- Page 1 and 2:

CITY COUNCILAGENDACouncil Chambers,

- Page 3 and 4:

Wellington-Dufferin-Guelph Board of

- Page 5 and 6:

October 16, 2012 Page No. 286Commit

- Page 7 and 8:

October 22, 2012 Page No. 288Counci

- Page 9:

October 22, 2012 Page No. 290Counci

- Page 12 and 13:

October 22, 2012 Page No. 293Counci

- Page 14 and 15:

October 22, 2012 Page No. 295The me

- Page 16 and 17:

October 22, 2012 Page No. 297THAT t

- Page 18 and 19:

October 22, 2012 Page No. 299AND TH

- Page 20 and 21:

October 22, 2012 Page No. 301AND TH

- Page 22 and 23:

October 22, 2012 Page No. 303Consen

- Page 24 and 25:

October 22, 2012 Page No. 305Counci

- Page 26 and 27:

October 22, 2012 Page No. 307collec

- Page 28 and 29:

October 22, 2012 Page No. 309AND TH

- Page 30 and 31:

October 22, 2012 Page No. 311Goodwi

- Page 32 and 33:

October 24, 2012 Page No 313Council

- Page 34 and 35:

October 24, 2012 Page No 315average

- Page 36 and 37:

October 24, 2012 Page No 3172. the

- Page 38 and 39:

October 24, 2012 Page No 319VOTING

- Page 40 and 41:

November 5, 2012 Page No. 321(Speci

- Page 42 and 43:

November 5, 2012 Page No. 323AND TH

- Page 44 and 45:

November 5, 2012 Page No. 325Paris-

- Page 46 and 47:

November 5, 2012 Page No. 327The me

- Page 48 and 49:

Schedule 1 - Page 2November 5, 2012

- Page 50 and 51:

Schedule 1 - Page 4November 5, 2012

- Page 52 and 53:

Schedule 1 - Page 6November 5, 2012

- Page 54 and 55:

Schedule 2 - Page 1November 5, 2012

- Page 56 and 57:

Schedule 2 - Page 3November 5, 2012

- Page 58 and 59:

Schedule 2 - Page 5November 5, 2012

- Page 60 and 61:

Schedule 3 - Page 2November 5, 2012

- Page 62 and 63:

Schedule 3 - Page 4November 5, 2012

- Page 64 and 65:

Schedule 3 - Page 6November 5, 2012

- Page 66 and 67:

November 6, 2012 Page No. 328Room C

- Page 68 and 69:

CONSENT REPORT OF THECOMMUNITY & SO

- Page 70 and 71:

COMMITTEEREPORTTOCommunity and Soci

- Page 72 and 73:

Option B: The Guelph Royals apply f

- Page 74 and 75:

COMMITTEEREPORTTOCommunity and Soci

- Page 76 and 77:

http://www.seniors.gov.on.ca/en/afc

- Page 78 and 79:

Vision , Guiding Values and Princip

- Page 80 and 81:

services, housing services, and edu

- Page 82 and 83:

Letter of Transmittal190 Attwell Dr

- Page 84 and 85:

1. ACKNOWLEDGEMENTSIt has been a pl

- Page 86 and 87:

Attachment 1Proposed guiding statem

- Page 88 and 89:

Attachment 111. Identify locations

- Page 90 and 91:

Attachment 137. Develop a Community

- Page 92 and 93:

Attachment 1HEALTH AND COMMUNITY SU

- Page 94 and 95:

Attachment 1Change Foundation, 2011

- Page 96 and 97:

Attachment 13. Housing• (e.g. cos

- Page 98 and 99:

Attachment 1Although the local popu

- Page 100 and 101:

Attachment 1Similar analysis for ol

- Page 102 and 103:

Attachment 1The full text of our co

- Page 104 and 105:

Attachment 18. SUMMARY OF CONSULTAT

- Page 106 and 107:

Attachment 1Urban design has contri

- Page 108 and 109:

Attachment 1• Community Care Acce

- Page 110 and 111:

Attachment 1Areas for ImprovementTh

- Page 112 and 113:

Attachment 1Areas for ImprovementTh

- Page 114 and 115:

Attachment 1People with mental heal

- Page 116 and 117:

DiversityOlder adults are not a hom

- Page 118 and 119:

