You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

TMT<br />

<strong>Memory</strong> Devices Technology<br />

8 October 2010<br />

abc<br />

year. Reassuringly, this is still well below the<br />

2005-08 average of 54%.<br />

Global DRAM capex (USDm)<br />

DRAM contract prices<br />

3<br />

2.5<br />

15,000<br />

200%<br />

2<br />

10,000<br />

150%<br />

100%<br />

1.5<br />

50%<br />

1<br />

5,000<br />

-<br />

2008 2009e 2010f 2011f 2012f<br />

0%<br />

-50%<br />

-100%<br />

Jul-09<br />

Oct-09<br />

Jan-10<br />

Apr-10<br />

Jul-10<br />

1Gb DDR2 128Mx 8 667 Mhz contract<br />

1Gb DDR3 128Mx 8 1066MHz contract<br />

Source: DRAMeXchange<br />

Source: Gartner, HSBC forecasts<br />

Total (HSBC) y-o-y (%)<br />

The off-shoot of this is surging bit supply in<br />

4Q10-1Q11, when the full brunt of extra capacity<br />

by Samsung, plus commercial yields from process<br />

migration by second-tier players such as Nanya<br />

and Inotera, comes into effect, as they bring on<br />

line 5xnm capacity that was held up in the past 2-<br />

3 quarters due to yield issues. We believe Nanya<br />

is now achieving c70% yield for its 5xnm process,<br />

which is sufficient to mass produce. We expect<br />

global supply bit growth in 3Q-4Q10 to rise 11%<br />

and 18% q-o-q respectively.<br />

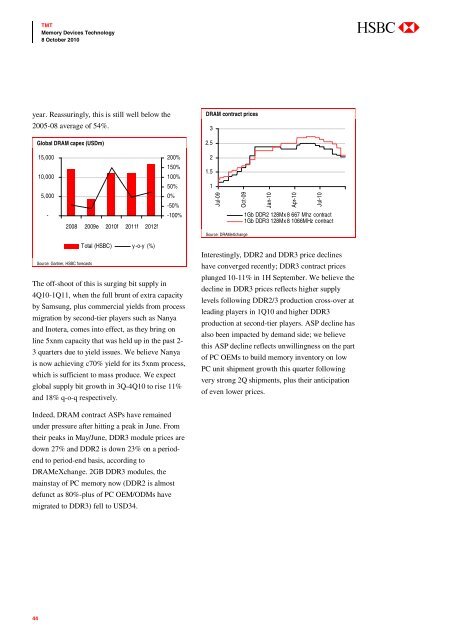

Interestingly, DDR2 and DDR3 price declines<br />

have converged recently; DDR3 contract prices<br />

plunged 10-11% in 1H September. We believe the<br />

decline in DDR3 prices reflects higher supply<br />

levels following DDR2/3 production cross-over at<br />

leading players in 1Q10 and higher DDR3<br />

production at second-tier players. ASP decline has<br />

also been impacted by demand side; we believe<br />

this ASP decline reflects unwillingness on the part<br />

of PC OEMs to build memory inventory on low<br />

PC unit shipment growth this quarter following<br />

very strong 2Q shipments, plus their anticipation<br />

of even lower prices.<br />

Indeed, DRAM contract ASPs have remained<br />

under pressure after hitting a peak in June. From<br />

their peaks in May/June, DDR3 module prices are<br />

down 27% and DDR2 is down 23% on a periodend<br />

to period-end basis, according to<br />

DRAMeXchange. 2GB DDR3 modules, the<br />

mainstay of PC memory now (DDR2 is almost<br />

defunct as 80%-plus of PC OEM/ODMs have<br />

migrated to DDR3) fell to USD34.<br />

44