- Page 1 and 2:

Life - a user’s manual Part II Gu

- Page 3 and 4:

Index Part II Society..............

- Page 5 and 6:

”Damage” on legal art Pustgrän

- Page 7 and 8:

Ekelund bridge Central bridge 7

- Page 9 and 10:

Knitted ”damage” At slussen Hor

- Page 11 and 12:

Legal och illegal Three dimensional

- Page 13 and 14:

Torsgatan Tegnérgatan 13

- Page 15 and 16:

Fatbursparken Hornsgatan Dalagatan

- Page 17 and 18:

It may seem as if the children in t

- Page 19 and 20:

In the spring, it was common for bo

- Page 21 and 22:

At the time of potato harvesting we

- Page 23 and 24:

When we became so grown up that we

- Page 25 and 26:

Another game called "Draga klönhan

- Page 27 and 28:

Sometimes we competed in agility to

- Page 29 and 30:

If we happened to have a ladder we

- Page 31 and 32:

Pawn games, as "Mary's purse" were

- Page 33 and 34:

Suspended sentence Courts may choos

- Page 35 and 36:

The economy of crime Shoplifting an

- Page 37 and 38:

Burglary in boats Coming to boats t

- Page 39 and 40:

Alcohol and drug related crimes Alc

- Page 41 and 42:

Traffic offenses As seen in table 7

- Page 43 and 44:

Get accomodation in Stockholm The p

- Page 45 and 46:

Building a house It may be cheaper

- Page 47 and 48:

Rent an office I have, a few times,

- Page 49 and 50:

Renting part of a dwelling "inheren

- Page 51 and 52:

Contact property owner Several peop

- Page 53 and 54:

Buying condominium The buyer of a c

- Page 55 and 56:

Buying a caravan To live in a carav

- Page 57 and 58:

Table 19 b Example of villas in the

- Page 59 and 60:

Although the concept possibly is un

- Page 61 and 62:

A potential benefit of having somet

- Page 63 and 64:

Another example that suggests this

- Page 65 and 66:

Twenty years later, most had centra

- Page 67 and 68:

But when a number of occupations we

- Page 69 and 70:

Political ideologies Political ideo

- Page 71 and 72:

Household economy = If all children

- Page 73 and 74:

500 years later, the Roman Empire f

- Page 75 and 76:

English, French and Dutch conqueror

- Page 77 and 78:

Table 1. When the countries that ex

- Page 79 and 80:

Malawi 1964 British colony / protec

- Page 81 and 82:

Demographic trends The year 0, ther

- Page 83 and 84:

Hungary 92 900 8,4 90,42 9,34 10,21

- Page 85 and 86:

Malaysia 6.11 23.27 5 8 573 120 2.1

- Page 87 and 88:

The long route to today's political

- Page 89 and 90:

- For economic stability and aid th

- Page 91 and 92:

State revenues In the Middle Ages,

- Page 93 and 94:

Over time, increased government tax

- Page 95 and 96:

40,0 Governement taxes and social f

- Page 97 and 98:

The most important import goods to

- Page 99 and 100:

Although tariffs and other trade ba

- Page 101 and 102:

In addition to these currencies we

- Page 103 and 104:

Government expenditure State affair

- Page 105 and 106:

Defence Owning weapons and to be fa

- Page 107 and 108:

With the population growth in the l

- Page 109 and 110:

The Swedish judicial system has rou

- Page 111 and 112:

The end of the 1800s At the end of

- Page 113 and 114:

Many ads, in particular those about

- Page 115 and 116:

Mora daily 1915 Bank & finance Cand

- Page 117 and 118:

Borås tidning, 1930 Movies Health

- Page 119 and 120:

Barometern, 1935 Beverages Health p

- Page 121 and 122:

Hudiksvallsposten, 1940 Building ma

- Page 123 and 124:

Jämtlandstidningen, 1945 Jämtland

- Page 125 and 126:

Örebrokuriren, 1950 Building mater

- Page 127 and 128:

The total country side press 4 , 19

- Page 129 and 130:

References Gröndal T (1991) Reklam

- Page 131 and 132:

Geography Differences between count

- Page 133 and 134:

Regarding other factors, like how l

- Page 135 and 136:

Estonia 99 95 5 6 123 4,1 9 392 Eth

- Page 137 and 138:

Sierra Leone 86 13 35 3 34 1,4 463

- Page 139 and 140:

Estonia 85 444 15,6 1 Estonian Kroo

- Page 141 and 142:

