Statutory Residence Test - HM Revenue & Customs

Statutory Residence Test - HM Revenue & Customs

Statutory Residence Test - HM Revenue & Customs

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

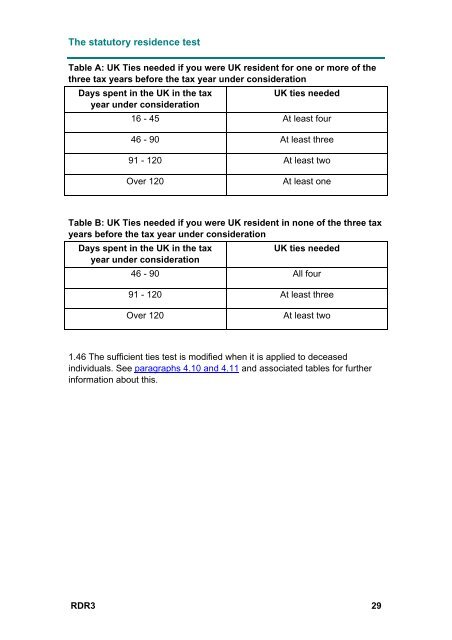

The statutory residence test<br />

Table A: UK Ties needed if you were UK resident for one or more of the<br />

three tax years before the tax year under consideration<br />

Days spent in the UK in the tax<br />

year under consideration<br />

UK ties needed<br />

16 - 45 At least four<br />

46 - 90 At least three<br />

91 - 120 At least two<br />

Over 120<br />

At least one<br />

Table B: UK Ties needed if you were UK resident in none of the three tax<br />

years before the tax year under consideration<br />

Days spent in the UK in the tax<br />

UK ties needed<br />

year under consideration<br />

46 - 90 All four<br />

91 - 120 At least three<br />

Over 120<br />

At least two<br />

1.46 The sufficient ties test is modified when it is applied to deceased<br />

individuals. See paragraphs 4.10 and 4.11 and associated tables for further<br />

information about this.<br />

RDR3 29