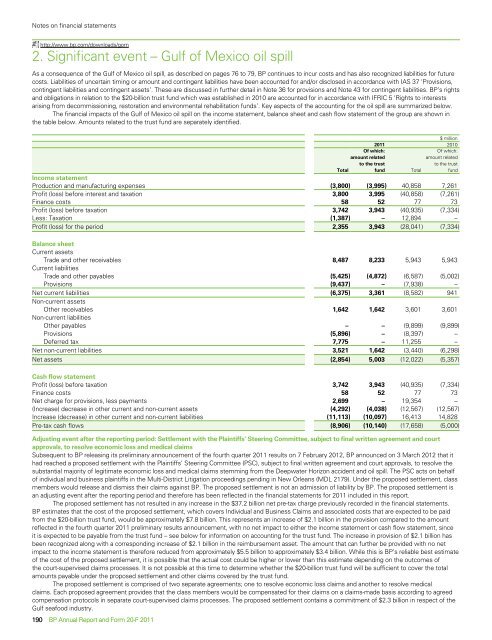

Notes on financial statementshttp://www.bp.com/downloads/gom2. Significant event – Gulf of Mexico oil spillAs a consequence of the Gulf of Mexico oil spill, as described on pages 76 to 79, <strong>BP</strong> continues to incur costs <strong>and</strong> has also recognized liabilities for futurecosts. Liabilities of uncertain timing or amount <strong>and</strong> contingent liabilities have been accounted for <strong>and</strong>/or disclosed in accordance with IAS 37 ‘Provisions,contingent liabilities <strong>and</strong> contingent assets’. These are discussed in further detail in Note 36 for provisions <strong>and</strong> Note 43 for contingent liabilities. <strong>BP</strong>’s rights<strong>and</strong> obligations in relation to the $<strong>20</strong>-billion trust fund which was established in <strong>20</strong>10 are accounted for in accordance with IFRIC 5 ‘Rights to interestsarising from decommissioning, restoration <strong>and</strong> environmental rehabilitation funds’. Key aspects of the accounting for the oil spill are summarized below.The financial impacts of the Gulf of Mexico oil spill on the income statement, balance sheet <strong>and</strong> cash flow statement of the group are shown inthe table below. Amounts related to the trust fund are separately identified.$ million<strong>20</strong>11 <strong>20</strong>10TotalOf which:amount relatedto the trustfundTotalOf which:amount relatedto the trustfundIncome statementProduction <strong>and</strong> manufacturing expenses (3,800) (3,995) 40,858 7,261Profit (loss) before interest <strong>and</strong> taxation 3,800 3,995 (40,858) (7,261)Finance costs 58 52 77 73Profit (loss) before taxation 3,742 3,943 (40,935) (7,334)Less: Taxation (1,387) – 12,894 –Profit (loss) for the period 2,355 3,943 (28,041) (7,334)Balance sheetCurrent assetsTrade <strong>and</strong> other receivables 8,487 8,233 5,943 5,943Current liabilitiesTrade <strong>and</strong> other payables (5,425) (4,872) (6,587) (5,002)Provisions (9,437) – (7,938) –Net current liabilities (6,375) 3,361 (8,582) 941Non-current assetsOther receivables 1,642 1,642 3,601 3,601Non-current liabilitiesOther payables – – (9,899) (9,899)Provisions (5,896) – (8,397) –Deferred tax 7,775 – 11,255 –Net non-current liabilities 3,521 1,642 (3,440) (6,298)Net assets (2,854) 5,003 (12,022) (5,357)Cash flow statementProfit (loss) before taxation 3,742 3,943 (40,935) (7,334)Finance costs 58 52 77 73Net charge for provisions, less payments 2,699 – 19,354 –(Increase) decrease in other current <strong>and</strong> non-current assets (4,292) (4,038) (12,567) (12,567)Increase (decrease) in other current <strong>and</strong> non-current liabilities (11,113) (10,097) 16,413 14,828Pre-tax cash flows (8,906) (10,140) (17,658) (5,000)Adjusting event after the reporting period: Settlement with the Plaintiffs’ Steering Committee, subject to final written agreement <strong>and</strong> courtapprovals, to resolve economic loss <strong>and</strong> medical claimsSubsequent to <strong>BP</strong> releasing its preliminary announcement of the fourth quarter <strong>20</strong>11 results on 7 February <strong>20</strong>12, <strong>BP</strong> announced on 3 March <strong>20</strong>12 that ithad reached a proposed settlement with the Plaintiffs’ Steering Committee (PSC), subject to final written agreement <strong>and</strong> court approvals, to resolve thesubstantial majority of legitimate economic loss <strong>and</strong> medical claims stemming from the Deepwater Horizon accident <strong>and</strong> oil spill. The PSC acts on behalfof individual <strong>and</strong> business plaintiffs in the Multi-District Litigation proceedings pending in New Orleans (MDL 2179). Under the proposed settlement, classmembers would release <strong>and</strong> dismiss their claims against <strong>BP</strong>. The proposed settlement is not an admission of liability by <strong>BP</strong>. The proposed settlement isan adjusting event after the reporting period <strong>and</strong> therefore has been reflected in the financial statements for <strong>20</strong>11 included in this report.The proposed settlement has not resulted in any increase in the $37.2 billion net pre-tax charge previously recorded in the financial statements.<strong>BP</strong> estimates that the cost of the proposed settlement, which covers Individual <strong>and</strong> Business Claims <strong>and</strong> associated costs that are expected to be paidfrom the $<strong>20</strong>-billion trust fund, would be approximately $7.8 billion. This represents an increase of $2.1 billion in the provision compared to the amountreflected in the fourth quarter <strong>20</strong>11 preliminary results announcement, with no net impact to either the income statement or cash flow statement, sinceit is expected to be payable from the trust fund – see below for information on accounting for the trust fund. The increase in provision of $2.1 billion hasbeen recognized along with a corresponding increase of $2.1 billion in the reimbursement asset. The amount that can further be provided with no netimpact to the income statement is therefore reduced from approximately $5.5 billion to approximately $3.4 billion. While this is <strong>BP</strong>’s reliable best estimateof the cost of the proposed settlement, it is possible that the actual cost could be higher or lower than this estimate depending on the outcomes ofthe court-supervised claims processes. It is not possible at this time to determine whether the $<strong>20</strong>-billion trust fund will be sufficient to cover the totalamounts payable under the proposed settlement <strong>and</strong> other claims covered by the trust fund.The proposed settlement is comprised of two separate agreements; one to resolve economic loss claims <strong>and</strong> another to resolve medicalclaims. Each proposed agreement provides that the class members would be compensated for their claims on a claims-made basis according to agreedcompensation protocols in separate court-supervised claims processes. The proposed settlement contains a commitment of $2.3 billion in respect of theGulf seafood industry.190 <strong>BP</strong> <strong>Annual</strong> <strong>Report</strong> <strong>and</strong> <strong>Form</strong> <strong>20</strong>-F <strong>20</strong>11