Sierra Leone 18 5 9,7 4 English Leo

- Page 143 and 144:

Tabell 5a. Natural Resources in rel

- Page 145 and 146:

Gabon Gambia Georgia Ghana Greece B

- Page 147 and 148:

Mali Malta Morocco Mauritania Mauri

- Page 149 and 150:

Somalia Spain Sri Lanka UK Sudan Su

- Page 151 and 152:

Bahamas 1 51 6 126 27 98 3,7 82 17

- Page 153 and 154:

Lichtenstein 19 44 0 Lithuania 33 3

- Page 155 and 156:

Uruguay 11 10 5 104 26 100 5,9 8 87

- Page 157 and 158:

Equatorial Flat with coast. 25 54 G

- Page 159 and 160:

St. Kitts and Nevis St Lucia St. Vi

- Page 161 and 162:

Dem Rep of 80 23 2 17 - 5 4 5 20 60

- Page 163 and 164:

Russia 98 87 5 2 166 4 245 16 121 2

- Page 165 and 166:

Type one hundred years after Buddha

- Page 167 and 168:

In 1154 Burma's pride, the then Hin

- Page 169 and 170:

Religions create some obvious diffe

- Page 171 and 172:

Ghana 13 5 4 4 71 33 3 19 23 1 920

- Page 173 and 174:

Vanuatu 52 5 4 3 119 1 38 27 3 127

- Page 175 and 176:

Estonia 99 95 5 6 123 4 444 16 167

- Page 177 and 178:

Sri Lanka 95 98 91 20 3 83 2 58 1 8

- Page 179 and 180:

An important question to ask yourse

- Page 181 and 182:

As a, personal assistant to a handi

- Page 183 and 184:

9 8 7 6 5 4 3 2 Control over the wo

- Page 185 and 186:

Table 1. Grading of a number of wor

- Page 187 and 188:

Organized meetings Another phenomen

- Page 189 and 190:

Challenges When I’we been newly e

- Page 191 and 192:

Personal development Personal devel

- Page 193 and 194:

A very important part of the activi

- Page 195 and 196:

The latter since the difference bet

- Page 197 and 198:

Generally I find that the less phys

- Page 199 and 200:

It is quite common that the employe

- Page 201 and 202:

Tabell 5. What skills as a mechanic

- Page 203 and 204:

Stress Stress is a physical reactio

- Page 205 and 206:

About getting rich What’s wealth

- Page 207 and 208:

