Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

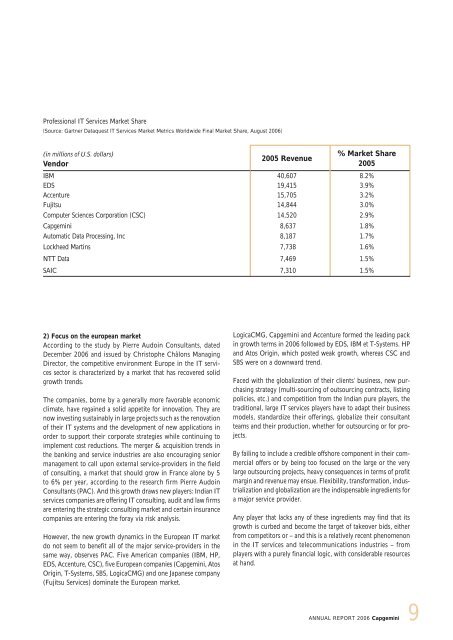

Professional IT Services Market Share<br />

(Source: Gartner Dataquest IT Services Market Metrics Worldwide Final Market Share, August 2006)<br />

(in millions of U.S. dollars)<br />

Vendor<br />

2005 Revenue<br />

% Market Share<br />

2005<br />

IBM 40,607 8.2%<br />

EDS 19,415 3.9%<br />

Accenture 15,705 3.2%<br />

Fujitsu 14,844 3.0%<br />

Computer Sciences Corporation (CSC) 14,520 2.9%<br />

<strong>Capgemini</strong> 8,637 1.8%<br />

Automatic Data Processing, Inc 8,187 1.7%<br />

Lockheed Martins 7,738 1.6%<br />

NTT Data 7,469 1.5%<br />

SAIC 7,310 1.5%<br />

2) Focus on the european market<br />

According to the study by Pierre Audoin Consultants, dated<br />

December 2006 and issued by Christophe Châlons Managing<br />

Director, the competitive environment Europe in the IT services<br />

sector is characterized by a market that has recovered solid<br />

growth trends.<br />

The companies, borne by a generally more favorable economic<br />

climate, have regained a solid appetite for innovation. They are<br />

now investing sustainably in large projects such as the renovation<br />

of their IT systems and the development of new applications in<br />

order to support their corporate strategies while continuing to<br />

implement cost reductions. The merger & acquisition trends in<br />

the banking and service industries are also encouraging senior<br />

management to call upon external service-providers in the field<br />

of consulting, a market that should grow in France alone by 5<br />

to 6% per year, according to the research firm Pierre Audoin<br />

Consultants (PAC). And this growth draws new players: Indian IT<br />

services companies are offering IT consulting, audit and law firms<br />

are entering the strategic consulting market and certain insurance<br />

companies are entering the foray via risk analysis.<br />

However, the new growth dynamics in the European IT market<br />

do not seem to benefit all of the major service-providers in the<br />

same way, observes PAC. Five American companies (IBM, HP,<br />

EDS, Accenture, CSC), five European companies (<strong>Capgemini</strong>, Atos<br />

Origin, T-Systems, SBS, LogicaCMG) and one Japanese company<br />

(Fujitsu Services) dominate the European market.<br />

LogicaCMG, <strong>Capgemini</strong> and Accenture formed the leading pack<br />

in growth terms in 2006 followed by EDS, IBM et T-Systems. HP<br />

and Atos Origin, which posted weak growth, whereas CSC and<br />

SBS were on a downward trend.<br />

Faced with the globalization of their clients’ business, new purchasing<br />

strategy (multi-sourcing of outsourcing contracts, listing<br />

policies, etc.) and competition from the Indian pure players, the<br />

traditional, large IT services players have to adapt their business<br />

models, standardize their offerings, globalize their consultant<br />

teams and their production, whether for outsourcing or for projects.<br />

By failing to include a credible offshore component in their commercial<br />

offers or by being too focused on the large or the very<br />

large outsourcing projects, heavy consequences in terms of profit<br />

margin and revenue may ensue. Flexibility, transformation, industrialization<br />

and globalization are the indispensable ingredients for<br />

a major service provider.<br />

Any player that lacks any of these ingredients may find that its<br />

growth is curbed and become the target of takeover bids, either<br />

from competitors or – and this is a relatively recent phenomenon<br />

in the IT services and telecommunications industries – from<br />

players with a purely financial logic, with considerable resources<br />

at hand.<br />

ANNUAL REPORT 2006 <strong>Capgemini</strong><br />

9