- Page 1 and 2:

IFEAT INTERNATIONAL CONFERENCE 2012

- Page 3 and 4:

CONTENTSPREFACEvRavi Sanganeria, Ch

- Page 5:

IFEAT BUSINESS 283IFEAT Annual Repo

- Page 8 and 9:

On the last day of the conference,

- Page 11 and 12:

A VIEW OF MENTHOL DEVELOPMENT- FROM

- Page 13 and 14:

There is a highly educated workforc

- Page 15 and 16:

eturn, say, mint, in this case. In

- Page 17 and 18:

By 2001, mint production had declin

- Page 19 and 20:

Uttar Pradesh (UP)UP is India’s m

- Page 21:

Mint ProductionThe graph illustrate

- Page 25 and 26:

The table provides an example of th

- Page 27 and 28:

RECENT TRENDS AND FUTURE CHALLENGES

- Page 29 and 30:

Compared to the giants in synthetic

- Page 31:

THANK YOU &HAVE A NICE DAY!Mr "Gats

- Page 34 and 35:

An intriguing element of this myste

- Page 36 and 37:

This will produce significant, if u

- Page 38 and 39:

Rising UrbanizationIndia has 70% of

- Page 40 and 41:

Systemic Drivers for Sectoral Growt

- Page 42 and 43:

LuxuryIndia’s luxury market is st

- Page 44 and 45:

Growth Projection of F&F MarketOver

- Page 46 and 47:

The rewards for those who innovate,

- Page 48 and 49:

&!!"%#!"!"#$%&'()##)*+',-'.'%!!"$#!

- Page 50 and 51:

Within the total area of 2.94 milli

- Page 52 and 53:

The methodologies include training

- Page 54 and 55:

• Protective microorganisms• Na

- Page 56 and 57:

Figure 18 : Centritherm - Thin Film

- Page 59 and 60:

S. Palaniswamy RajaJasmine C. E. Pv

- Page 61 and 62:

Such cultivation and use of flowers

- Page 63 and 64:

The floral fragrance products in th

- Page 65 and 66:

(b) Sambac(b)SambacJasminum sambac

- Page 67 and 68:

(d) Mimosa(d)MimosaAcacia mearnsii

- Page 69:

FUTUREBesides the long tradition, t

- Page 72 and 73:

Geographically the state is divided

- Page 74 and 75:

This table below shows the volume o

- Page 76 and 77:

Main ConstituentsThe main constitue

- Page 78 and 79:

INDIAN CALAMUS OILThe botanical nam

- Page 80 and 81:

TAGETES OILThe botanical name is Ta

- Page 82 and 83:

JUNIPER BERRY OILThe botanical name

- Page 84 and 85:

Odour ProfileBalsamic, woody, herba

- Page 86 and 87:

This oil is one important component

- Page 88 and 89:

Various improvements in the cultiva

- Page 91 and 92:

CHINA’S FLAVOUR AND FRAGRANCE IND

- Page 93 and 94:

In my presentation today I intend t

- Page 95 and 96:

These figures show theproportionate

- Page 97 and 98:

Enterprises have to pay close atten

- Page 99 and 100:

OVERVIEW OF THE CHINESE GUM TURPENT

- Page 101 and 102:

The abundant pine forests in China

- Page 103 and 104:

Chinese GT Industry PerspectiveOleo

- Page 105 and 106:

faded out, which was equivalent to

- Page 107 and 108:

The GT derivatives industry has bee

- Page 109 and 110:

Acknowledgements• Mr. Lin Like, P

- Page 111 and 112:

ANETHOLE DEVELOPMENT TRENDSHuang Zo

- Page 113 and 114:

INDUSTRIAL PRODUCTION OF ANETHOLEAn

- Page 115 and 116:

hydrate (KOH), then anethole is gai

- Page 117 and 118:

output of anethole is calculated to

- Page 119 and 120:

price and supply of synthetic helio

- Page 121 and 122:

!!!!!!!!!!!THE ESSENTIAL OIL INDUST

- Page 123 and 124:

!!"#$%&'(')%*+,-(((The graphs below

- Page 125 and 126:

Pepper OilPepper, which is known as

- Page 127 and 128:

15Crop production: 2,700 mtOil expo

- Page 129 and 130:

vated as a mono crop in the Central

- Page 131 and 132:

distillation units there are 135 fi

- Page 133 and 134:

MAJOR CHALLENGES IN THE INDUSTRYTho

- Page 135 and 136:

THE FLAVOUR AND FRAGRANCE INDUSTRY

- Page 137 and 138:

THANK YOU!!!!!!!!!!!!!!!!!!!!!!!!!!