Notes on financial statementshttp://www.bp.com/downloads/gom2. Significant event – Gulf of Mexico oil spill continuedThe proposed economic loss settlement provides for a transition from the Gulf Coast Claims Facility (GCCF). A court-supervised transitional claimsprocess for economic loss claims will be in operation while the infrastructure for the new settlement claims process is put in place. During this transitionalperiod, the processing of claims that have been submitted to the GCCF will continue, <strong>and</strong> new claimants may submit their claims.Costs of the proposed settlement will be paid either from the $<strong>20</strong>-billion Trust or, should the Trust not be sufficient, directly by <strong>BP</strong>. At this time <strong>BP</strong>expects all claims to be paid from the Trust.The proposed settlement does not include claims against <strong>BP</strong> made by the United States Department of Justice or other federal agencies (includingunder the Clean Water Act <strong>and</strong> for Natural Resource Damages under the Oil Pollution Act) or by the states <strong>and</strong> local governments. The proposedsettlement also excludes certain other claims against <strong>BP</strong>, such as securities <strong>and</strong> shareholder claims pending in MDL 2185, <strong>and</strong> claims based solely on thedeepwater drilling moratorium <strong>and</strong>/or the related permitting process.The proposed settlement also provides that, to the extent permitted by law, <strong>BP</strong> will assign to the PSC certain of its claims, rights <strong>and</strong> recoveriesagainst Transocean <strong>and</strong> Halliburton for damages with protections such that Transocean <strong>and</strong> Halliburton cannot pass those damages through to <strong>BP</strong>.The proposed settlement is subject to reaching definitive <strong>and</strong> fully documented agreements within 45 days of 2 March <strong>20</strong>12. If those agreementsare not reached, either party has the right to terminate the proposed settlement. Once there are definitive <strong>and</strong> fully documented agreements, <strong>BP</strong> <strong>and</strong>the PSC would then seek the court’s preliminary approval of the settlement. Under US federal law, there is an established procedure for determining thefairness, reasonableness <strong>and</strong> adequacy of class action settlements. Pursuant to this procedure <strong>and</strong> subject to the court granting preliminary approval ofboth agreements, there would be an extensive outreach programme to the public to explain the settlement agreements, class members’ rights, includingthe right to ‘opt out’ of the classes, <strong>and</strong> the process of making claims. The court would then conduct fairness hearings at which class members <strong>and</strong>various other parties would have an opportunity to be heard <strong>and</strong> present evidence. The court would then decide whether or not to approve each proposedsettlement agreement.For further details of the proposed settlement see Legal proceedings on pages 160 to 164.Trust fundIn <strong>20</strong>10, <strong>BP</strong> established the Deepwater Horizon Oil Spill Trust (the Trust) to be funded in the amount of $<strong>20</strong> billion (the trust fund) over the period tothe fourth quarter of <strong>20</strong>13, which is available to satisfy legitimate individual <strong>and</strong> business claims administered by the Gulf Coast Claims Facility (GCCF),state <strong>and</strong> local government claims resolved by <strong>BP</strong>, final judgments <strong>and</strong> settlements, state <strong>and</strong> local response costs, <strong>and</strong> natural resource damages <strong>and</strong>related costs. In <strong>20</strong>10, <strong>BP</strong> contributed $5 billion to the fund, <strong>and</strong> further regular contributions totalling $5 billion were made in <strong>20</strong>11. During <strong>20</strong>11, <strong>BP</strong> alsocontributed the cash settlements received from MOEX, Weatherford <strong>and</strong> Anadarko, amounting in total to $5.1 billion. A further cash settlement fromCameron was received in January <strong>20</strong>12 <strong>and</strong> was also contributed to the trust fund. As a result of these accelerated contributions, it is now expected thatthe $<strong>20</strong>-billion commitment will have been paid in full by the end of <strong>20</strong>12. The income statement charge for <strong>20</strong>10 included $<strong>20</strong> billion in relation to thetrust fund, adjusted to take account of the time value of money. Fines, penalties <strong>and</strong> claims administration costs are not covered by the trust fund. Theestablishment of the trust fund