- Page 1 and 2:

This document comprises a prospectu

- Page 3 and 4:

SUMMARY INFORMATIONThis summary mus

- Page 5 and 6:

Summary Consolidated Income Stateme

- Page 7 and 8:

Summary Consolidated Cash Flow Stat

- Page 9 and 10:

Production from the Zapadno Chumpas

- Page 11 and 12:

Given the geographic spread of the

- Page 13 and 14:

RISK FACTORSAny investment in the O

- Page 15 and 16:

wells may change as a result of low

- Page 17 and 18:

which could have a materially adver

- Page 19 and 20:

Failure to obtain additional financ

- Page 21 and 22:

contractual or pricing terms, both

- Page 23 and 24:

years. In addition, since December

- Page 25 and 26:

UgandaUganda is among the poorest c

- Page 27 and 28:

Market Price of the Ordinary Shares

- Page 29 and 30:

DIRECTORS, CORPORATE SECRETARY, SEN

- Page 31 and 32:

EXPECTED TIMETABLE OF PRINCIPAL EVE

- Page 33 and 34:

CurrenciesAll references in this do

- Page 35 and 36:

PART I—INFORMATION ON THE GROUPOV

- Page 37 and 38:

Strong management and technical tea

- Page 39 and 40:

the availability of existing infras

- Page 41 and 42:

In 2005, the Group acquired a 95 pe

- Page 43 and 44:

The Group acquired a 10 per cent. i

- Page 45 and 46:

The Group is the operator and has a

- Page 47 and 48:

exploration wells. The total estima

- Page 49 and 50:

The Group has also entered into a s

- Page 51 and 52:

Pakistan has current proved hydroca

- Page 53 and 54:

operational by drawing up an Enviro

- Page 55 and 56:

Mr. Buckingham has never had any as

- Page 57 and 58:

Date2007 ........ On 18 January 200

- Page 59 and 60:

(3) One common share of Heritage Ho

- Page 61 and 62:

(f) General Sir Michael WilkesGener

- Page 63 and 64:

Remuneration CommitteeThe Remunerat

- Page 65 and 66:

Goldsworth House, Denton Way, Golds

- Page 67 and 68:

ResourcesA summary of the gross Con

- Page 69 and 70:

