English - DFDS

English - DFDS

English - DFDS

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

34 terminal services<br />

<strong>DFDS</strong> annual report 2009<br />

Markets, activities and customers<br />

The geographical region for <strong>DFDS</strong>’ Terminal services is dictated by<br />

the need to support the internal shipping business units. Each location<br />

is optimally placed to serve the lines in the most efficient and cost<br />

effective manner. <strong>DFDS</strong>’ objective is to create hubs with operation<br />

of several services to/from the same terminals, wherever possible,<br />

enabling customers to optimise their own resources and minimise<br />

their operational cost.<br />

<strong>DFDS</strong>’ main customer segments are: unit loads (trailers/containers),<br />

automotive, forest products, steel, chemicals and project cargo. It is the<br />

terminal’s purpose to support <strong>DFDS</strong>’ growth by providing first class,<br />

cost effective added value services such as: stevedoring, warehousing,<br />

car compounds, timber terminals, road/rail distribution, transhipments<br />

and project cargo solutions. The same services are to an increasing<br />

extent also offered to third-party customers.<br />

The terminal services are linked to <strong>DFDS</strong>’ shipping services by fully<br />

integrated IT systems, whereby customers are provided with seamless,<br />

tailor made IT solutions for their complete supply chains. Important<br />

success criteria for terminal operations include:<br />

n The efficient and safe processing of cargo<br />

n Understanding the industry and customer needs<br />

n Servicing several modes of transport<br />

n Added value activities<br />

n Contributing to the reduction of transit time and total lead time<br />

Market trends<br />

As a result of the high dependency on particularly own ro-ro volumes,<br />

the operation and profitability of Terminal Services follows the market<br />

trend for these shipping routes.<br />

As for the global economy, the market conditions in 2009 were<br />

very challenging for the shipping industry with a sudden decline in<br />

volumes starting in the last part of 2008 continuing into 2009. As a<br />

result, port terminals experienced insufficient capacity utilization and<br />

therefore commenced a process of reducing capacity and costs to<br />

match volumes. A first phase of this process was completed in mid<br />

2009 and resulted in development of terminal operations with higher<br />

levels of efficiency and a more flexible cost base.<br />

Concurrently long-term developments are expected to favour<br />

larger terminals, as there is an increasing demand for terminals with<br />

high levels of efficiency and through-flow. This is expected to lead<br />

to a gradual reduction in the number of smaller ports. In addition,<br />

higher volumes from fewer shipping companies, using larger ships, will<br />

increase the need for on-going productivity improvements in port<br />

terminals.<br />

Integration process<br />

The process of integrating the Terminal Services business unit’s activities<br />

began at the end of 2007. This integration is based on a joint business<br />

model that describes work processes and defines productivity targets.<br />

The model defines joint key operational data that form a basis<br />

for benchmarking of productivity and exchange knowledge and skills<br />

between terminals. This integration enables the organisation to evaluate<br />

new concepts, solutions and strategies, in order to meet increasing<br />

demands for productivity and thereby implement solutions which have<br />

resulted in a reduction in costs.<br />

Efficiency programme implemented in Immingham<br />

2009 was a turbulent year for Terminal Services, with volumes down<br />

on average by 25 % in the first half year, and up to 50 % in specific<br />

areas of activity such as Automotive, Steel and Timber.<br />

An extensive streamlining programme was initiated throughout,<br />

but with particular focus on the largest terminal at Immingham. As a<br />

result, the total workforce was reduced by 24 % against 2008, and cost<br />

as a percentage of turnover was reduced considerably.<br />

In the second half of the year the Immingham terminal experienced<br />

a relatively robust recovery in volumes, including record<br />

monthly volumes for both steel and automotive in the months of<br />

September and October. Employees have supported the efficiency<br />

and productivity measures positively and together with Management<br />

ensured the productivity gains were fully cemented.<br />

As ship’s sizes and capacity continue to increase, the role of port<br />

terminals became increasingly critical. <strong>DFDS</strong> will for these reasons<br />

continue to monitor and review all existing practises and capabilities,<br />

to deliver continued productivity and efficiency gains, cost reductions<br />

and improved performance.<br />

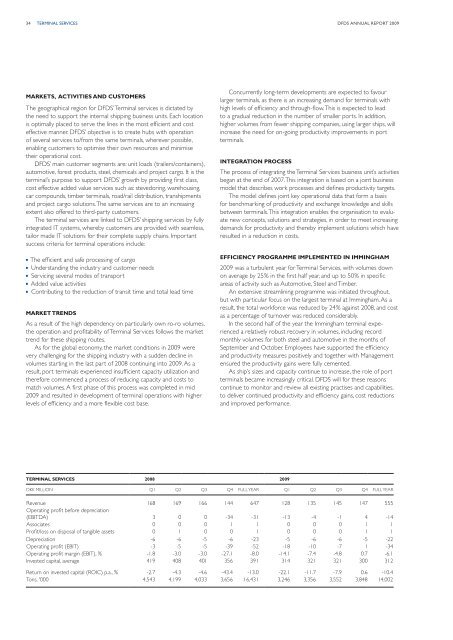

Terminal Services 2008 2009<br />

DKK miLLION Q1 Q2 Q3 Q4 FULL YEAR Q1 Q2 Q3 Q4 FULL YEAR<br />

Revenue 168 169 166 144 647 128 135 145 147 555<br />

Operating profit before depreciation<br />

(EBITDA) 3 0 0 -34 -31 -13 -4 -1 4 -14<br />

Associates 0 0 0 1 1 0 0 0 1 1<br />

Profit/loss on disposal of tangible assets 0 1 0 0 1 0 0 0 1 1<br />

Depreciation -6 -6 -5 -6 -23 -5 -6 -6 -5 -22<br />

Operating profit (EBIT) -3 -5 -5 -39 -52 -18 -10 -7 1 -34<br />

Operating profit margin (EBIT), % -1.8 -3.0 -3.0 -27.1 -8.0 -14.1 -7.4 -4.8 0.7 -6.1<br />

Invested capital, average 419 408 401 356 391 314 321 321 300 312<br />

Return on invested capital (ROIC) p.a., % -2.7 -4.3 -4.6 -43.4 -13.0 -22.1 -11.7 -7.9 0.6 -10.4<br />

Tons, '000 4,543 4,199 4,033 3,656 16,431 3,246 3,356 3,552 3,848 14,002