Hedging Strategy and Electricity Contract Engineering - IFOR

Hedging Strategy and Electricity Contract Engineering - IFOR

Hedging Strategy and Electricity Contract Engineering - IFOR

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

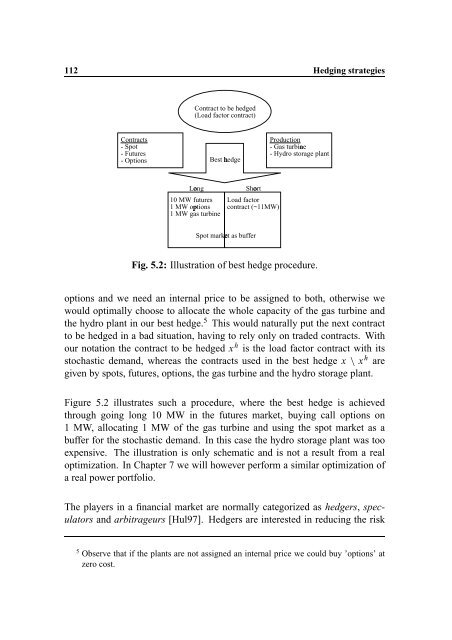

112 <strong>Hedging</strong> strategies<br />

<strong>Contract</strong> to be hedged<br />

(Load factor contract)<br />

<strong>Contract</strong>s<br />

- Spot<br />

- Futures<br />

- Options Best hÕ edge<br />

Production<br />

- Gas turbine<br />

- Hydro storage plant<br />

Ô<br />

ng LoÖ<br />

10 MW futures<br />

1 MW options<br />

1 MW gas turbine<br />

×<br />

rt ShoÖ<br />

Load factor<br />

contract (~11MW)<br />

Spot market as buffer<br />

Ø<br />

Fig. 5.2: Illustration of best hedge procedure.<br />

options <strong>and</strong> we need an internal price to be assigned to both, otherwise we<br />

would optimally choose to allocate the whole capacity of the gas turbine <strong>and</strong><br />

the hydro plant in our best hedge. 5 This would naturally put the next contract<br />

to be hedged in a bad situation, having to rely only on traded contracts. With<br />

our notation the contract to be hedged x h is the load factor contract with its<br />

stochastic dem<strong>and</strong>, whereas the contracts used in the best hedge x x h are<br />

given by spots, futures, options, the gas turbine <strong>and</strong> the hydro storage plant.<br />

Figure 5.2 illustrates such a procedure, where the best hedge is achieved<br />

through going long 10 MW in the futures market, buying call options on<br />

1 MW, allocating 1 MW of the gas turbine <strong>and</strong> using the spot market as a<br />

buffer for the stochastic dem<strong>and</strong>. In this case the hydro storage plant was too<br />

expensive. The illustration is only schematic <strong>and</strong> is not a result from a real<br />

optimization. In Chapter 7 we will however perform a similar optimization of<br />

a real power portfolio.<br />

The players in a financial market are normally categorized as hedgers, speculators<br />

<strong>and</strong> arbitrageurs [Hul97]. Hedgers are interested in reducing the risk<br />

5 Observe that if the plants are not assigned an internal price we could buy ’options’ at<br />

zero cost.