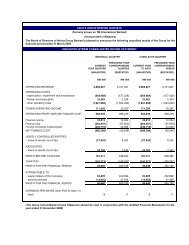

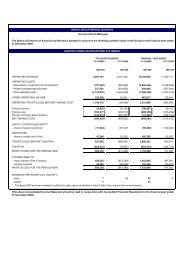

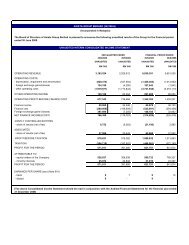

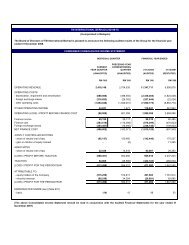

Download - Axiata Group Berhad - Investor Relations

Download - Axiata Group Berhad - Investor Relations

Download - Axiata Group Berhad - Investor Relations

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Key building blocks for App StoresTo understand the future of app stores one must not only look at their historical evolution, but also at their geneticmake-up. The diagram below presents the five key elements of an App Store and their potential evolution over thenext few years.Key Building BlocksBuilding block Developer market Billing & settlement Distribution surfaceDescriptionEvolution2000-2007open APIs,closed route tomarket2008-2009the iTunes Storecloning era2010-2012the app storeseverywhere eraRolesMNO uniquevalue addOEM uniquevalue addprocess for submission,certification, targeting andpricing of applicationscomplex, undocumented &fragmented approach forcertification and pricingsingle websites forsubmission, certification,targeting and pricing ofapplications10s of marketplaces,emergence of marketplaceaggregatorsnoneplatform certification,developer tools, developercommunitiesSource: VisionMobile researchmerchanism for billing,settlement and reportingof application salesdevelopers had to set upown billing or use premiumSMS with only 10%-50%going to developercredit-card billing, fasttime-to-settlement, 70%rev share as the normubiquitous operator billingapproaching 70% revshare, and multitude ofrevenue modelsestablished billingrelationship and credit linenonesize of addressable marketacross mobile phone OEMs,operators and regionsdistribution done onregion-by-region ANDhandset-by-handset basisglobal distribution on aper-platform basis (OSX,560, Blackberry, etc)global distribution onper-platform ORper-operator basisDelivery & in-lifemanagementapp download, silent install,in-place access, applicensing and in-life appmanagementdownload separate fromaccess, lack of updates, norights managementtransparent app download,install, access and in-lifeapp updatingapp delivery extends toB2B apps and meddlewarethat can be backgrounddownloaded& installedRetailing &Merchandisingapp discovery, apppromotion, premiumplacement, search andrecommendationsapp promotions anddiscovery via complexshortcodes and scatteredwebsite adson-device app discovery,1-click purchase,auto-matedrecommendationssegment-specific retailing ofapps, socialrecommendations anddeveloper back-channelnone none can aggregate apps acrossdevices/stpres andpromote ‘preferred’ appscross-operator andcross-regional distributionon-device integration fortransparent app install,access & lifecyclemanagementnoneThe Challenges & Opportunities for MNOsAs major vendors open their own app stores to sellmobile content directly to end users, MNOs are atincreasing risk of being disintermediated from the contentvalue chain. MNOs’ recent initiatives have largely beendesigned to address this threat. For example, Vodafoneunveiled its global initiative in May 2009, when it promisedto offer its application developers a single point ofaccess to its 289 million users worldwide and morerecently, 24 operators from around the world have cometogether to launch a joint wholesale applicationcommunity (WAC) that aims to pool joint developercommunities and platforms to target a base of about 3billion subscribersMNOs are well-placed to enhance some aspects of theuser experience by utilising their core network assets.For example, their billing assets offer an intuitive paymentexperience. MNOs provide premium-rate SMS servicesand a mobile Internet billing platform, which offer endusers an extremely easy-to-use payment process. Severalmajor vendors’ app stores offer credit card and PayPalpayment methods, but these tend to be cumbersome incomparison to operators’ on-phone billing mechanisms.MNOs will also need to overcome some significantobstacles. Device fragmentation will be a considerablebarrier to providing a wide selection of applications toend users and to maintaining quality. Devices differ interms of their OS (for example, Android, Linux, MicrosoftWindows Mobile, Palm and Symbian), application platform(for example, BREW, C++ and Java) and capabilities (forexample, screen size and resolution, memory capacityand battery power).This requires content and application providers to developmultiple versions of each of their products to accommodatethe diversification in mobile phones, which result in highdevelopment costs and therefore inhibits the proliferationand quality of mobile applications. This issue will be morechallenging for MNOs than device vendors, becauseMNOs will need to operate app store platforms that aresuitable for multiple device types, whereas devicevendors can focus on one or very few platforms.Despite these challenges, MNOs should work toincorporate app stores into their service portfolios inorder to capitalise on the growing consumer demand formobile applications, retain control of the end-userrelationship and therefore maintain their relevance to thecontent value chain.Annual Report 2009 • 143