SMS Siemag AG - Alu-web.de

SMS Siemag AG - Alu-web.de

SMS Siemag AG - Alu-web.de

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

E conoM ics<br />

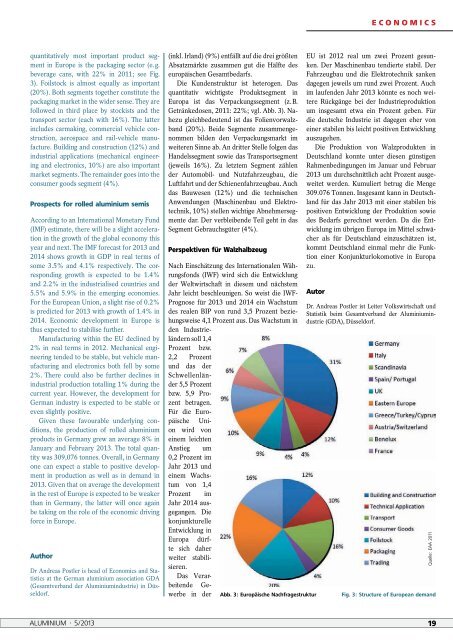

quantitatively most important product segment<br />

in Europe is the packaging sector (e. g.<br />

beverage cans, with 22% in 2011; see Fig.<br />

3). Foilstock is almost equally as important<br />

(20%). Both segments together constitute the<br />

packaging market in the wi<strong>de</strong>r sense. They are<br />

followed in third place by stockists and the<br />

transport sector (each with 16%). The latter<br />

inclu<strong>de</strong>s carmaking, commercial vehicle construction,<br />

aerospace and rail-vehicle manufacture.<br />

Building and construction (12%) and<br />

industrial applications (mechanical engineering<br />

and electronics, 10%) are also important<br />

market segments. The remain<strong>de</strong>r goes into the<br />

consumer goods segment (4%).<br />

Prospects for rolled aluminium semis<br />

According to an International Monetary Fund<br />

(IMF) estimate, there will be a slight acceleration<br />

in the growth of the global economy this<br />

year and next. The IMF forecast for 2013 and<br />

2014 shows growth in GDP in real terms of<br />

some 3.5% and 4.1% respectively. The corresponding<br />

growth is expected to be 1.4%<br />

and 2.2% in the industrialised countries and<br />

5.5% and 5.9% in the emerging economies.<br />

For the European Union, a slight rise of 0.2%<br />

is predicted for 2013 with growth of 1.4% in<br />

2014. Economic <strong>de</strong>velopment in Europe is<br />

thus expected to stabilise further.<br />

Manufacturing within the EU <strong>de</strong>clined by<br />

2% in real terms in 2012. Mechanical engineering<br />

ten<strong>de</strong>d to be stable, but vehicle manufacturing<br />

and electronics both fell by some<br />

2%. There could also be further <strong>de</strong>clines in<br />

industrial production totalling 1% during the<br />

current year. However, the <strong>de</strong>velopment for<br />

German industry is expected to be stable or<br />

even slightly positive.<br />

Given these favourable un<strong>de</strong>rlying conditions,<br />

the production of rolled aluminium<br />

products in Germany grew an average 8% in<br />

January and February 2013. The total quantity<br />

was 309,076 tonnes. Overall, in Germany<br />

one can expect a stable to positive <strong>de</strong>velopment<br />

in production as well as in <strong>de</strong>mand in<br />

2013. Given that on average the <strong>de</strong>velopment<br />

in the rest of Europe is expected to be weaker<br />

than in Germany, the latter will once again<br />

be taking on the role of the economic driving<br />

force in Europe.<br />

author<br />

Dr Andreas Postler is head of Economics and Statistics<br />

at the German aluminium association GDA<br />

(Gesamtverband <strong>de</strong>r <strong>Alu</strong>miniumindustrie) in Düsseldorf.<br />

