Hedging Strategy and Electricity Contract Engineering - IFOR

Hedging Strategy and Electricity Contract Engineering - IFOR

Hedging Strategy and Electricity Contract Engineering - IFOR

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

2.9 Price dynamic 37<br />

400<br />

2000<br />

350<br />

1800<br />

300<br />

1600<br />

1400<br />

NOK/MWh<br />

250<br />

200<br />

150<br />

NOK/MWh<br />

1200<br />

1000<br />

800<br />

100<br />

600<br />

400<br />

50<br />

200<br />

0<br />

1998 1999 2000<br />

0<br />

1998 1999 2000<br />

(a) Daily average<br />

(b) Hourly<br />

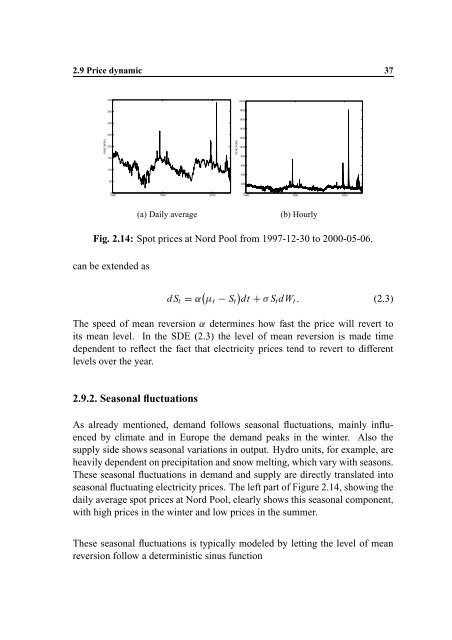

Fig. 2.14: Spot prices at Nord Pool from 1997-12-30 to 2000-05-06.<br />

can be extended as<br />

dS t R Q t S t dt F S t dW t<br />

P (2.3)<br />

The speed of mean R reversion determines how fast the price will revert to<br />

its mean level. In the SDE (2.3) the level of mean reversion is made time<br />

dependent to reflect the fact that electricity prices tend to revert to different<br />

levels over the year.<br />

2.9.2. Seasonal fluctuations<br />

As already mentioned, dem<strong>and</strong> follows seasonal fluctuations, mainly influenced<br />

by climate <strong>and</strong> in Europe the dem<strong>and</strong> peaks in the winter. Also the<br />

supply side shows seasonal variations in output. Hydro units, for example, are<br />

heavily dependent on precipitation <strong>and</strong> snow melting, which vary with seasons.<br />

These seasonal fluctuations in dem<strong>and</strong> <strong>and</strong> supply are directly translated into<br />

seasonal fluctuating electricity prices. The left part of Figure 2.14, showing the<br />

daily average spot prices at Nord Pool, clearly shows this seasonal component,<br />

with high prices in the winter <strong>and</strong> low prices in the summer.<br />

These seasonal fluctuations is typically modeled by letting the level of mean<br />

reversion follow a deterministic sinus function