Income and expenditure Someone who

- Page 209 and 210: Investments in securities As far as

- Page 211 and 212: For those who avoid crisis companie

- Page 213 and 214: Summary of the interest on mortgage

- Page 215 and 216: Before the IT crash in 2001 everyth

- Page 217 and 218: As hopefully seen in the earlier re

- Page 219 and 220: It does need not be difficult to, a

- Page 221 and 222: On the other hand, the average temp

- Page 223 and 224: A variant to trading stocks is to t

- Page 225 and 226: Currency trading I have no experien

- Page 227 and 228: Retirement savings Those who discus

- Page 229 and 230: But this model is only partially tr

- Page 231 and 232: The state think that the forest is

- Page 233 and 234: 0,60 Average price each year SEK /k

- Page 235 and 236: Apartment blocks You can either buy

- Page 237 and 238: Individual homes An alternative to

- Page 239 and 240: Regulatory requirements Just as in

- Page 241 and 242: Deicing and snow on stairs, etc. If

- Page 243 and 244: Water traps and floor drains in hom

- Page 245 and 246: Table 1a. Proposed checkpoints for

- Page 247 and 248: Table 1c. Proposed checkpoints for

- Page 249 and 250: Bath, toilet and kitchen Unsecure e

- Page 251 and 252: Table 1f. Proposed checkpoints for

- Page 253 and 254: Bad water pipes It is common in old

- Page 255 and 256: Facade damage, brick facades Brick

- Page 257 and 258: Burglary and vandalism Researchers

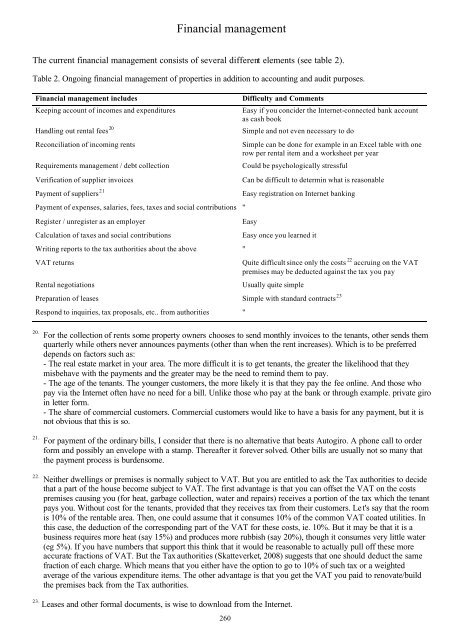

- Page 259: Contractors When an action is decid

- Page 263 and 264: Social management My experience is

- Page 265 and 266: Increase the area that generate rev

- Page 267 and 268: References Arbetsmiljöverket (2005

- Page 269 and 270: Here are some suggestions: Ergonomi

- Page 271 and 272: Although physical deficiencies in t

- Page 273 and 274: Service production has in some case

- Page 275 and 276: In general, work environment polici

- Page 277 and 278: Languages A quick lesson in languag

- Page 279 and 280: Nouns continued English Swedish Fre

- Page 281 and 282: Weekdays and months English Swedish

- Page 283 and 284: Figures English Swedish French 2 Sp

- Page 285 and 286: Miscellaneous continued. English Sw

- Page 287 and 288: Capital letters and paragraphs Sent

- Page 289 and 290: How nouns are All words that descri

- Page 291 and 292: Short vowels are not always followe

- Page 293 and 294: Sometimes it is not en but ett Abou

- Page 295 and 296: Var means the same as är but in th

- Page 297 and 298: Then for some reason you use mer (m

- Page 299 and 300: Twenty should be called tvåtio Num

- Page 301 and 302: A quick lesson in writing Probably

- Page 303 and 304: Damn, I have to hide myself, it's t

- Page 305 and 306: - I will probably go home now, I mu

- Page 307 and 308: Anyone who has ambition to make a g

- Page 309 and 310: It may be easier to find something

- Page 311 and 312:

However, it is not necessarily to a

- Page 313 and 314:

2. In the eye’s of the described

- Page 315 and 316:

It is obviously important that peop

- Page 317 and 318:

The events should, as well as the t

- Page 319 and 320:

From the outside Objectively Anyone

- Page 321 and 322:

It could certainly be done in a muc

- Page 323 and 324:

The confusion regarding who says wh

- Page 325 and 326:

Introductions Some think that the f

- Page 327 and 328:

Checklist - Do not poke and modify

- Page 329 and 330:

About proverbs Proverbs are complet

- Page 331 and 332:

Quite a number of proverbs in the A

- Page 333 and 334:

There are many more proverbs in the

- Page 335 and 336:

Many children books and comics are

- Page 337 and 338:

Animals maybe not knew how to use a

- Page 339 and 340:

How can a dog talk to a bird But if

- Page 341 and 342:

Have you read any fairtails There c

- Page 343 and 344:

The history of amusements 343

- Page 345 and 346:

Visual arts Paintings After visitin

- Page 347 and 348:

Abstract It is difficult to see tha

- Page 349 and 350:

Photo art Most cases in which someo

- Page 351 and 352:

In addition, musicians was given a

- Page 353 and 354:

In the 1960s, however, created the

- Page 355 and 356:

Radio and moving pictures Radio 192

- Page 357 and 358:

TV 1920-50's television technology

- Page 359 and 360:

Performing arts Circus Circus is cr

- Page 361 and 362:

Musical The musical is said to be d

- Page 363 and 364:

La donna del lago 1819 10 Gioachino

- Page 365 and 366:

Theater Probably the church dominat

- Page 367 and 368:

Sports People probably has competed

- Page 369 and 370:

Football. They have found evidence

- Page 371 and 372:

Games Playing cards may have been u

- Page 373 and 374:

Journals The world's first daily ne

- Page 375 and 376:

Probably everyone appreciates a rep

- Page 377 and 378:

One reason could be that the art ph

- Page 379 and 380:

73% of the photographic works at th

- Page 381 and 382:

Jus as regarding photography, every

- Page 383 and 384:

One explanation for the differences

- Page 385 and 386:

The purpose of sports consumption W

- Page 387 and 388:

Table 2. Selection of Sweden/Swedes

- Page 389 and 390:

Table 3. Roughly the number of page

- Page 391 and 392:

The purpose of pets From a human pe

- Page 393 and 394:

Table 3. The participants' percepti