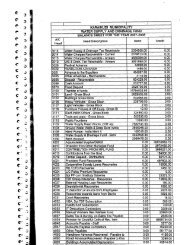

Tamil Nadu Urban Infrastructure Financial Services ... - Municipal

Tamil Nadu Urban Infrastructure Financial Services ... - Municipal

Tamil Nadu Urban Infrastructure Financial Services ... - Municipal

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

8. Initiate formal and independent Information Systems and Security Audits, given the<br />

implemented and ongoing e-governance initiatives of ULBs in <strong>Tamil</strong> <strong>Nadu</strong> –<br />

ULBs should be required to establish the practices of an independent system audit to be<br />

conducted annually. This would enable ULBs to establish greater accountability and build in<br />

robust processes for disaster recovery and security of the IT architecture of the ULB<br />

9. Facilitate creation of a formal institutional mechanism to manage functional overlaps<br />

among nodal agencies/state level agencies and the ULB – As described earlier in section 5.4 –<br />

role of other agencies, ULBs shares responsibility for a number of service delivery areas with<br />

other agencies/departments of the state including Department of Town Planning, Department of<br />

Highway, <strong>Tamil</strong> <strong>Nadu</strong> Electricity Board, <strong>Tamil</strong> <strong>Nadu</strong> Water and Drainage Board, Road Transport<br />

Corporations etc.<br />

In order to overcome the limitations of these overlaps and to enable operation of these<br />

various organs of the state in a coordinated manner, each ULB should be mandated to<br />

facilitate creation of a formal steering committee at the city level comprising of 8-10<br />

officials from all government departments/agencies. This committee could meet regularly<br />

(once every 2-3 months) to discuss and share information on respective projects/areas and<br />

could pave the way for better communication and effective service delivery.<br />

9.3 Suggestions for improving financial performance and collection efficiency<br />

Overall income of Krish- M grew at a -0.5 % CAGR, driven largely by significant growth in Water<br />

and Other service charges income. Own income of the municipality grew at a moderate 5 %, while<br />

expenditure actually declined during the period at a CAGR of 8% due to a steep decline in<br />

Administrative expenses and finance expenditure. However, this presents only part of the picture.<br />

Current collection efficiencies in property tax and water user charges are abysmally low at an average<br />

61% and 66% respectively.<br />

Krish- M‟s ability to improve on its financial performance hinges primarily on its ability to sustain<br />

and improve on the revenue growth noticeable in recent years. While there is potential for expenditure<br />

control in certain areas (as in the case of energy costs), the focus of cost management should be to<br />

shift expenditure from administration to better asset management and O&M. The following<br />

paragraphs outline select interventions for improvement of financial and operating performance.<br />

9.3.1 Revenue enhancement<br />

Property tax<br />

Specific recommendations for improving property tax revenue and collections are detailed below.<br />

Recommendations in bold are actions that can be implemented immediately by the municipality<br />

without any significant investment and can enable the municipality to show immediate results<br />

CCP cum BP - Krishnagiri <strong>Municipal</strong>ity 78