(inkl. Irland) (9%) entfällt auf die drei größten<br />

Absatzmärkte zusammen gut die Hälfte <strong>de</strong>s<br />

europäischen Gesamtbedarfs.<br />

Die Kun<strong>de</strong>nstruktur ist heterogen. Das<br />

quantitativ wichtigste Produktsegment in<br />

Europa ist das Verpackungssegment (z. B.<br />

Getränkedosen, 2011: 22%; vgl. Abb. 3). Nahezu<br />

gleichbe<strong>de</strong>utend ist das Folienvorwalzband<br />

(20%). Bei<strong>de</strong> Segmente zusammengenommen<br />

bil<strong>de</strong>n <strong>de</strong>n Verpackungsmarkt im<br />

weiteren Sinne ab. An dritter Stelle folgen das<br />

Han<strong>de</strong>lssegment sowie das Transportsegment<br />

(jeweils 16%). Zu letztem Segment zählen<br />

<strong>de</strong>r Automobil- und Nutzfahrzeugbau, die<br />

Luftfahrt und <strong>de</strong>r Schienenfahrzeugbau. Auch<br />

das Bauwesen (12%) und die technischen<br />

Anwendungen (Maschinenbau und Elektrotechnik,<br />

10%) stellen wichtige Abnehmersegmente<br />

dar. Der verbleiben<strong>de</strong> Teil geht in das<br />

Segment Gebrauchsgüter (4%).<br />

Perspektiven für Walzhalbzeug<br />

Nach Einschätzung <strong>de</strong>s Internationalen Währungsfonds<br />

(IWF) wird sich die Entwicklung<br />

<strong>de</strong>r Weltwirtschaft in diesem und nächstem<br />

Jahr leicht beschleunigen. So weist die IWF-<br />

Prognose für 2013 und 2014 ein Wachstum<br />

<strong>de</strong>s realen BIP von rund 3,5 Prozent beziehungsweise<br />

4,1 Prozent aus. Das Wachstum in<br />

<strong>de</strong>n Industrielän<strong>de</strong>rn<br />

soll 1,4<br />

Prozent bzw.<br />

2,2 Prozent<br />

und das <strong>de</strong>r<br />

Schwellenlän<strong>de</strong>r<br />

5,5 Prozent<br />

bzw. 5,9 Prozent<br />

betragen.<br />

Für die Europäische<br />

Union<br />

wird von<br />

einem leichten<br />

Anstieg um<br />

0,2 Prozent im<br />

Jahr 2013 und<br />

einem Wachstum<br />

von 1,4<br />

Prozent im<br />

Jahr 2014 ausgegangen.<br />

Die<br />

konjunkturelle<br />

Entwicklung in<br />

Europa dürfte<br />

sich daher<br />

weiter stabilisieren.<br />

Das Verarbeiten<strong>de</strong><br />

Gewerbe<br />

in <strong>de</strong>r<br />

EU ist 2012 real um zwei Prozent gesunken.<br />

Der Maschinenbau tendierte stabil. Der<br />

Fahrzeugbau und die Elektrotechnik sanken<br />

dagegen jeweils um rund zwei Prozent. Auch<br />

im laufen<strong>de</strong>n Jahr 2013 könnte es noch weitere<br />

Rückgänge bei <strong>de</strong>r Industrieproduktion<br />

um insgesamt etwa ein Prozent geben. Für<br />

die <strong>de</strong>utsche Industrie ist dagegen eher von<br />

einer stabilen bis leicht positiven Entwicklung<br />

auszugehen.<br />

Die Produktion von Walzprodukten in<br />

Deutschland konnte unter diesen günstigen<br />

Rahmenbedingungen im Januar und Februar<br />

2013 um durchschnittlich acht Prozent ausgeweitet<br />

wer<strong>de</strong>n. Kumuliert betrug die Menge<br />

309.076 Tonnen. Insgesamt kann in Deutschland<br />

für das Jahr 2013 mit einer stabilen bis<br />

positiven Entwicklung <strong>de</strong>r Produktion sowie<br />

<strong>de</strong>s Bedarfs gerechnet wer<strong>de</strong>n. Da die Entwicklung<br />

im übrigen Europa im Mittel schwächer<br />

als für Deutschland einzuschätzen ist,<br />

kommt Deutschland einmal mehr die Funktion<br />

einer Konjunkturlokomotive in Europa<br />

zu.<br />

autor<br />

Abb. 3: Europäische Nachfragestruktur<br />

Dr. Andreas Postler ist Leiter Volkswirtschaft und<br />

Statistik beim Gesamtverband <strong>de</strong>r <strong>Alu</strong>miniumindustrie<br />

(GDA), Düsseldorf.<br />

Quelle: EAA 2011<br />

Fig. 3: Structure of European <strong>de</strong>mand<br />

ALUMINIUM · 5/2013 19