- Page 139 and 140:

INTRODUCTIONOVERVIEW OF THE AGARWOO

- Page 141 and 142:

AQUILARIA SPECIES PRODUCES AGARWOOD

- Page 143 and 144:

RESINOUS COMPOUNDSSome of these che

- Page 145 and 146:

OIL QUALITY GRADINGCurrently, there

- Page 147 and 148:

VALUE ADDITIONIN THE INDONESIAN FLA

- Page 149 and 150:

!"#$$%&'%()*&)+#$,%)-..*&'))!""#$%&

- Page 151 and 152:

MARKETING TRENDS OF AMBIENT SCENTIN

- Page 153 and 154:

Our fragrance partner is Drom with

- Page 155 and 156:

Hong KongHong Kong is the home to t

- Page 157 and 158:

Sustainability and Market Issues149

- Page 159 and 160:

INTRODUCTIONSUSTAINABLE SUPPLYA CON

- Page 161 and 162:

The internet age has dramatically c

- Page 163 and 164:

Similarly, our customers want to kn

- Page 165 and 166:

A critical part of Performance with

- Page 167 and 168:

Earlier I talked about how our bran

- Page 169 and 170:

INTRODUCTIONEFFORTS AND CHALLENGES

- Page 171 and 172:

The following table provides an ove

- Page 173 and 174:

price has recovered to normal andpr

- Page 175 and 176:

The activities of the patchouli pil

- Page 177 and 178:

CONCLUSIONSIn conclusion, consideri

- Page 179 and 180:

THE INGREDIENTS SUPPLY CHAIN:PAST A

- Page 181 and 182:

HOW HAVE BUYERS AND SUPPLIERS CONNE

- Page 183 and 184:

Let’s take a look at a few of the

- Page 185 and 186:

Illustrative example of a total ind

- Page 187 and 188:

ERP solution is provided as well as

- Page 189 and 190:

Traceability from the origin and ve

- Page 191 and 192:

Those who embrace this new dynamic

- Page 193 and 194:

New Sources of Natural Ingredient S

- Page 195 and 196:

AROMA CHEMICALS FROM THE TROPICS VI

- Page 197 and 198:

FROM BIOMATERIALS TO OLEOCHEMICALSB

- Page 199 and 200:

Bioconversion of coconut oil to est

- Page 201 and 202:

Shao Quan LIU is an Assistant Profe

- Page 203 and 204:

BIOTECHNOLOGY AND THE CHANGING ROLE

- Page 205 and 206:

Why is this so important to us? How

- Page 207 and 208:

and in the San Francisco Bay area (

- Page 209 and 210:

The tools that have been developed

- Page 211 and 212:

CAN BIO-SYNTHETIC BIOLOGY BE THE NE

- Page 213 and 214:

!"#$"%&'(#)(*+,%(-&.%,+(*%$&contain

- Page 215 and 216:

!"#$%&'(')*+",-.*/+01&')&23".4.56'7

- Page 217 and 218:

