- Page 1 and 2:

Exceptional Argentina Di Tella, Gla

- Page 3 and 4:

A third explanation of Argentina’

- Page 5 and 6:

Maddison's "Western Offshoots" by l

- Page 7 and 8:

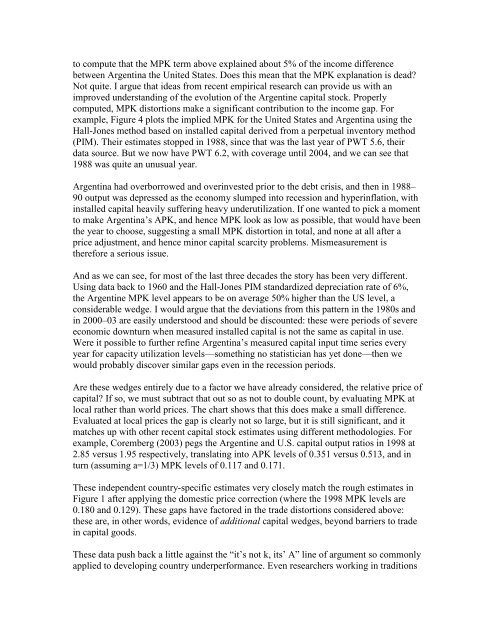

A final point on this mechanistic a

- Page 9 and 10:

GDP in 1900 at 12,100 (in constant

- Page 11 and 12:

nationalized railways and banks, to

- Page 13 and 14:

country interacted with initial con

- Page 15 and 16:

1900. As there is an extremely stro

- Page 17 and 18:

Between the 1940s and 1970s income

- Page 19 and 20:

particularly in terms of food consu

- Page 21 and 22:

Even before the 2001 crisis, Argent

- Page 23 and 24:

Scandinavia and Northern Europe the

- Page 25 and 26:

Figure 4. A modified Human Developm

- Page 27 and 28:

Figure 6. Per capita GDP across Arg

- Page 29 and 30:

production 15 . Moreover, beyond st

- Page 31 and 32:

Figure 10. Average weight of export

- Page 33 and 34:

etween the prewar export-led growth

- Page 35 and 36:

which was wholly bound to local dem

- Page 37 and 38:

