You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

76<br />

90<br />

80<br />

70<br />

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

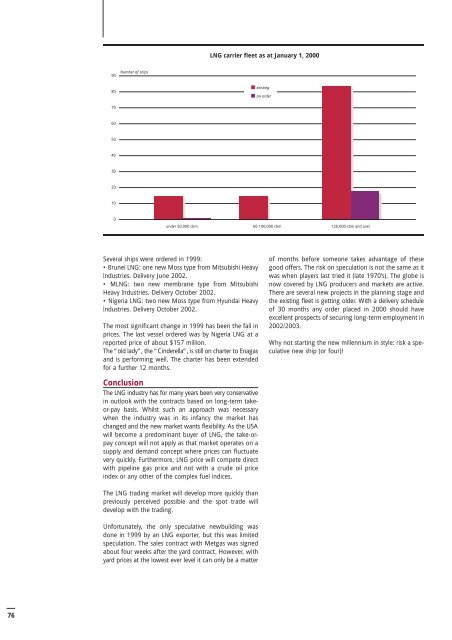

Number of ships<br />

Several ships were ordered in 1999:<br />

• Brunei LNG: one new Moss type from Mitsubishi Heavy<br />

Industries. Delivery June 2002.<br />

• MLNG: two new membrane type from Mitsubishi<br />

Heavy Industries. Delivery Oc<strong>to</strong>ber 2002.<br />

• Nigeria LNG: two new Moss type from Hyundai Heavy<br />

Industries. Delivery Oc<strong>to</strong>ber 2002.<br />

The most significant change in 1999 has been the fall in<br />

prices. The last vessel ordered was by Nigeria LNG at a<br />

reported price of about $157 million.<br />

The “old lady”, the “Cinderella”, is still on charter <strong>to</strong> Enagas<br />

and is performing well. The charter has been extended<br />

for a further 12 months.<br />

Conclusion<br />

The LNG industry has for many years been very conservative<br />

in outlook with the contracts based on long-term takeor-pay<br />

basis. Whilst such an approach was necessary<br />

when the industry was in its infancy the market has<br />

changed and the new market wants flexibility. As the USA<br />

will become a predominant buyer of LNG, the take-orpay<br />

concept will not apply as that market operates on a<br />

supply and demand concept where prices can fluctuate<br />

very quickly. Furthermore, LNG price will compete direct<br />

with pipeline gas price and not with a crude oil price<br />

index or any other of the complex fuel indices.<br />

The LNG trading market will develop more quickly than<br />

previously perceived possible and the spot trade will<br />

develop with the trading.<br />

Unfortunately, the only speculative newbuilding was<br />

done in 1999 by an LNG exporter, but this was limited<br />

speculation. The sales contract with Metgas was signed<br />

about four weeks after the yard contract. However, with<br />

yard prices at the lowest ever level it can only be a matter<br />

LNG carrier fleet as at January 1, 2000<br />

existing<br />

on order<br />

under 50,000 cbm 60-100,000 cbm 120,000 cbm and over<br />

of months before someone takes advantage of these<br />

good offers. The risk on speculation is not the same as it<br />

was when players last tried it (late 1970’s). The globe is<br />

now covered by LNG producers and markets are active.<br />

There are several new projects in the planning stage and<br />

the existing fleet is getting older. With a delivery schedule<br />

of 30 months any order placed in 2000 should have<br />

excellent prospects of securing long-term employment in<br />

2002/2003.<br />

Why not starting the new millennium in style: risk a speculative<br />

new ship (or four)!