- Page 1 and 2:

EN2008EUROPEAN CENTRAL BANK ANNUAL

- Page 3 and 4:

© European Central Bank, 2009Addre

- Page 5 and 6:

CHAPTER 4FINANCIAL STABILITY AND IN

- Page 7 and 8:

7 Statistical accounting consequenc

- Page 9:

ABBREVIATIONSCOUNTRIESOTHERSBE Belg

- Page 12 and 13:

in the course of the year, in line

- Page 14 and 15:

currencies, T2S will be a major ste

- Page 16 and 17:

CHAPTER 1ECONOMICDEVELOPMENTS ANDMO

- Page 18 and 19:

Chart 1 ECB interest rates and mone

- Page 20 and 21: Despite moderating, the annual grow

- Page 22 and 23: substantial downward revisions in r

- Page 24 and 25: in July, annual inflation in the OE

- Page 26 and 27: As regards the Chinese economy, rea

- Page 28 and 29: generally tighter financing conditi

- Page 30 and 31: were recorded in December, but thes

- Page 32 and 33: was driven mainly by developments i

- Page 34 and 35: market tensions, particularly for l

- Page 36 and 37: anking and financial system. At the

- Page 38 and 39: cash flows to compensate for a redu

- Page 40 and 41: quarter of 2008 and -0.1% in Decemb

- Page 42 and 43: whereby investors’ uncertainty su

- Page 44 and 45: September onwards, amid the great u

- Page 46 and 47: Chart C Trading volumes for governm

- Page 48 and 49: sponsored rescue plans were initiat

- Page 50 and 51: The annual growth rate of consumer

- Page 52 and 53: end of 2007. By December 2008 this

- Page 54 and 55: calculated as the balance between g

- Page 56 and 57: commodity prices (see Box 4). Conve

- Page 58 and 59: Chart D Longer-term inflation expec

- Page 60 and 61: apidly to 1.7% in December, mainly

- Page 62 and 63: productivity slowed to 0.2% in the

- Page 64 and 65: Table 3 Composition of real GDP gro

- Page 66 and 67: Corporate investment, which had exp

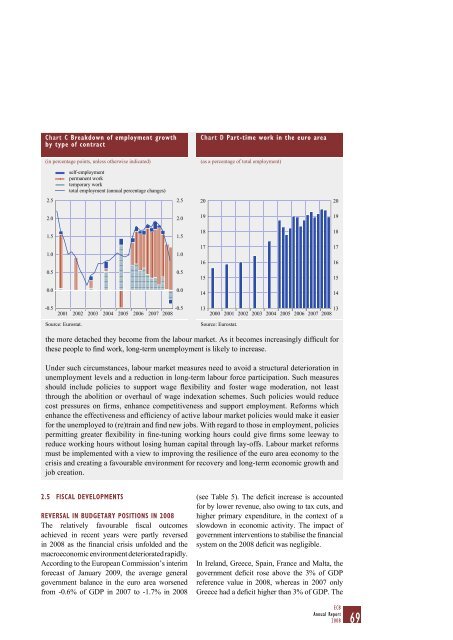

- Page 68 and 69: Box 5LABOUR MARKET DEVELOPMENTS IN

- Page 72 and 73: Box 6DEVELOPMENTS IN THE ISSUANCE A

- Page 74 and 75: Chart B Government bond yield sprea

- Page 76 and 77: Box 7STATISTICAL ACCOUNTING CONSEQU

- Page 78 and 79: warranted because of the need to co

- Page 80 and 81: sharp depreciation of the euro was

- Page 82 and 83: prices in the first eight months of

- Page 84 and 85: focused more on the production rath

- Page 86 and 87: segments and, in turn, affected eur

- Page 88 and 89: and Bulgaria registered robust grow

- Page 90 and 91: In the remaining non-euro area EU c

- Page 92 and 93: Estonian kroon and the Lithuanian l

- Page 94 and 95: Table 10 Official monetary policy s

- Page 96 and 97: the Bank of England and Sveriges Ri

- Page 98 and 99: CHAPTER 2CENTRAL BANKOPERATIONSAND

- Page 100 and 101: Box 10MONETARY POLICY OPERATIONS DU

- Page 102 and 103: Chart A Liquidity supply through op

- Page 104 and 105: franc funding needs of banks with n

- Page 106 and 107: MINIMUM RESERVE SYSTEMCredit instit

- Page 108 and 109: with the ample allotments in the fi

- Page 110 and 111: 2008. By contrast, the average shar

- Page 112 and 113: and SDR holdings increased by aroun

- Page 114 and 115: and the ECB). As a result of carefu

- Page 116 and 117: cross-CSD settlement. T2S will thus

- Page 118 and 119: ELIGIBLE LINKS BETWEEN NATIONAL SEC

- Page 120 and 121:

Chart 48 Number of euro banknotes i

- Page 122 and 123:

3.3 BANKNOTE PRODUCTION AND ISSUANC

- Page 124 and 125:

4 STATISTICSThe ECB, assisted by th

- Page 126 and 127:

iii) payments statistics and iv) de

- Page 128 and 129:

5 ECONOMIC RESEARCHThe main functio

- Page 130 and 131:

were organised to disseminate resea

- Page 132 and 133:

the Financial Collateral Directive,

- Page 134 and 135:

on the Banque centrale du Luxembour

- Page 136 and 137:

standards by individual Eurosystem

- Page 138 and 139:

CHAPTER 3ENTRY OF SLOVAKIAINTO THE

- Page 140 and 141:

