Gazprom-AR2014

Gazprom-AR2014

Gazprom-AR2014

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

52<br />

Trends and Developments on Oil and Gas Markets<br />

The more favourable business conditions for independent producers include the following:<br />

— no restrictions on gas prices; opportunity to offer discounts to the regulated price;<br />

— lower costs of gas transportation due to shorter distances;<br />

— lower tax burden, with the mineral extraction tax rates by 1.5x lower for independent producers<br />

than for OAO <strong>Gazprom</strong>;<br />

— priority access to OAO <strong>Gazprom</strong>’s gas transportation system for suppliers of dry stripped gas<br />

produced by refining associated petroleum gas (APG).<br />

At the same time, independent producers supply almost no gas to households, while <strong>Gazprom</strong><br />

is bound by social obligations to act as the household supplier of last resort.<br />

Exchange gas trading provides a very useful tool for shaping the market principles and improving<br />

pricing transparency on the gas market, as well as an opportunity to register market indicators<br />

to form a pricing system. In 2013, in order to form market-driven pricing principles, <strong>Gazprom</strong><br />

was authorised by law to sell up to 17.5 bcm of gas at unregulated prices through organised<br />

trading (commodity exchanges and trading systems).<br />

Since October 2014, OAO <strong>Gazprom</strong>, jointly with ZAO Saint-Petersburg International Mercantile<br />

Exchange and ZAO Settlement depository company, arranged an organised natural gas<br />

auction with one-month supply deadlines at ZAO Saint-Petersburg International Mercantile<br />

Exchange. Between October and December of 2014, the exchange hosted the first gas trades in<br />

the Natural Gas section, at which OAO <strong>Gazprom</strong> successfully sold 429.4 mmcm of gas.<br />

In order to further expand gas exchange trading on the Russian market, OAO <strong>Gazprom</strong><br />

is contributing to the improvement of the legal and regulatory framework regulating the Russian<br />

gas market. <strong>Gazprom</strong> Group is carrying out a comprehensive study to evaluate OAO <strong>Gazprom</strong>’s<br />

opportunities to expand gas supplies to the domestic market and exports through exchange trading<br />

under the competitive pressure from other fuel and energy resources and other natural gas<br />

suppliers in the state-regulated gas sector.<br />

Competing unconventional hydrocarbon producers, LNG market conditions<br />

Today’s attention to unconventional gas (primarily shale gas) has been driven by an unprecedented<br />

growth in its production in the USA in the recent years. Only the USA and Canada still produce<br />

commercially significant volumes of shale gas. None of that is supplied outside North America. In<br />

other regions (Europe, China, Australia, Argentina and Saudi Arabia), the shale gas branch is still<br />

at its infancy stage. This means zero competition from shale gas in international markets to which<br />

OAO <strong>Gazprom</strong> supplies, or plans to supply, gas from Russia.<br />

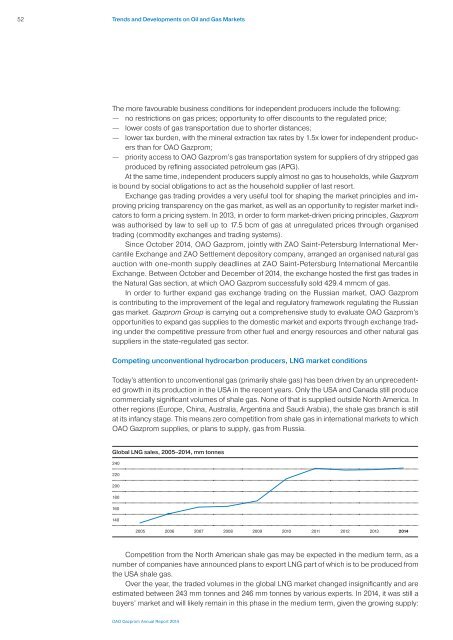

Global LNG sales, 2005–2014, mm tonnes<br />

240<br />

220<br />

200<br />

180<br />

160<br />

140<br />

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014<br />

Competition from the North American shale gas may be expected in the medium term, as a<br />

number of companies have announced plans to export LNG part of which is to be produced from<br />

the USA shale gas.<br />

Over the year, the traded volumes in the global LNG market changed insignificantly and are<br />

estimated between 243 mm tonnes and 246 mm tonnes by various experts. In 2014, it was still a<br />

buyers’ market and will likely remain in this phase in the medium term, given the growing supply:<br />

OAO <strong>Gazprom</strong> Annual Report 2014