital of the amount SCR1 in order to meet the<br />

SCR. The process outlined above can be iterated until run-off of the<br />

liabilities. At t=n, the reference undertaking is relieved from the insurance<br />

obligation and no own funds will be left.<br />

B.11. This proves that the <strong>for</strong>mula stated in this advice is in line with the risk<br />

margin definition of the <strong>Level</strong> 1 text. In particular, the way of discounting<br />

98/112<br />

© CEIOPS 2010