Attachment 1Transit and MobilityMob

- Page 120 and 121:

Attachment 1Community Support Servi

- Page 122 and 123:

Attachment 1The City has done an ex

- Page 124 and 125:

Attachment 1POPULATION GROWTH PROJE

- Page 126 and 127:

11. RECOMMENDATIONSThis report prop

- Page 128 and 129:

Attachment 1Rationale:The importanc

- Page 130 and 131:

Attachment 1• Establishment of an

- Page 132 and 133:

Attachment 1A standardized approach

- Page 134 and 135:

Attachment 1Timeline: OngoingLead R

- Page 136 and 137:

Attachment 1Recommendation Timeline

- Page 138 and 139:

Attachment 1Recommendation Timeline

- Page 140 and 141:

Attachment 1Recommendation Timeline

- Page 142 and 143:

Attachment 1Recommendation Timeline

- Page 144 and 145:

Attachment 1Recommendation Timeline

- Page 146 and 147:

City of Guelph Older Adult Strategy

- Page 148 and 149:

Attachment 1Activities/Actions by R

- Page 150 and 151:

Attachment 1Activities/Actions by R

- Page 152 and 153:

13. EVALUATIONAs noted earlier, an

- Page 154 and 155:

Older Adult Strategy - Preliminary

- Page 156 and 157:

Attachment 1Recommendation Proposed

- Page 158 and 159:

Attachment 1Recommendation Proposed

- Page 160 and 161:

Attachment 1Recommendation Proposed

- Page 162 and 163:

Appendix A - Steering Committee Mem

- Page 164 and 165:

Attachment 137. McMaster University

- Page 166 and 167:

Attachment 1Appendix D - Sample Que

- Page 168 and 169:

Attachment 1In Public housing renta

- Page 170 and 171:

Attachment 1RESPECT AND SOCIAL INCL

- Page 172 and 173:

Attachment 1Appendix E - Summary of

- Page 174 and 175:

Attachment 1County of WellingtonAff

- Page 176 and 177:

Attachment 1The Seniors Advisory Co

- Page 178 and 179:

Attachment 1APPENDIXSENIORS ADVISOR

- Page 180 and 181:

COMPARATOR MUNICIPALITY: CHATHAM-KE

- Page 182 and 183:

4. Within sixty (60) days of a vaca

- Page 184 and 185:

Participants then conducted an audi

- Page 186 and 187:

COMPARATOR MUNICIPALITY: BRANT/BRAN

- Page 188 and 189:

6. FUNDING THE INITIATIVEDevelopmen

- Page 190:

This report authored byThe Osborne

- Page 208 and 209:

The issue of the cost of Police Rec

- Page 210 and 211:

City Building3.1 Ensure a well desi

- Page 212 and 213:

THE CHALLENGE• Community benefit

- Page 214 and 215:

The Program Model for GuelphThe pro

- Page 216 and 217:

Why a Community Benefit Agreement?T

- Page 218 and 219:

COMMITTEEREPORTTOCommunity and Soci

- Page 220 and 221:

The Interim Agreement is included a

- Page 222 and 223:

Attachment 1This agreement made thi

- Page 224 and 225:

City of Guelph, University of Guelp

- Page 226 and 227:

City of Guelph, University of Guelp

- Page 228 and 229:

City of Guelph, University of Guelp

- Page 230 and 231:

CONSENT REPORT OF THECORPORATE ADMI

- Page 232 and 233:

municipality’s competitive advant

- Page 234 and 235:

Local Government, City Building) in

- Page 236 and 237:

Similarly, implementation of the Se

- Page 238 and 239:

Through this lens, the CSP Work Pla

- Page 240 and 241:

Prepared By:Brenda BoisvertCorporat

- Page 242 and 243:

Appendix A - Recommended CSP Work P

- Page 244 and 245:

Appendix A - Recommended CSP Work P

- Page 246 and 247:

51 City Wifi Business Case (Joint W

- Page 248 and 249:

Report Recommendations• THAT Coun

- Page 250 and 251:

Initiative Evaluation Process1. ‘

- Page 252 and 253:

2. Focusing on Key Performance Indi

- Page 254 and 255:

Adjusting Pace• Citizen First Ser

- Page 256 and 257:

Next StepsElementInclusion of CSP r

- Page 258 and 259:

Page No. 2November 26, 2012Governan

- Page 260 and 261:

Government and its current context.

