Nkomazi Local Municipality 20 - Co-operative Governance and ...

Nkomazi Local Municipality 20 - Co-operative Governance and ...

Nkomazi Local Municipality 20 - Co-operative Governance and ...

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

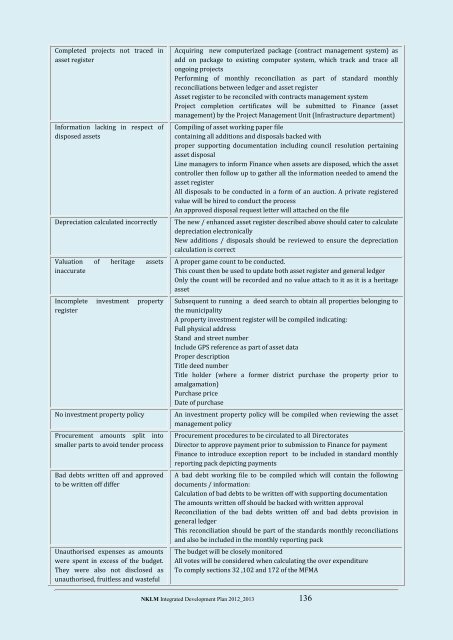

<strong>Co</strong>mpleted projects not traced inasset registerInformation lacking in respect ofdisposed assetsDepreciation calculated incorrectlyValuation of heritage assetsinaccurateIncomplete investment propertyregisterNo investment property policyProcurement amounts split intosmaller parts to avoid tender processBad debts written off <strong>and</strong> approvedto be written off differUnauthorised expenses as amountswere spent in excess of the budget.They were also not disclosed asunauthorised, fruitless <strong>and</strong> wastefulAcquiring new computerized package (contract management system) asadd on package to existing computer system, which track <strong>and</strong> trace allongoing projectsPerforming of monthly reconciliation as part of st<strong>and</strong>ard monthlyreconciliations between ledger <strong>and</strong> asset registerAsset register to be reconciled with contracts management systemProject completion certificates will be submitted to Finance (assetmanagement) by the Project Management Unit (Infrastructure department)<strong>Co</strong>mpiling of asset working paper filecontaining all additions <strong>and</strong> disposals backed withproper supporting documentation including council resolution pertainingasset disposalLine managers to inform Finance when assets are disposed, which the assetcontroller then follow up to gather all the information needed to amend theasset registerAll disposals to be conducted in a form of an auction. A private registeredvalue will be hired to conduct the processAn approved disposal request letter will attached on the fileThe new / enhanced asset register described above should cater to calculatedepreciation electronicallyNew additions / disposals should be reviewed to ensure the depreciationcalculation is correctA proper game count to be conducted.This count then be used to update both asset register <strong>and</strong> general ledgerOnly the count will be recorded <strong>and</strong> no value attach to it as it is a heritageassetSubsequent to running a deed search to obtain all properties belonging tothe municipalityA property investment register will be compiled indicating:Full physical addressSt<strong>and</strong> <strong>and</strong> street numberInclude GPS reference as part of asset dataProper descriptionTitle deed numberTitle holder (where a former district purchase the property prior toamalgamation)Purchase priceDate of purchaseAn investment property policy will be compiled when reviewing the assetmanagement policyProcurement procedures to be circulated to all DirectoratesDirector to approve payment prior to submission to Finance for paymentFinance to introduce exception report to be included in st<strong>and</strong>ard monthlyreporting pack depicting paymentsA bad debt working file to be compiled which will contain the followingdocuments / information:Calculation of bad debts to be written off with supporting documentationThe amounts written off should be backed with written approvalReconciliation of the bad debts written off <strong>and</strong> bad debts provision ingeneral ledgerThis reconciliation should be part of the st<strong>and</strong>ards monthly reconciliations<strong>and</strong> also be included in the monthly reporting packThe budget will be closely monitoredAll votes will be considered when calculating the over expenditureTo comply sections 32 ,102 <strong>and</strong> 172 of the MFMANKLM Integrated Development Plan <strong>20</strong>12_<strong>20</strong>13 136