does not represent a cap or floor on <strong>BP</strong>’s liabilities <strong>and</strong> <strong>BP</strong> does not admit to a liability of this amount.Under the terms of the Trust agreement, <strong>BP</strong> has no right to access the funds once they have been contributed to the trust fund <strong>and</strong> <strong>BP</strong>has no decision-making role in connection with the payment by the trust fund of individual <strong>and</strong> business claims resolved by the GCCF <strong>and</strong> the newcourt‐supervised claims processes referred to below. <strong>BP</strong> will receive funds from the trust fund only upon its expiration, if there are any funds remainingat that point. Any amount remaining in the trust fund when the trustees determine that all claims have been settled would be returned to <strong>BP</strong>. However,it is not possible to reliably estimate the number or total amount of the claims that will be settled from the trust fund, <strong>and</strong> therefore it is not possible toreliably measure the fair value of <strong>BP</strong>’s residual interest in it. The carrying amount of <strong>BP</strong>’s residual interest is, consequently, nil. <strong>BP</strong> has the authority underthe Trust agreement to present certain resolved claims, including natural resource damages claims <strong>and</strong> state <strong>and</strong> local response claims, to the Trust forpayment, by providing the trustees with all the required documents establishing that such claims are valid under the Trust agreement. However, any suchpayments can only be made on the authority of the Trustee <strong>and</strong> any funds distributed are paid directly to the claimants, not to <strong>BP</strong>. <strong>BP</strong> will not settle anysuch items directly or receive reimbursement from the trust fund for such items.The proposed settlement with the PSC announced on 3 March <strong>20</strong>12 provides for a transition from the GCCF. A court-supervised transitional claimsprocess for economic loss claims will be in operation while the infrastructure for the new settlement claims process is put in place. During this transitionalperiod, the processing of claims that have been submitted to the GCCF will continue, <strong>and</strong> new claimants may submit their claims. <strong>BP</strong> has agreed not towait for final approval of the economic loss settlement before claims are paid. The economic loss claims process will continue under court supervisionbefore final approval of the settlement, first under the transitional claims process, <strong>and</strong> then through the settlement claims process established by theproposed economic loss settlement.The Trust will remain in place, unaffected by the proposed settlement <strong>and</strong> the transition from the GCCF to the new court-supervised claims processes.<strong>BP</strong>’s obligation to make contributions to the trust fund was recognized in full in <strong>20</strong>10, amounting to $<strong>20</strong> billion on an undiscounted basis as itis committed to making these contributions. On initial recognition the discounted amount recognized was $19,580 million. After <strong>BP</strong>’s contributionsof $15,140 million to the trust fund during <strong>20</strong>10 <strong>and</strong> <strong>20</strong>11, <strong>and</strong> adjustments for discounting, the remaining liability as at 31 December <strong>20</strong>11 was$4,872 million. This liability is recorded within current other payables on the balance sheet, <strong>and</strong> is expected to be paid in full before the end of <strong>20</strong>12.The table below shows movements in the funding obligation during the period to 31 December <strong>20</strong>11.$ million<strong>20</strong>11 <strong>20</strong>10At 1 January 14,901 –Trust fund liability initially recognized – discounted – 19,580Unwinding of discount 52 73Change in discounting 43 240Contributions (10,140) (5,000)Other 16 8At 31 December 4,872 14,901Of which – current 4,872 5,002– non-current – 9,899Financial statementsAn asset has been recognized representing <strong>BP</strong>’s right to receive reimbursement from the trust fund. This is the portion of the estimated futureexpenditure provided for that will be settled by payments from the trust fund. We use the term ’reimbursement asset‘ to describe this asset. <strong>BP</strong> will notactually receive any reimbursements from the trust fund, instead payments will be made directly to claimants from the trust fund, <strong>and</strong> <strong>BP</strong> will be releasedfrom its corresponding obligation.<strong>BP</strong> <strong>Annual</strong> <strong>Report</strong> <strong>and</strong> <strong>Form</strong> <strong>20</strong>-F <strong>20</strong>11 191