- Page 262 and 263:

PrinciplesThe vision of Open Govern

- Page 264 and 265:

• Senior Communications and Issue

- Page 266 and 267:

Attachment 1: A Survey of Open Gove

- Page 268 and 269:

Attachment 1: A Survey of Open Gove

- Page 270 and 271:

Attachment 1: A Survey of Open Gove

- Page 272 and 273:

Attachment 1: A Survey of Open Gove

- Page 274 and 275:

Attachment 1: A Survey of Open Gove

- Page 276 and 277:

Attachment 1: A Survey of Open Gove

- Page 278 and 279:

Attachment 1: A Survey of Open Gove

- Page 280 and 281:

Attachment 1: A Survey of Open Gove

- Page 282 and 283:

Attachment 1: A Survey of Open Gove

- Page 284 and 285:

Attachment 1: A Survey of Open Gove

- Page 286 and 287:

#Overview• History• Drivers•

- Page 288 and 289:

#Drivers#External• “FAST” org

- Page 290 and 291:

#Defining Open GovTransparencyTo cr

- Page 292 and 293:

#Open EngagementTo build on the tra

- Page 294 and 295:

#Open DataTo encourage the use of p

- Page 296 and 297:

#Apps for Democracy• 2008 app cha

- Page 298 and 299: #Access to InformationTo subscribe

- Page 300 and 301: #Open GovernanceTo develop a manage

- Page 302: #Track.dc.gov18

- Page 305 and 306: #Next Steps• Phase 1 (2012)• Co

- Page 307 and 308: I submit these comments on behalf o

- Page 309 and 310: COUNCILREPORTTOGovernance Committee

- Page 311 and 312: strategic issues management along w

- Page 313 and 314: 2013 Council and Committee Meeting

- Page 315 and 316: 2013 Council and Committee Meeting

- Page 317 and 318: 2013 Council and Committee Meeting

- Page 319 and 320: COMMITTEEREPORTTOGovernance Committ

- Page 321 and 322: Standing Committees 2009 2010 2011

- Page 323: wording. Council is then required t

- Page 334 and 335: 2006-2010 Councillor Time Commitmen

- Page 336 and 337: Good governance creates a strong fu

- Page 338 and 339: __________________________Prepared

- Page 340 and 341: Appendix B - Preliminary Review of

- Page 342 and 343: COMMITTEEREPORTTOGovernance Committ

- Page 344 and 345: In an effort to demonstrate efficie

- Page 346 and 347: Deliverables would include:• Iden

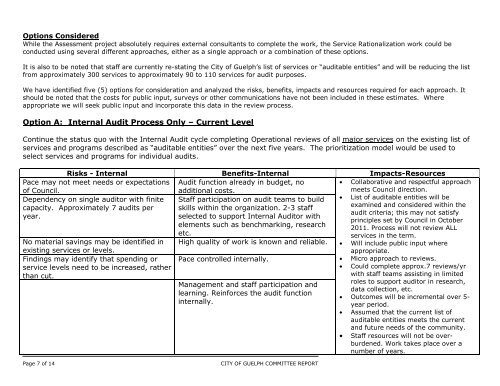

- Page 350 and 351: Option C: Organizational Assessment

- Page 352 and 353: Option E: Organization Assessment (

- Page 354 and 355: ConclusionOur strategic plan sets o

- Page 356 and 357: CONSENT REPORT OF THENOMINATING COM

- Page 358 and 359: COMMITTEEREPORTTOOperations, Transi

- Page 360 and 361: 1. ParkingIt will be necessary to e

- Page 362 and 363: DEPARTMENTAL CONSULTATIONFinance &

- Page 364 and 365: COMMITTEEREPORTTOPlanning & Buildin

- Page 366 and 367: CORPORATE STRATEGIC PLAN1.2 Develop

- Page 368 and 369: f. The following is inserted as the

- Page 370 and 371: REPORTBarrel Works Guelph Limited h

- Page 372 and 373: SCHEDULE A- LOCATION MAPPage 4 of 6

- Page 374 and 375: SCHEDULE B- SIGNAGE FOR VARIANCE123

- Page 376 and 377: Part Lot 6, Registered Plan 128;Par