protectionism", certainly stronger

- Page 39 and 40: agricultural pastures and cropland

- Page 41 and 42: far. Argentina's differential popul

- Page 43 and 44: Appendix Figure A. 1. Argentina's r

- Page 45 and 46: Peru 35 38 25 34 34 34 32 29 26 27

- Page 47 and 48: Like the Llach paper, the Campante

- Page 49 and 50: I. Introduction Both Buenos Aires a

- Page 51 and 52: across the ocean. Over the course o

- Page 53 and 54: Buenos Aires’ hinterland rose dra

- Page 55 and 56: significantly greater education lev

- Page 57 and 58: Why is there such a difference in l

- Page 59 and 60: illion dollars today). Each Chicago

- Page 61 and 62: Chicago also appears to have been a

- Page 63 and 64: casualties. Roca secured the presid

- Page 65 and 66: capital to St. Petersburg he was pr

- Page 67 and 68: and the logarithm of per capita GDP

- Page 69 and 70: Moreover, years of schooling today

- Page 71 and 72: y its overwhelming political import

- Page 73 and 74: 200 Figure 2a: Annual Wage Data 187

- Page 75 and 76: Figure 3: Real Monthly Wages in Chi

- Page 77 and 78: Log GDP per capita 2000 5 6 7 8 9 1

- Page 79 and 80: Figure 7 Log GDP per capita 2000 7

- Page 81 and 82: Table 2: Top 5 Industries in Chicag

- Page 83 and 84: Table 4: 19th Century Variables and

- Page 85 and 86: A simple calculation suggests that

- Page 87 and 88: toy model with a minimum of paramet

- Page 89: were lifted, but import taxes remai

- Page 93 and 94: versus foreigners, on most occasion

- Page 95 and 96: X institutions policies income p

- Page 97 and 98: series variation. The coincidence o

- Page 99 and 100: Figure 1—The Great Divergence and

- Page 101 and 102: Figure 3—Trade taxes

- Page 103 and 104: Transition Remarks The previous ess

- Page 105 and 106: CHAPTER FOUR Argentine Trade Polici

- Page 107 and 108: Argentine comparative advantage lie

- Page 109 and 110: thousands of product lines in Argen

- Page 111 and 112: Japan). Third, the agricultural pro

- Page 113 and 114: different preferences over trade pr

- Page 115 and 116: two nomenclatures had to be manuall

- Page 117 and 118: esult, soybeans were finally adopte

- Page 119 and 120: Figure 1 Trade Openness Exports + I

- Page 121 and 122: Figure 5 Relative Sectoral Protecti

- Page 123 and 124: Figure 7 Average Export Taxes 0 10

- Page 125 and 126: Figure 9 Average Export Taxes at 2-

- Page 127 and 128: Figure 11 Evolution of Argentine Ag

- Page 129 and 130: Figure 13 Yields in Agriculture: Wh

- Page 131 and 132: Table 2 Livestock per Capita 1895 C

- Page 133 and 134: Table 5 Mean Share of Exports (Impo

- Page 135 and 136: Table 7 Tariff Statistics for perio

- Page 137 and 138: Table 9 Evolution of Industrial Pro

- Page 139 and 140: CHAPTER FIVE Path-Dependent Import-

- Page 141 and 142:

actors, and they were demanding pro

- Page 143 and 144:

the primary sector, using land and

- Page 145 and 146:

Figure 1: The Long Run: Four Region

- Page 147 and 148:

Finally, in the reversal of pattern

- Page 149 and 150:

Figure 3: Medium Run Preferences ov

- Page 151 and 152:

sector to give rise to a protection

- Page 153 and 154:

technological improvements or incre

- Page 155 and 156:

Argentina did relatively well when

- Page 157 and 158:

World War, a second globalization e

- Page 159 and 160:

Argentine primary sector and ensure

- Page 161 and 162:

Clearly, world market conditions we

- Page 163 and 164:

for the years to come. The most imp

- Page 165 and 166:

governments zigzagged in their poli

- Page 167 and 168:

public spending on infrastructure s

- Page 169 and 170:

understand the rise of the urban-ru

- Page 171 and 172:

To sum up, by the beginning of the

- Page 173 and 174:

has a comparative advantage in the

- Page 175 and 176:

L λ = m L K κ = m K That is, λ i

- Page 177 and 178:

K c a = 1− α 1−α T A ( κ )

- Page 179 and 180:

Given a set of parameters ϒ , φ a

- Page 181 and 182:

consumption of good i. For any agen

- Page 183 and 184:

Proposition 3 In the short run, pro

- Page 185 and 186:

ρ 1/ 1 ρ ρ 1 ( ξ ξ ) 1 TT K ,

- Page 187 and 188:

Up to 2008, the FPV government had

- Page 189 and 190:

negative correlation between the pr

- Page 191 and 192:

policies would, supposedly, eviscer

- Page 193 and 194:

I. Introduction In a seminal study,

- Page 195 and 196:

terms, Peronist beliefs in the 1990

- Page 197 and 198:

Several authors have emphasized the

- Page 199 and 200:

foreign capital and trade as the gl

- Page 201 and 202:

of already available information. A

- Page 203 and 204:

having the need to do more than wak

- Page 205 and 206:

Argentines (who implement these pol

- Page 207 and 208:

opinion about elements of capitalis

- Page 209 and 210:

intense (the proportion is under 1.

- Page 211 and 212:

involved in social ordering that wi

- Page 213 and 214:

cost of the deviating firm, since w

- Page 215 and 216:

Admissible Region Bounds on w b Nex

- Page 217 and 218:

The previous proposition may be par

- Page 219 and 220:

and note that Peron insists on the

- Page 221 and 222:

Appendix 2: Definitions of Variable

- Page 223 and 224:

Table II: The Beliefs of Peronists

- Page 225 and 226:

Transition Remarks The previous cha

- Page 227 and 228:

CHAPTER SEVEN A Short Episodic Hist

- Page 229 and 230:

the income distribution between 193

- Page 231 and 232:

empirical evidence and on existing

- Page 233 and 234:

of commodities. The country was off

- Page 235 and 236:

accounts increased by 8% between 19

- Page 237 and 238:

