Crop Insurance as a Risk Management Strategy in Bangladesh

Crop Insurance as a Risk Management Strategy in Bangladesh

Crop Insurance as a Risk Management Strategy in Bangladesh

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

% of farmer<br />

% of farmer<br />

% of farmer<br />

100<br />

80<br />

60<br />

40<br />

20<br />

0<br />

100<br />

80<br />

60<br />

40<br />

20<br />

0<br />

100<br />

80<br />

60<br />

40<br />

20<br />

0<br />

Gondymari - le<strong>as</strong>t vulnerable<br />

Bank Loan NGO & Micro<br />

Credit<br />

Loan from<br />

Local<br />

Mohajon<br />

Mode of Self Reliance after<br />

Dis<strong>as</strong>ter<br />

Bank Loan NGO & Micro<br />

Credit<br />

Loan from<br />

Local<br />

Mohajon<br />

Mode of Self Reliance after<br />

Dis<strong>as</strong>ter<br />

91<br />

high<br />

Sh<strong>in</strong>gmari - moderate moderately vulnerable<br />

high<br />

Purb<strong>as</strong>ardubi - highly vulnerable<br />

Bank Loan NGO & Micro<br />

Credit<br />

Loan from<br />

Local<br />

Mohajon<br />

Mode of Self Reliance after<br />

Dis<strong>as</strong>ter<br />

high<br />

high<br />

medium<br />

low<br />

low<br />

medium<br />

Income level<br />

low<br />

medium<br />

medium<br />

high<br />

medium<br />

low<br />

Income level<br />

high<br />

medium<br />

low<br />

low<br />

Income level<br />

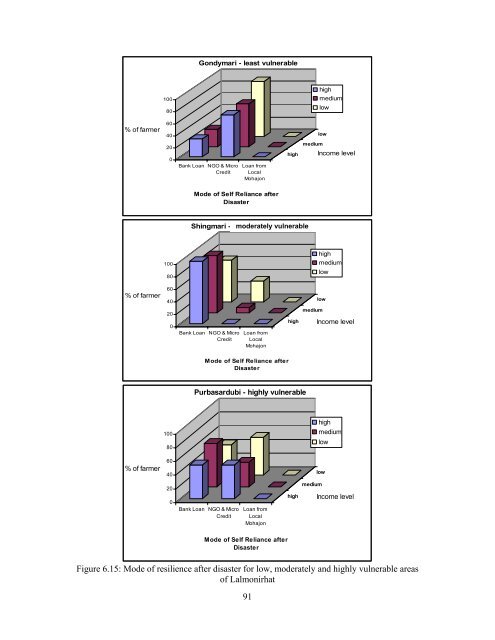

Figure 6.15: Mode of resilience after dis<strong>as</strong>ter for low, moderately and highly vulnerable are<strong>as</strong><br />

of Lalmonirhat