Table 13 Main economic indicators f

- Page 142 and 143:

As of January 2009 Slovakia is thus

- Page 144 and 145:

3 OPERATIONAL ASPECTS OF THE INTEGR

- Page 146 and 147:

4 THE CASH CHANGEOVER IN SLOVAKIATH

- Page 149 and 150:

Willem F. Duisenberg accepting the

- Page 151 and 152:

1 FINANCIAL STABILITYThe Eurosystem

- Page 153 and 154:

With regard to merger and acquisiti

- Page 155 and 156:

with the principles set out in Octo

- Page 157 and 158:

2.2 BANKINGCAPITAL REQUIREMENTS DIR

- Page 159 and 160:

3 FINANCIAL INTEGRATIONThe Eurosyst

- Page 161 and 162:

The market for short-term paper in

- Page 163 and 164:

de France and the Banca d’Italia.

- Page 165 and 166:

and the Eurosystem’s business con

- Page 167 and 168:

4.2 RETAIL PAYMENT SYSTEMS ANDINSTR

- Page 169 and 170:

for Clearing and Settlement, and th

- Page 171 and 172:

Willem F. Duisenberg at his farewel

- Page 173 and 174:

1 EUROPEAN ISSUESIn 2008 the ECB co

- Page 175 and 176:

for financial institutions, to faci

- Page 177 and 178:

1.3 DEVELOPMENTS IN AND RELATIONS W

- Page 179 and 180:

On a number of occasions in 2008, t

- Page 181 and 182:

countries have voiced support for t

- Page 183 and 184:

Former Italian President Carlo Azeg

- Page 185 and 186:

1 ACCOUNTABILITY VIS-À-VIS THE GEN

- Page 187:

implementation of the steps foresee

- Page 190 and 191:

CHAPTER 7EXTERNALCOMMUNICATION

- Page 192 and 193:

2 COMMUNICATION ACTIVITIESThe ECB a

- Page 195 and 196:

Panel at the Fifth ECB Central Bank

- Page 197 and 198:

1 DECISION-MAKING BODIES AND CORPOR

- Page 199 and 200:

Council decided on the main aspects

- Page 201 and 202:

1.3 THE EXECUTIVE BOARDThe Executiv

- Page 203 and 204:

1.4 THE GENERAL COUNCILThe General

- Page 205 and 206:

The Eurosystem/ESCB committees have

- Page 207 and 208:

members of the Executive Board. 13

- Page 209 and 210:

for their current position. On the

- Page 211 and 212:

statistical office (Statistisches B

- Page 213 and 214:

4 ANNUAL ACCOUNTS OF THE ECB212 ECB

- Page 215 and 216:

function, and by the Governing Coun

- Page 217 and 218:

BALANCE SHEET AS AT 31 DECEMBER 200

- Page 219 and 220:

PROFIT AND LOSS ACCOUNT FOR THE YEA

- Page 221 and 222:

mid-market prices on 30 December 20

- Page 223 and 224:

The defined benefit obligation is c

- Page 225 and 226:

NOTES ON THE BALANCE SHEET1 GOLD AN

- Page 227 and 228:

Eurosystem (see “Banknotes in cir

- Page 229 and 230:

(see “Banknotes in circulation”

- Page 231 and 232:

values at which the transactions we

- Page 233 and 234:

15 CAPITAL AND RESERVESCAPITALPursu

- Page 235 and 236:

epresenting the remainder of its ca

- Page 237 and 238:

NOTES ON THE PROFIT AND LOSS ACCOUN

- Page 239:

individual circumstances. Basic sal

- Page 243 and 244:

5 CONSOLIDATED BALANCE SHEET OF THE

- Page 246 and 247:

ANNEXES

- Page 248 and 249:

Number Title OJ referenceECB/2008/1

- Page 250 and 251:

Number Title OJ referenceECB/2009/1

- Page 252 and 253:

Number 2 Originator SubjectCON/2008

- Page 254 and 255:

Number 2 Originator SubjectCON/2008

- Page 256 and 257:

Number 2 Originator SubjectCON/2009

- Page 258 and 259:

Number 4 Originator Subject OJ refe

- Page 260 and 261:

oth the marginal lending facility a

- Page 262 and 263:

OVERVIEW OF THE ECB’S COMMUNICATI

- Page 264 and 265:

y the respective NCBs will also be

- Page 266 and 267:

OPEN MARKET OPERATIONS BY CURRENCYE

- Page 268 and 269:

USD operationsType oftransaction 1)

- Page 270 and 271:

DOCUMENTS PUBLISHED BY THEEUROPEAN

- Page 272 and 273:

95 “Financial stability challenge

- Page 274 and 275:

1012 “Petrodollars and imports of

- Page 276 and 277:

GLOSSARYThis glossary contains sele

- Page 278 and 279:

Economic analysis: one pillar of th

- Page 280 and 281:

Financial stability: condition in w

- Page 282 and 283:

MFIs (monetary financial institutio

- Page 284 and 285:

Reserve base: the sum of the eligib

![KNOW YOUR NEW GIBRALTAR BANKNOTES - [Home] bThe/b](https://img.yumpu.com/50890985/1/184x260/know-your-new-gibraltar-banknotes-home-bthe-b.jpg?quality=85)

![PAPUA NEW GUINEA - [Home] - Polymer Bank Notes of the World](https://img.yumpu.com/49758743/1/190x143/papua-new-guinea-home-polymer-bank-notes-of-the-world.jpg?quality=85)