Argentina in 1942 (4.1%) is not ver

- Page 239 and 240:

This change in inequality is also r

- Page 241 and 242:

1982, when Mexico’s default on it

- Page 243 and 244:

1995. While growth bounced back qui

- Page 245 and 246:

The main characteristics of this ep

- Page 247 and 248:

skilled workers that more than offs

- Page 249 and 250:

Household Expenditure Survey. An in

- Page 251 and 252:

The relationship between internatio

- Page 253 and 254:

machinery and equipment can acceler

- Page 255 and 256:

occurred not only in production tec

- Page 257 and 258:

a relative abundance of rents to sh

- Page 259 and 260:

even when the number of well-off in

- Page 261 and 262:

and similar patterns emerge when co

- Page 263 and 264:

This chapter described the level an

- Page 265 and 266:

Transition Remarks Economic success

- Page 267 and 268:

CHAPTER EIGHT Why do Argentines tru

- Page 269 and 270:

in the 1970s and 1980s. Despite the

- Page 271 and 272:

Figure 5. Percentage of the populat

- Page 273 and 274:

analysis of the Argentinean and Chi

- Page 275 and 276:

observationally equivalent individu

- Page 277 and 278:

the low rank policeman. 13 4. The C

- Page 279 and 280:

Figure 7. Share of people having a

- Page 281 and 282:

6. Why did the Argentinean Police d

- Page 283 and 284:

instability, σ, a worried leader h

- Page 285 and 286:

the deeper question of why the Arge

- Page 287 and 288:

Table 2. Comparative facts for cano

- Page 289 and 290:

of formal education, whereas in the

- Page 291 and 292:

only bargaining tool to get money.

- Page 293 and 294:

Table 6. Tierra del Fuego Subinspec

- Page 295 and 296:

4. Police deaths during the 20th ce

- Page 297 and 298:

Of course, these conclusions depend

- Page 299 and 300:

“stop go” dynamics 4 ). In fact

- Page 301 and 302:

income distribution and earnings gr

- Page 303 and 304:

Figure 2. Basic Statistics Food Clo

- Page 305 and 306:

Table 2 Dep. Var.: Share of food Sm

- Page 307 and 308:

Figure 3. Variety in food retailing

- Page 309 and 310:

Table 3 Dep. Var.: Share of food at

- Page 311 and 312:

3.3 Income distribution effects The

- Page 313 and 314:

Figure 6. Individual Effects Using

- Page 315 and 316:

Expenditure Income 5000 6000 4000 4

- Page 317 and 318:

Figure 10. Income distribution Dens

- Page 319 and 320:

Appendix A: Estimation strategy Est

- Page 321 and 322:

w ijt where [ ln( 1+ ∏ ) − ln(

- Page 323 and 324:

2.2 Income distribution effects Fol

- Page 325 and 326:

Appendix B: The data To run our est

- Page 327 and 328:

Appendix C: Additional tables C1: B

- Page 329 and 330:

C3: Table 3 coefficients Dummy for

- Page 331 and 332:

CONCLUSION 20 th century Argentina

- Page 333 and 334:

can be harbingers of worse things t

- Page 335 and 336:

Ahumada, Hildegart, Alfredo Canaves

- Page 337 and 338:

Barro, Robert J. 2005. “Rare Even

- Page 339 and 340:

Burzaco, Eugenio et al. 2004. “Ma

- Page 341 and 342:

Cortés Conde, Roberto and María M

- Page 343 and 344:

Di Tella, Rafael, Juan Dubra and Ro

- Page 345 and 346:

Gaggero, Horacio and Alicia Garro.

- Page 347 and 348:

Gerchunoff, Pablo, Fernando Rocchi

- Page 349 and 350:

James, Daniel. 1988. “October 17

- Page 351 and 352:

Maddison, Angus. 2006. The World Ec

- Page 353 and 354:

Piketty, T. 2003. “Income Inequal

- Page 355 and 356:

Spiller, Pablo and Mariano Tommasi.

- Page 357:

Williamson, Jeffrey G. 1995. “The