- Page 2 and 3:

Cover imagePhotograph of DeepseaSta

- Page 4 and 5:

Cross reference to Form 20-FPageIte

- Page 6 and 7:

Miscellaneous termsIn this document

- Page 8 and 9:

6 BP Annual Report and Form 20-F 20

- Page 10:

Chairman’s letterCarl-Henric Svan

- Page 13 and 14:

During the year, the remuneration c

- Page 15 and 16:

Business review: Group overviewBP A

- Page 17 and 18:

SafetyDuring the year, we reorganiz

- Page 19 and 20:

In Refining and Marketing, our worl

- Page 21 and 22:

Crude oil and gas prices,and refini

- Page 23:

In detailFor more information, seeR

- Page 26 and 27:

Our market: Longer-term outlookThe

- Page 29 and 30:

BP’s distinctive capabilities and

- Page 31 and 32:

Technology will continue to play a

- Page 33 and 34:

In detailFor more information,see C

- Page 35 and 36:

In detailFind out more online.bp.co

- Page 37 and 38:

BP Annual Report and Form 20-F 2011

- Page 39 and 40:

Below BP has asignificant presencei

- Page 41 and 42:

What you can measure6 Active portfo

- Page 43 and 44:

Business review: Group overview2012

- Page 45 and 46:

Our risk management systemOur enhan

- Page 47 and 48:

Our current strategic priorities ar

- Page 49 and 50:

Our performance2011 was a year of f

- Page 51 and 52:

Left BP employeesat work in Prudhoe

- Page 53 and 54:

We continued to sell non-core asset

- Page 55 and 56:

Reported recordableinjury frequency

- Page 57 and 58:

Business reviewBP in more depth56 F

- Page 59 and 60:

Business reviewThe primary addition

- Page 61 and 62:

Business reviewRisk factorsWe urge

- Page 63 and 64:

Business review2010. Similar action

- Page 65 and 66:

Business reviewBusiness continuity

- Page 67:

Business reviewSafetyOver the past

- Page 70:

Business reviewour review of all th

- Page 73 and 74:

Business reviewGreenhouse gas regul

- Page 75 and 76:

Business reviewresources such as dr

- Page 77 and 78:

Business reviewExploration and Prod

- Page 79 and 80:

Business reviewCompleting the respo

- Page 81 and 82:

Business reviewgrants, which were s

- Page 83 and 84:

Business reviewOur performanceKey s

- Page 85 and 86:

Business reviewwere in Russia (Oren

- Page 87 and 88:

Business reviewCanadaIn Canada, BP

- Page 89 and 90:

Business review• In March 2011, T

- Page 91 and 92:

Business reviewaccess advantageous

- Page 93 and 94:

Business reviewBP’s vice presiden

- Page 95 and 96:

Business reviewhttp://www.bp.com/do

- Page 97 and 98:

Business reviewbalance of participa

- Page 99 and 100:

Business reviewAcquisitions and dis

- Page 101 and 102:

Business reviewLPGOur global LPG ma

- Page 103 and 104:

Business reviewOther businesses and

- Page 105 and 106:

Business reviewLiquidity and capita

- Page 107 and 108:

Business reviewThe group expects it

- Page 109 and 110:

Business reviewFrequently, work (in

- Page 111 and 112:

Business reviewHazardous and Noxiou

- Page 113 and 114:

Business reviewpart of a larger por

- Page 115 and 116:

Directors andsenior management114 D

- Page 117 and 118:

Directors and senior managementDire

- Page 119 and 120:

Directors and senior managementH L

- Page 121 and 122:

Corporate governanceCorporate gover

- Page 123 and 124:

Corporate governanceAntony Burgmans

- Page 125 and 126:

Corporate governanceBoard oversight

- Page 127 and 128:

Corporate governanceBoard and commi

- Page 129 and 130:

Corporate governancefinancial repor

- Page 131 and 132:

Corporate governancechairs and secr

- Page 133 and 134:

Corporate governance• Oversee GCR

- Page 135 and 136:

Corporate governanceCommittee’s r

- Page 137 and 138:

Corporate governanceControls and pr

- Page 139 and 140:

