Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

68<br />

US$ 1,000 PCM<br />

800<br />

700<br />

600<br />

500<br />

400<br />

300<br />

200<br />

100<br />

0<br />

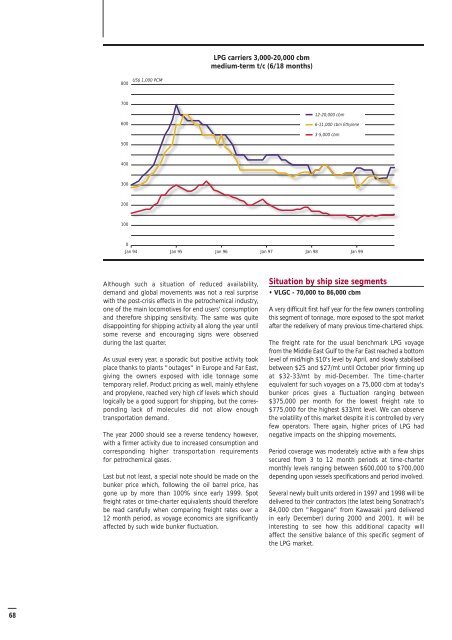

Although such a situation of reduced availability,<br />

demand and global movements was not a real surprise<br />

with the post-crisis effects in the petrochemical industry,<br />

one of the main locomotives for end users' consumption<br />

and therefore shipping sensitivity. The same was quite<br />

disappointing for shipping activity all along the year until<br />

some reverse and encouraging signs were observed<br />

during the last quarter.<br />

As usual every year, a sporadic but positive activity <strong>to</strong>ok<br />

place thanks <strong>to</strong> plants "outages" in Europe and Far East,<br />

giving the owners exposed with idle <strong>to</strong>nnage some<br />

temporary relief. Product pricing as well, mainly ethylene<br />

and propylene, reached very high cif levels which should<br />

logically be a good support for shipping, but the corresponding<br />

lack of molecules did not allow enough<br />

transportation demand.<br />

The year 2000 should see a reverse tendency however,<br />

with a firmer activity due <strong>to</strong> increased consumption and<br />

corresponding higher transportation requirements<br />

for petrochemical gases.<br />

Last but not least, a special note should be made on the<br />

bunker price which, following the oil barrel price, has<br />

gone up by more than 100% since early 1999. Spot<br />

freight rates or time-charter equivalents should therefore<br />

be read carefully when comparing freight rates over a<br />

12 month period, as voyage economics are significantly<br />

affected by such wide bunker fluctuation.<br />

LPG carriers 3,000-20,000 cbm<br />

medium-term t/c (6/18 months)<br />

12-20,000 cbm<br />

6-11,000 cbm Ethylene<br />

3-5,000 cbm<br />

Jan 94 Jan 95 Jan 96 Jan 97 Jan 98 Jan 99<br />

Situation by ship size segments<br />

• VLGC - 70,000 <strong>to</strong> 86,000 cbm<br />

A very difficult first half year for the few owners controlling<br />

this segment of <strong>to</strong>nnage, more exposed <strong>to</strong> the spot market<br />

after the redelivery of many previous time-chartered ships.<br />

The freight rate for the usual benchmark LPG voyage<br />

from the Middle East Gulf <strong>to</strong> the Far East reached a bot<strong>to</strong>m<br />

level of mid/high $10's level by April, and slowly stabilised<br />

between $25 and $27/mt until Oc<strong>to</strong>ber prior firming up<br />

at $32-33/mt by mid-December. The time-charter<br />

equivalent for such voyages on a 75,000 cbm at <strong>to</strong>day's<br />

bunker prices gives a fluctuation ranging between<br />

$375,000 per month for the lowest freight rate <strong>to</strong><br />

$775,000 for the highest $33/mt level. We can observe<br />

the volatility of this market despite it is controlled by very<br />

few opera<strong>to</strong>rs. There again, higher prices of LPG had<br />

negative impacts on the shipping movements.<br />

Period coverage was moderately active with a few ships<br />

secured from 3 <strong>to</strong> 12 month periods at time-charter<br />

monthly levels ranging between $600,000 <strong>to</strong> $700,000<br />

depending upon vessels specifications and period involved.<br />

Several newly built units ordered in 1997 and 1998 will be<br />

delivered <strong>to</strong> their contrac<strong>to</strong>rs (the latest being Sonatrach's<br />

84,000 cbm "Reggane" from Kawasaki yard delivered<br />

in early December) during 2000 and 2001. It will be<br />

interesting <strong>to</strong> see how this additional capacity will<br />

affect the sensitive balance of this specific segment of<br />

the LPG market.