Untitled - Centro de Estudios Tributarios de la Universidad de Chile

Untitled - Centro de Estudios Tributarios de la Universidad de Chile

Untitled - Centro de Estudios Tributarios de la Universidad de Chile

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

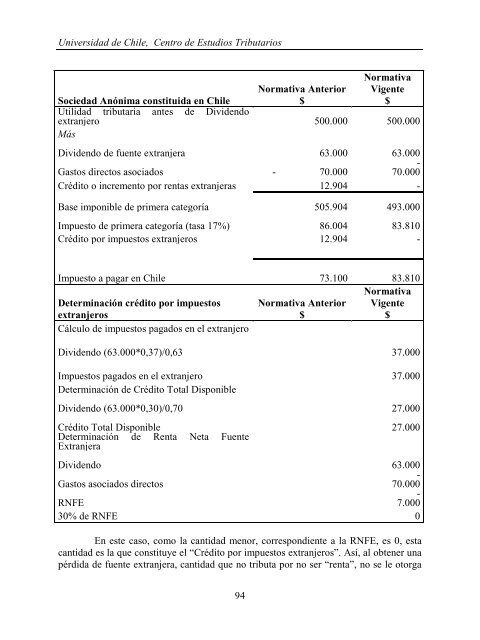

<strong>Universidad</strong> <strong>de</strong> <strong>Chile</strong>, <strong>Centro</strong> <strong>de</strong> <strong>Estudios</strong> <strong>Tributarios</strong><br />

Sociedad Anónima constituida en <strong>Chile</strong><br />

Normativa Anterior<br />

$<br />

Utilidad tributaria<br />

extranjero<br />

Más<br />

antes <strong>de</strong> Divi<strong>de</strong>ndo<br />

500.000<br />

94<br />

Normativa<br />

Vigente<br />

$<br />

500.000<br />

Divi<strong>de</strong>ndo <strong>de</strong> fuente extranjera<br />

Gastos directos asociados<br />

63.000<br />

- 70.000<br />

63.000<br />

-<br />

70.000<br />

Crédito o incremento por rentas extranjeras 12.904 -<br />

Base imponible <strong>de</strong> primera categoría 505.904<br />

493.000<br />

Impuesto <strong>de</strong> primera categoría (tasa 17%) 86.004 83.810<br />

Crédito por impuestos extranjeros 12.904 -<br />

Impuesto a pagar en <strong>Chile</strong> 73.100<br />

Determinación crédito por impuestos<br />

extranjeros<br />

Cálculo <strong>de</strong> impuestos pagados en el extranjero<br />

Divi<strong>de</strong>ndo (63.000*0,37)/0,63<br />

Impuestos pagados en el extranjero<br />

Determinación <strong>de</strong> Crédito Total Disponible<br />

Divi<strong>de</strong>ndo (63.000*0,30)/0,70<br />

Crédito Total Disponible<br />

Determinación<br />

Extranjera<br />

<strong>de</strong> Renta Neta Fuente<br />

Normativa Anterior<br />

$<br />

83.810<br />

Normativa<br />

Vigente<br />

$<br />

37.000<br />

37.000<br />

27.000<br />

27.000<br />

Divi<strong>de</strong>ndo<br />

Gastos asociados directos<br />

RNFE<br />

63.000<br />

-<br />

70.000<br />

-<br />

7.000<br />

30% <strong>de</strong> RNFE 0<br />

En este caso, como <strong>la</strong> cantidad menor, correspondiente a <strong>la</strong> RNFE, es 0, esta<br />

cantidad es <strong>la</strong> que constituye el “Crédito por impuestos extranjeros”. Así, al obtener una<br />

pérdida <strong>de</strong> fuente extranjera, cantidad que no tributa por no ser “renta”, no se le otorga