Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Agennix<br />

Germany/Biotechnology Analyser<br />

Agennix (Buy)<br />

Buy<br />

Recommendation unchanged<br />

Share price: EUR<br />

closing price as of 07/05/2012<br />

Target price: EUR<br />

Target Price unchanged<br />

Reuters/Bloomberg<br />

1.71<br />

2.40<br />

<strong>AG</strong>X.DE/<strong>AG</strong>X GR<br />

Market capitalisation (EURm) 88<br />

Current N° of shares (m) 51<br />

Free float 27%<br />

Daily avg. no. trad. sh. 12 mth 8,773<br />

Daily avg. trad. vol. 12 mth (m) 0<br />

Price high 12 mth (EUR) 3.51<br />

Price low 12 mth (EUR) 1.50<br />

Abs. perf. 1 mth -0.64%<br />

Abs. perf. 3 mth 2.34%<br />

Abs. perf. 12 mth -52.40%<br />

Key financials (EUR) 12/11 12/12e 12/13e<br />

Sales (m) 0 0 45<br />

EBITDA (m) (45) (45) 9<br />

EBITDA margin nm nm 20.3%<br />

EBIT (m) (45) (46) 8<br />

EBIT margin nm nm 18.5%<br />

Net Profit (adj.)(m) (42) (47) 8<br />

ROCE -31.0% -31.7% 5.8%<br />

Net debt/(cash) (m) (44) (1) (45)<br />

Net Debt/Equity -0.3 0.0 -0.4<br />

Debt/EBITDA 1.0 0.0 -4.9<br />

Int. cover(EBITDA/Fin. int) (112.1) (119.1) 15.5<br />

EV/Sales nm nm 0.9<br />

EV/EBITDA nm nm 4.6<br />

EV/EBITDA (adj.) nm nm 4.6<br />

EV/EBIT nm nm 5.0<br />

P/E (adj.) nm nm 11.2<br />

P/BV 0.8 0.9 0.9<br />

OpFCF yield -38.5% -48.7% 51.2%<br />

Dividend yield 0.0% 0.0% 0.0%<br />

EPS (adj.) (0.99) (0.91) 0.15<br />

BVPS 3.32 1.83 1.98<br />

DPS 0.00 0.00 0.00<br />

4.0 vvdsvdvsdy<br />

3.5<br />

3.0<br />

2.5<br />

2.0<br />

1.5<br />

Apr 11 May 11 Jun 11 Jul 11 Aug 11 Sep 11 Oct 11 Nov 11 Dec 11 Jan 12 Feb 12 Mar 12 Apr 12 May 12<br />

Source: Factset<br />

<strong>AG</strong>ENNIX CDAX (Rebased)<br />

Shareholders: Dievini Hopp 65%; Cain Family 8%;<br />

Analyst(s):<br />

Edouard Aubery, Equinet Bank<br />

edouard.aubery@equinet-ag.de<br />

+49 69 5899 7439<br />

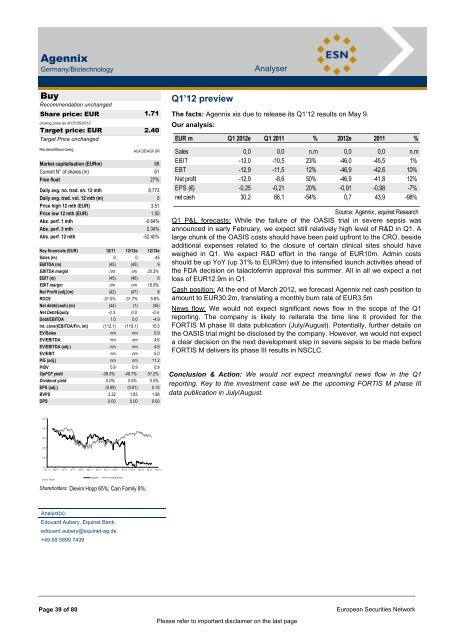

Q1’12 preview<br />

The facts: Agennix xis due to release its Q1‟12 results on May 9.<br />

Our analysis:<br />

EUR m Q1 2012e Q1 2011 % 2012e 2011 %<br />

Sales 0,0 0,0 n.m 0,0 0,0 n.m<br />

EBIT -13,0 -10,5 23% -46,0 -45,5 1%<br />

EBT -12,9 -11,5 12% -46,9 -42,6 10%<br />

Net profit -12,9 -8,6 50% -46,9 -41,8 12%<br />

EPS (€) -0,25 -0,21 20% -0,91 -0,98 -7%<br />

net cash 30,2 66,1 -54% 0,7 43,9 -98%<br />

Source: Agennix, equinet Research<br />

Q1 P&L forecasts: While the failure of the OASIS trial in severe sepsis was<br />

announced in early February, we expect still relatively high level of R&D in Q1. A<br />

large chunk of the OASIS costs should have been paid upfront to the CRO, beside<br />

additional expenses related to the closure of certain clinical sites should have<br />

weighed in Q1. We expect R&D effort in the range of EUR10m. Admin costs<br />

should be up YoY (up 31% to EUR3m) due to intensified launch activities ahead of<br />

the FDA decision on talactoferrin approval this summer. All in all we expect a net<br />

loss of EUR12.9m in Q1.<br />

Cash position: At the end of March 2012, we forecast Agennix net cash position to<br />

amount to EUR30.2m, translating a monthly burn rate of EUR3.5m<br />

News flow: We would not expect significant news flow in the scope of the Q1<br />

reporting. The company is likely to reiterate the time line it provided for the<br />

FORTIS M phase III data publication (July/August). Potentially, further details on<br />

the OASIS trial might be disclosed by the company. However, we would not expect<br />

a clear decision on the next development step in severe sepsis to be made before<br />

FORTIS M delivers its phase III results in NSCLC.<br />

Conclusion & Action: We would not expect meaningful news flow in the Q1<br />

reporting. Key to the investment case will be the upcoming FORTIS M phase III<br />

data publication in July/August.<br />

Page 39 of 80 European Securities Network<br />

Please refer to important disclaimer on the last page