Hedging Strategy and Electricity Contract Engineering - IFOR

Hedging Strategy and Electricity Contract Engineering - IFOR

Hedging Strategy and Electricity Contract Engineering - IFOR

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

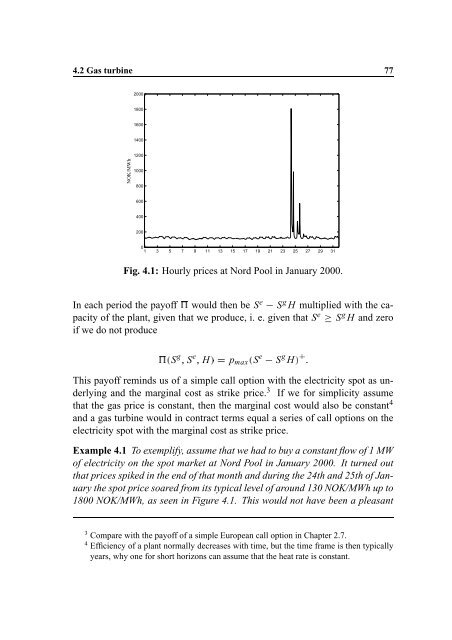

4.2 Gas turbine 77<br />

2000<br />

1800<br />

1600<br />

1400<br />

1200<br />

NOK/MWh<br />

1000<br />

800<br />

600<br />

400<br />

200<br />

0<br />

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31<br />

Fig. 4.1: Hourly prices at Nord Pool in January 2000.<br />

In each period the ˜ payoff would then be S e S g H multiplied with the capacity<br />

of the plant, given that we produce, i. e. given that S e S g H <strong>and</strong> zero<br />

if we do not produce<br />

S S eš H› p ˜{ max S e S g H› œŸž <br />

This payoff reminds us of a simple call option with the electricity spot as underlying<br />

<strong>and</strong> the marginal cost as strike price. 3 If we for simplicity assume<br />

gš<br />

that the gas price is constant, then the marginal cost would also be constant 4<br />

<strong>and</strong> a gas turbine would in contract terms equal a series of call options on the<br />

electricity spot with the marginal cost as strike price.<br />

Example 4.1 To exemplify, assume that we had to buy a constant flow of 1 MW<br />

of electricity on the spot market at Nord Pool in January 2000. It turned out<br />

that prices spiked in the end of that month <strong>and</strong> during the 24th <strong>and</strong> 25th of January<br />

the spot price soared from its typical level of around 130 NOK/MWh up to<br />

1800 NOK/MWh, as seen in Figure 4.1. This would not have been a pleasant<br />

3 Compare with the payoff of a simple European call option in Chapter 2.7.<br />

4 Efficiency of a plant normally decreases with time, but the time frame is then typically<br />

years, why one for short horizons can assume that the heat rate is constant.