Statutory Residence Test - HM Revenue & Customs

Statutory Residence Test - HM Revenue & Customs

Statutory Residence Test - HM Revenue & Customs

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Split Year Treatment<br />

<br />

spend no more than the permitted limit of days in the UK during that<br />

period.<br />

Case 1: Calculating whether you work full time overseas during the<br />

relevant period<br />

5.12 Apply the sufficient hours overseas calculation to the relevant period with<br />

these modifications:<br />

<br />

the maximum number of days you can subtract from the reference<br />

period for gaps between employments, is reduced from 30 days to the<br />

permitted limit of days that can be subtracted for gaps between<br />

employments<br />

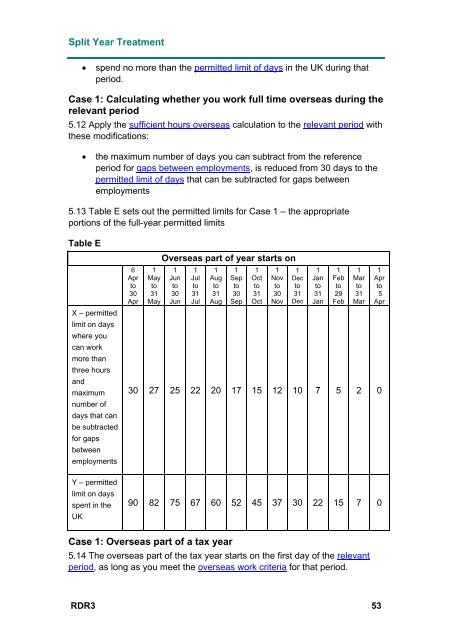

5.13 Table E sets out the permitted limits for Case 1 – the appropriate<br />

portions of the full-year permitted limits<br />

Table E<br />

X – permitted<br />

limit on days<br />

where you<br />

can work<br />

more than<br />

three hours<br />

and<br />

maximum<br />

number of<br />

days that can<br />

be subtracted<br />

for gaps<br />

between<br />

employments<br />

6<br />

Apr<br />

to<br />

30<br />

Apr<br />

1<br />

May<br />

to<br />

31<br />

May<br />

Overseas part of year starts on<br />

1<br />

Jun<br />

to<br />

30<br />

Jun<br />

1<br />

Jul<br />

to<br />

31<br />

Jul<br />

1<br />

Aug<br />

to<br />

31<br />

Aug<br />

1<br />

Sep<br />

to<br />

30<br />

Sep<br />

1<br />

Oct<br />

to<br />

31<br />

Oct<br />

1<br />

Nov<br />

to<br />

30<br />

Nov<br />

1<br />

Dec<br />

to<br />

31<br />

Dec<br />

1<br />

Jan<br />

to<br />

31<br />

Jan<br />

1<br />

Feb<br />

to<br />

29<br />

Feb<br />

1<br />

Mar<br />

to<br />

31<br />

Mar<br />

30 27 25 22 20 17 15 12 10 7 5 2 0<br />

1<br />

Apr<br />

to<br />

5<br />

Apr<br />

Y – permitted<br />

limit on days<br />

spent in the<br />

UK<br />

90 82 75 67 60 52 45 37 30 22 15 7 0<br />

Case 1: Overseas part of a tax year<br />

5.14 The overseas part of the tax year starts on the first day of the relevant<br />

period, as long as you meet the overseas work criteria for that period.<br />

RDR3 53