Correction des exercices du livre La Gestion des Risques Financiers

Correction des exercices du livre La Gestion des Risques Financiers

Correction des exercices du livre La Gestion des Risques Financiers

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

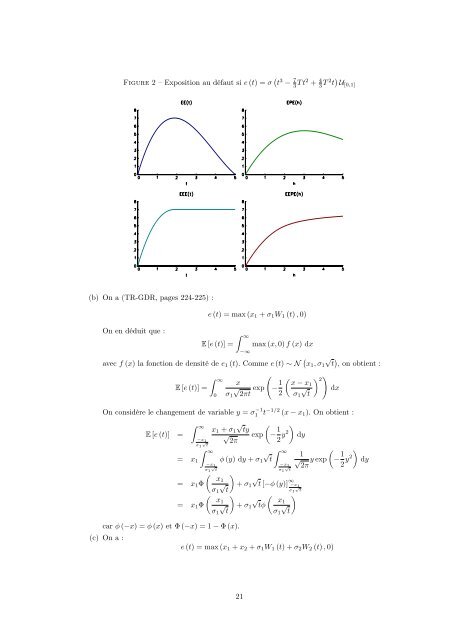

Figure 2 – Exposition au défaut si e (t) = σ ( t 3 − 7 3 T t2 + 4 3 T 2 t ) U [0,1](b) On a (TR-GDR, pages 224-225) :On en dé<strong>du</strong>it que :e (t) = max (x 1 + σ 1 W 1 (t) , 0)E [e (t)] =∫ ∞−∞max (x, 0) f (x) dxavec f (x) la fonction de densité de e 1 (t). Comme e (t) ∼ N ( x 1 , σ 1√t), on obtient :E [e (t)] =∫ ∞−x 1σ 1√t∫ ∞0(x√ exp − 1 ( ) ) 2 x − x1√ dxσ 1 2πt 2 σ 1 tOn considère le changement de variable y = σ1 −1 t−1/2 (x − x 1 ). On obtient :E [e (t)] =exp(− 1 )2 y2 dyx 1 + σ 1√ty√2π∫ ∞ √∫ ∞= x 1 ϕ (y) dy + σ 1 t−x√ 1−x 1σ 1 t( )x1 √∞= x 1 Φ √ + σ 1 t [−ϕ (y)] −x1σ 1 t√σ 1 t= x 1 Φcar ϕ (−x) = ϕ (x) et Φ (−x) = 1 − Φ (x).(c) On a :σ 1√t1(x1σ 1√t)+ σ 1√tϕ(x1σ 1√t)√ y exp(− 1 )2π 2 y2e (t) = max (x 1 + x 2 + σ 1 W 1 (t) + σ 2 W 2 (t) , 0)dy21