The post tax Net Present Value (NPV

- Page 71 and 72: RPS EnergyHeritage Oil - Competent

- Page 73 and 74: RPS EnergyHeritage Oil - Competent

- Page 75 and 76: RPS EnergyHeritage Oil - Competent

- Page 77 and 78: RPS EnergyHeritage Oil - Competent

- Page 79 and 80: RPS EnergyHeritage Oil - Competent

- Page 81 and 82: RPS EnergyHeritage Oil - Competent

- Page 83 and 84: RPS EnergyHeritage Oil - Competent

- Page 85 and 86: RPS EnergyHeritage Oil - Competent

- Page 87 and 88: RPS EnergyHeritage Oil - Competent

- Page 89 and 90: RPS EnergyHeritage Oil - Competent

- Page 91 and 92: RPS EnergyHeritage Oil - Competent

- Page 93 and 94: RPS EnergyHeritage Oil - Competent

- Page 95 and 96: RPS EnergyHeritage Oil - Competent

- Page 97 and 98: RPS EnergyHeritage Oil - Competent

- Page 99 and 100: RPS EnergyHeritage Oil - Competent

- Page 101 and 102: RPS EnergyHeritage Oil - Competent

- Page 103 and 104: RPS EnergyHeritage Oil - Competent

- Page 105 and 106: RPS EnergyHeritage Oil - Competent

- Page 107 and 108: RPS EnergyHeritage Oil - Competent

- Page 109 and 110: RPS EnergyHeritage Oil - Competent

- Page 111 and 112: RPS EnergyHeritage Oil - Competent

- Page 113 and 114: RPS EnergyHeritage Oil - Competent

- Page 115 and 116: RPS EnergyHeritage Oil - Competent

- Page 117 and 118: RPS EnergyHeritage Oil - Competent

- Page 119 and 120: RPS EnergyHeritage Oil - Competent

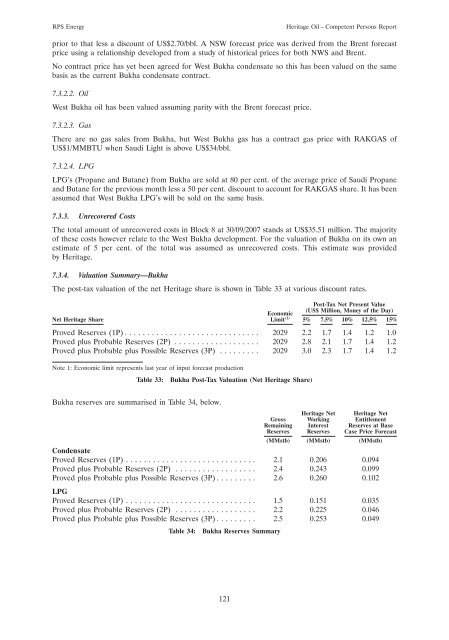

- Page 121: RPS EnergyHeritage Oil - Competent

- Page 125 and 126: RPS EnergyHeritage Oil - Competent

- Page 127 and 128: RPS EnergyHeritage Oil - Competent

- Page 129 and 130: RPS EnergyHeritage Oil - Competent

- Page 131 and 132: RPS EnergyHeritage Oil - Competent

- Page 133 and 134: RPS EnergyHeritage Oil - Competent

- Page 135 and 136: Summary Consolidated Balance Sheets

- Page 137 and 138: Summary Consolidated Balance Sheets

- Page 139 and 140: locks during the first three and a

- Page 141 and 142: On 2 October 2007, the Group execut

- Page 143 and 144: of amplitude anomalies, further sup

- Page 145 and 146: The increase in operating expenses

- Page 147 and 148: 5.11 Discontinued OperationsThe res

- Page 149 and 150: 6. RESULTS OF CONTINUING OPERATIONS

- Page 151 and 152: 6.7 Foreign Exchange LossesThere wa

- Page 153 and 154: 6.14 Capital ExpendituresThe follow

- Page 155 and 156: 7.3 Petroleum and Natural Gas Reven

- Page 157 and 158: 7.14 Capital ExpendituresAdditions

- Page 159 and 160: 10. LIQUIDITY AND CAPITAL RESOURCES

- Page 161 and 162: Year Ended 31 December 2005 Prepare

- Page 163 and 164: Intangible E&E assets related to ea

- Page 165 and 166: 11.2 The year ended 31 December 200

- Page 167 and 168: (c) Reconciliation of loss for the

- Page 169 and 170: Year Ended 31 December 2004 Prepare

- Page 171 and 172: PART VII—FINANCIAL INFORMATIONA.

- Page 173 and 174:

DeclarationFor the purposes of Pros

- Page 175 and 176:

HERITAGE OIL LIMITEDNOTES TO BALANC

- Page 177 and 178:

AUDITED AND UNAUDITED FINANCIAL INF

- Page 179 and 180:

HERITAGE OIL CORPORATIONCONSOLIDATE

- Page 181 and 182:

HERITAGE OIL CORPORATIONCONSOLIDATE

- Page 183 and 184:

HERITAGE OIL CORPORATIONNOTES TO CO

- Page 185 and 186:

Intangible E&E assets related to ea

- Page 187 and 188:

k) InvestmentsThe Group classifies

- Page 189 and 190:

usually when legal title passes to

- Page 191 and 192:

iii) IFRIC 12, ‘‘Service conces

- Page 193 and 194:

v) Liquidity riskLiquidity risk is

- Page 195 and 196:

ii) DerivativesDerivatives are reco

- Page 197 and 198:

5 Other finance costsNine-month per

- Page 199 and 200:

Congo to the other partners in the

- Page 201 and 202:

No assets have been pledged as secu

- Page 203 and 204:

31 December 30 September2005 2006 2

- Page 205 and 206:

16 Trade and other payables31 Decem

- Page 207 and 208:

A reconciliation of the asset retir

- Page 209 and 210:

21 Loss per shareThe following tabl

- Page 211 and 212:

25 Commitments and contingenciesHer

- Page 213 and 214:

In November 2007, the Group farmed-

- Page 215 and 216:

Reconciliation of loss for the year

- Page 217 and 218:

At the end of the last reporting pe

- Page 219 and 220:

Reconciliation of cash flow stateme

- Page 221 and 222:

At 31 December 2006, this has resul

- Page 223 and 224:

AUDITED FINANCIAL STATEMENTS RELATI

- Page 225 and 226:

AUDITORS’ REPORT TO THE SHAREHOLD

- Page 227 and 228:

HERITAGE OIL CORPORATIONCONSOLIDATE

- Page 229 and 230:

HERITAGE OIL CORPORATIONNOTES TO CO

- Page 231 and 232:

effective as hedges, both at incept

- Page 233 and 234:

A ceiling test was undertaken at De

- Page 235 and 236:

6. Share capital:(a) Authorized:Unl

- Page 237 and 238:

fair value of stock options are amo

- Page 239 and 240:

C. PRO FORMA FINANCIAL INFORMATION

- Page 241 and 242:

PRO FORMA NET ASSET STATEMENTThe fo

- Page 243 and 244:

Production assumptionsProduction du

- Page 245 and 246:

Macroeconomic assumptionsThe Direct

- Page 247 and 248:

Accordingly, the Illustrative Proje

- Page 249 and 250:

Arrangement AgreementPursuant to th

- Page 251 and 252:

PART X—ADDITIONAL INFORMATION1. R

- Page 253 and 254:

(ii) no share or loan capital of th

- Page 255 and 256:

(j)In Alberta, the principal jurisd

- Page 257 and 258:

nominal amount has been paid up of

- Page 259 and 260:

instrument of transfer (in the case

- Page 261 and 262:

up on all the shares conferring tha

- Page 263 and 264:

(B) may be a director or other offi

- Page 265 and 266:

and is in default for a period of 1

- Page 267 and 268:

(c)have sufficient moneys, assets o

- Page 269 and 270:

(e)against surrender of the Exchang

- Page 271 and 272:

e, to the extent that the same is r

- Page 273 and 274:

(g)(ii) by arranging for the credit

- Page 275 and 276:

(b) rights, options or warrants oth

- Page 277 and 278:

any provision of provincial, territ

- Page 279 and 280:

7.5 None of the major shareholders

- Page 281 and 282:

Position stillDirector/Senior Manag

- Page 283 and 284:

employment or terminates his or her

- Page 285 and 286:

All rights of a holder of Exchangea

- Page 287 and 288:

agreement of this nature. These cir

- Page 289 and 290:

to change. Where the Company pays a

- Page 291 and 292:

As part of an agreement reached in

- Page 293 and 294:

(x) Foreign Property Information Re

- Page 295 and 296:

19. DOCUMENTS AVAILABLE FOR INSPECT

- Page 297 and 298:

declared and unpaid dividends on ea

- Page 299 and 300:

‘‘DTR’’‘‘DutchCo’’

- Page 301 and 302:

‘‘ISIN’’‘‘ITA’’‘

- Page 303 and 304:

anniversary of the Effective Date a

- Page 305 and 306:

‘‘Support Agreement’’‘‘

- Page 307:

emaining quantities recovered will