Corporate governanceThe Act require

- Page 141 and 142: Directors’ remuneration reportRem

- Page 143 and 144: Directors’ remuneration reportSum

- Page 145 and 146: Directors’ remuneration reportSaf

- Page 147 and 148: Directors’ remuneration reportRem

- Page 149 and 150: Directors’ remuneration reportThe

- Page 151 and 152: Directors’ remuneration reportSha

- Page 153 and 154: Directors’ remuneration reportNon

- Page 155 and 156: Additional informationfor sharehold

- Page 157 and 158: Additional information for sharehol

- Page 159 and 160: Additional information for sharehol

- Page 161 and 162: Additional information for sharehol

- Page 163 and 164: Additional information for sharehol

- Page 165 and 166: Additional information for sharehol

- Page 167 and 168: Additional information for sharehol

- Page 169 and 170: Additional information for sharehol

- Page 171 and 172: Additional information for sharehol

- Page 173 and 174: Additional information for sharehol

- Page 175 and 176: Financial statements174 Statement o

- Page 177 and 178: Consolidated financial statements o

- Page 179 and 180: Consolidated financial statements o

- Page 181 and 182: Consolidated financial statements o

- Page 183 and 184: Consolidated financial statements o

- Page 185 and 186: Notes on financial statements1. Sig

- Page 187 and 188: Notes on financial statements1. Sig

- Page 189 and 190: Notes on financial statements1. Sig

- Page 191: Notes on financial statements1. Sig

- Page 195 and 196: Notes on financial statementshttp:/

- Page 197 and 198: Notes on financial statements3. Bus

- Page 199 and 200: Notes on financial statements5. Dis

- Page 201 and 202: Notes on financial statements5. Dis

- Page 203 and 204: Notes on financial statementshttp:/

- Page 205 and 206: Notes on financial statementshttp:/

- Page 207 and 208: Notes on financial statements7. Int

- Page 209 and 210: Notes on financial statements10. Im

- Page 211 and 212: Notes on financial statements15. Ex

- Page 213 and 214: Notes on financial statementshttp:/

- Page 215 and 216: Notes on financial statementshttp:/

- Page 217 and 218: Notes on financial statementshttp:/

- Page 219 and 220: Notes on financial statements26. Fi

- Page 221 and 222: Notes on financial statements26. Fi

- Page 223 and 224: Notes on financial statements26. Fi

- Page 225 and 226: Notes on financial statements29. Tr

- Page 227 and 228: Notes on financial statements33. De

- Page 229 and 230: Notes on financial statements33. De

- Page 231 and 232: Notes on financial statements34. Fi

- Page 233 and 234: Notes on financial statementshttp:/

- Page 235 and 236: Notes on financial statements36. Pr

- Page 237 and 238: Notes on financial statements37. Pe

- Page 239 and 240: Notes on financial statements37. Pe

- Page 241 and 242: Notes on financial statements37. Pe

- Page 243 and 244:

Notes on financial statements38. Ca

- Page 245 and 246:

Notes on financial statementsTotal

- Page 247 and 248:

Notes on financial statements39. Ca

- Page 249 and 250:

Notes on financial statements40. Sh

- Page 251 and 252:

Notes on financial statements42. Re

- Page 253 and 254:

Notes on financial statements45. Su

- Page 255 and 256:

Notes on financial statements46. Co

- Page 257 and 258:

Notes on financial statements46. Co

- Page 259:

Notes on financial statements46. Co

- Page 262 and 263:

Supplementary information on oil an

- Page 264 and 265:

Supplementary information on oil an

- Page 266 and 267:

Supplementary information on oil an

- Page 268 and 269:

Supplementary information on oil an

- Page 270 and 271:

Supplementary information on oil an

- Page 272 and 273:

Supplementary information on oil an

- Page 274 and 275:

Supplementary information on oil an

- Page 276 and 277:

Supplementary information on oil an

- Page 278 and 279:

Supplementary information on oil an

- Page 280 and 281:

Supplementary information on oil an

- Page 282 and 283:

Supplementary information on oil an

- Page 284 and 285:

SignaturesThe registrant hereby cer

- Page 286 and 287:

Parent company financial statements

- Page 288 and 289:

Parent company financial statements

- Page 290 and 291:

Parent company financial statements

- Page 292 and 293:

Parent company financial statements

- Page 294 and 295:

Parent company financial statements

- Page 296 and 297:

Parent company financial statements

- Page 298 and 299:

Parent company financial statements