small additive, wherein you could h

- Page 219 and 220: And you can see that any of these c

- Page 221 and 222: Dr. P M Murali, is the Managing Dir

- Page 223 and 224: Regulatory Issues215

- Page 225 and 226: THE SOCIO-ECONOMIC IMPORTANCE OF TH

- Page 227 and 228: The issues affecting the fragrance

- Page 229 and 230: THE IFRA SOCIO-ECONOMIC ANALYSIS PR

- Page 231 and 232: So we have taken this grid, and est

- Page 233 and 234: The data have been broken down betw

- Page 235 and 236: Nevertheless, it’s the SCCS, so D

- Page 237 and 238: wolf: “Ah we can’t do anything,

- Page 239 and 240: The process would be to start from

- Page 241 and 242: I will not bore you with all of the

- Page 243 and 244: REACH: AN UPDATE OF EFEO’S PROGRA

- Page 245 and 246: Based on the 2005 survey 47 NCSs ar

- Page 247 and 248: Therefore, all manufacturers and su

- Page 249 and 250: As a result of EFEO’s phase-2 ini

- Page 251 and 252: EXPERIENCESThe data requirements fo

- Page 253 and 254: • exposure and risk assessment•

- Page 255 and 256: EFEO - THE FIRST DECADE AND BEYONDP

- Page 257 and 258: !"#$%&'()&*!+,&-($)#.&/&"*,!(0.& .1

- Page 259 and 260: !"#$%&'($")*$)&+&,+%-.!/)• '""$0"

- Page 261 and 262: Country and Other Studies253

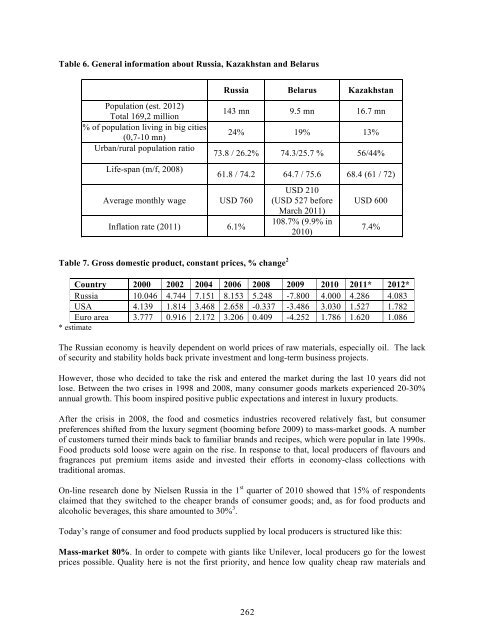

- Page 263 and 264: THE FLAVOUR AND FRAGRANCE INDUSTRY

- Page 265 and 266: Major business activity is still co

- Page 267 and 268: Important service provided by local

- Page 269: F&F BUYERS - DOMESTIC MARKETIn the

- Page 273 and 274: Household chemicalsSince the late 1

- Page 275 and 276: Consumers’ habits are also changi

- Page 277 and 278: Alcoholic beveragesThe most popular

- Page 279 and 280: BIBLIOGRAPHY1. http://www.gks.ru/fr

- Page 281 and 282: IMPROVED IDENTIFICATION METHODS FOR

- Page 283 and 284: Australian aboriginals have used th

- Page 285 and 286: Another interesting point is thenum

- Page 287 and 288: perform a chiral test on these comp

- Page 289 and 290: If you are buying oil in 185 kgs st

- Page 291 and 292: IFEAT Business283

- Page 293 and 294: IFEAT ANNUAL REPORT 2011Ramon Borda

- Page 295 and 296: INTRODUCTIONICATS / PLYMOUTH UNIVER

- Page 297 and 298: A key ICATS activity, supported by

- Page 299 and 300: REPORT ON THE 2012BRITISH SOCIETY O

- Page 301 and 302: As the course progresses, flavour c

- Page 303 and 304: BRAZIL & PARAGUAY IFEAT STUDY TOUR

- Page 305 and 306: After the return of the boat, we dr

- Page 307 and 308: Saturday was one the highlights of

- Page 309 and 310: IFEAT 2013 SAN FRANCISCO CONFERENCE

- Page 311 and 312: The Fairmont has excellent dining f

- Page 313 and 314: VISASWhat is IFEAT proposing to do?

- Page 315 and 316: THE IFEAT 2013 STUDY TOUR TO SOUTH

- Page 317 and 318: Sunday 9th JuneParticipants arrive

- Page 319 and 320: Friday 14th June - Day 5Friday 14th

- Page 321 and 322:

Monday 17th June - Day 8In the morn

- Page 323 and 324:

INTRODUCTIONICATS INTERMEDIATE PERF

- Page 325 and 326:

WHY FRAGRANCE PRODUCTS?There is onl

- Page 327 and 328:

In this paper for the conference pr

- Page 329 and 330:

FRAGRANCE CREATIONThis was a short