Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

KPN Telecom<br />

Netherlands/Telecommunications Analyser<br />

KPN Telecom (Accumulate)<br />

Accumulate<br />

from Reduce<br />

Share price: EUR<br />

closing price as of 07/05/2012<br />

Target price: EUR<br />

Target Price unchanged<br />

Reuters/Bloomberg<br />

6.48<br />

7.50<br />

KPN.AS/KPN NA<br />

Market capitalisation (EURm) 9,319<br />

Current N° of shares (m) 1,438<br />

Free float 95%<br />

Daily avg. no. trad. sh. 12 mth 7,691,553<br />

Daily avg. trad. vol. 12 mth (m) 70<br />

Price high 12 mth (EUR) 10.72<br />

Price low 12 mth (EUR) 6.37<br />

Abs. perf. 1 mth -17.76%<br />

Abs. perf. 3 mth -21.10%<br />

Abs. perf. 12 mth -39.33%<br />

Key financials (EUR) 12/11 12/12e 12/13e<br />

Sales (m) 13,163 12,681 12,549<br />

EBITDA (m) 5,138 4,739 4,850<br />

EBITDA margin 39.0% 37.4% 38.7%<br />

EBIT (m) 2,550 2,348 2,404<br />

EBIT margin 19.4% 18.5% 19.2%<br />

Net Profit (adj.)(m) 1,549 1,259 1,332<br />

ROCE 13.3% 12.0% 12.6%<br />

Net debt/(cash) (m) 12,109 12,674 12,350<br />

Net Debt/Equity 4.1 4.3 3.9<br />

Debt/EBITDA 2.4 2.7 2.5<br />

Int. cover(EBITDA/Fin. int) 6.8 6.4 6.7<br />

EV/Sales 2.0 1.7 1.7<br />

EV/EBITDA 5.0 4.6 4.5<br />

EV/EBITDA (adj.) 5.0 4.6 4.5<br />

EV/EBIT 10.1 9.4 9.0<br />

P/E (adj.) 8.8 7.4 7.0<br />

P/BV 4.7 3.2 3.0<br />

OpFCF yield 19.4% 22.5% 22.9%<br />

Dividend yield 13.1% 13.9% 9.3%<br />

EPS (adj.) 1.05 0.88 0.92<br />

BVPS 1.98 2.05 2.17<br />

DPS 0.85 0.90 0.60<br />

10.5 vvdsvdvsdy<br />

10.0<br />

9.5<br />

9.0<br />

8.5<br />

8.0<br />

7.5<br />

7.0<br />

6.5<br />

6.0<br />

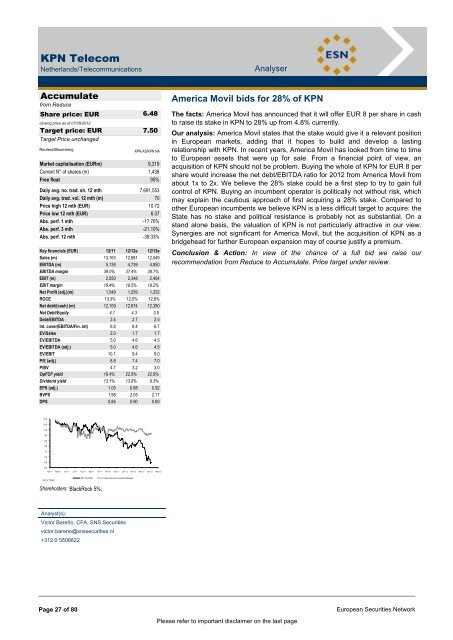

Apr 11 May 11 Jun 11 Jul 11 Aug 11 Sep 11 Oct 11 Nov 11 Dec 11 Jan 12 Feb 12 Mar 12 Apr 12 May 12<br />

Source: Factset<br />

Shareholders: BlackRock 5%;<br />

Analyst(s):<br />

KPN TELECOM Stoxx Telecommunications (Rebased)<br />

Victor Bareño, CFA, SNS Securities<br />

victor.bareno@snssecurities.nl<br />

+312 0 5508822<br />

America Movil bids for 28% of KPN<br />

The facts: America Movil has announced that it will offer EUR 8 per share in cash<br />

to raise its stake in KPN to 28% up from 4.8% currently.<br />

Our analysis: America Movil states that the stake would give it a relevant position<br />

in European markets, adding that it hopes to build and develop a lasting<br />

relationship with KPN. In recent years, America Movil has looked from time to time<br />

to European assets that were up for sale. From a financial point of view, an<br />

acquisition of KPN should not be problem. Buying the whole of KPN for EUR 8 per<br />

share would increase the net debt/EBITDA ratio for 2012 from America Movil from<br />

about 1x to 2x. We believe the 28% stake could be a first step to try to gain full<br />

control of KPN. Buying an incumbent operator is politically not without risk, which<br />

may explain the cautious approach of first acquiring a 28% stake. Compared to<br />

other European incumbents we believe KPN is a less difficult target to acquire: the<br />

State has no stake and political resistance is probably not as substantial. On a<br />

stand alone basis, the valuation of KPN is not particularly attractive in our view.<br />

Synergies are not significant for America Movil, but the acquisition of KPN as a<br />

bridgehead for further European expansion may of course justify a premium.<br />

Conclusion & Action: In view of the chance of a full bid we raise our<br />

recommendation from Reduce to Accumulate. Price target under review.<br />

Page 27 of 80 European Securities Network<br />

Please refer to important disclaimer on the last page