- Page 1 and 2:

STANDING COMMITTEE ON RULES OF PRAC

- Page 3 and 4:

July 30, 2003 ONE HUNDRED FIFTY-SEC

- Page 5 and 6:

P. 26 (a)(3). New Committee notes p

- Page 7 and 8:

In Category Eleven are a proposed a

- Page 9 and 10:

For the guidance of the Court and t

- Page 11 and 12:

(c) After Dismissal by the District

- Page 13 and 14:

MARYLAND RULES OF PROCEDURE TITLE 3

- Page 15 and 16:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 17 and 18:

has jurisdiction for the purposes o

- Page 19 and 20:

whether a transfer will result in u

- Page 21 and 22:

action was not entitled to be trans

- Page 23 and 24:

notice of intention to defend or ot

- Page 25 and 26:

individual members of the class tha

- Page 27 and 28:

or complication in the presentation

- Page 29 and 30:

REPORTER’S NOTE The Rules Committ

- Page 31 and 32:

compromise shall be given to stockh

- Page 33 and 34:

contended that there is a genuine d

- Page 35 and 36:

When a ruling upon on a motion for

- Page 37 and 38:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 39 and 40:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 41 and 42:

motions. Cross reference: Rule 2-31

- Page 43 and 44:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 45 and 46:

of any insurance agreement under wh

- Page 47 and 48:

written report made by the expert c

- Page 49 and 50:

Subsection (f)(1) is derived in par

- Page 51 and 52:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 53 and 54:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 55 and 56:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 57 and 58:

allowed. The transcript may then be

- Page 59 and 60:

transcript was not signed and retur

- Page 61 and 62:

was present or represented at the t

- Page 63 and 64:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 65 and 66:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 67 and 68:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 69 and 70:

REPORTER’S NOTE The proposed dele

- Page 71 and 72:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 73 and 74:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 75 and 76:

decisions made at the conference. T

- Page 77 and 78:

REPORTER’S NOTE The proposed amen

- Page 79 and 80:

MARYLAND RULES OF PROCEDURE TITLE 4

- Page 81 and 82:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 83 and 84:

MARYLAND RULES OF PROCEDURE APPENDI

- Page 85 and 86:

REPORTER'S NOTE The proposed amendm

- Page 87 and 88:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 89 and 90:

may direct that prospective jurors

- Page 91 and 92:

one peremptory challenge for each g

- Page 93 and 94:

MARYLAND RULES OF PROCEDURE TITLE 4

- Page 95 and 96:

(c) Jury List Before the examinatio

- Page 97 and 98:

(g) (h) Designation of List of Qual

- Page 99 and 100:

The court shall appoint at least tw

- Page 101 and 102:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 103 and 104:

Proposed amendments to Rules 2-521

- Page 105 and 106:

to writing may be taken into the ju

- Page 107 and 108:

(c) "Verdict" Defined For purposes

- Page 109 and 110:

process is not made and the summons

- Page 111 and 112:

and time for trial of the action. W

- Page 113 and 114:

MARYLAND RULES OF PROCEDURE TITLE 3

- Page 115 and 116:

sufficient to allow the plaintiff t

- Page 117 and 118:

(5) A defendant who is served with

- Page 119 and 120:

MARYLAND RULES OF PROCEDURE TITLE 3

- Page 121 and 122:

Rule 4-216. PRETRIAL RELEASE (a) In

- Page 123 and 124:

Article, §5-202 (b), (c), (d), or

- Page 125 and 126:

or the alleged victim’s premises

- Page 127 and 128:

Recommendation of the Rules Committ

- Page 129 and 130:

commissioner's pretrial release det

- Page 131 and 132:

REPORTER’S NOTE The Pretrial Rele

- Page 133 and 134:

under subsection (e)(4)(B). A third

- Page 135 and 136:

copy of the notice shall be furnish

- Page 137 and 138:

REPORTER’S NOTE In his June 21, 2

- Page 139 and 140:

MARYLAND RULES OF PROCEDURE TITLE 4

- Page 141 and 142:

MARYLAND RULES OF PROCEDURE TITLE 4

- Page 143 and 144:

"Information" means a charging docu

- Page 145 and 146:

With the addition of the definition

- Page 147 and 148:

opportunity for hearing, may requir

- Page 149 and 150:

emoval shall designate the county t

- Page 151 and 152:

MARYLAND RULES OF PROCEDURE TITLE 4

- Page 153 and 154:

MARYLAND RULES OF PROCEDURE TITLE 4

- Page 155 and 156:

certain circumstances. (f) Allocuti

- Page 157 and 158: (2) District Court Upon the entry o

- Page 159 and 160: MARYLAND RULES OF PROCEDURE TITLE 4

- Page 161 and 162: MARYLAND RULES OF PROCEDURE TITLE 4

- Page 163 and 164: ond hereby secured remains undischa

- Page 165 and 166: REPORTER’S NOTE The proposed amen

- Page 167 and 168: disposition or a General Waiver and

- Page 169 and 170: imprisonment; and I am not now a de

- Page 171 and 172: company, unincorporated association

- Page 173 and 174: _____________________________ _____

- Page 175 and 176: personal representative and consent

- Page 177 and 178: _______________________________ ___

- Page 179 and 180: contents of the foregoing schedule

- Page 181 and 182: writing, shall set forth the relief

- Page 183 and 184: in the presence of the Register of

- Page 185 and 186: MARYLAND RULES OF PROCEDURE TITLE 6

- Page 187 and 188: otherwise delivers to the creditor

- Page 189 and 190: MARYLAND RULES OF PROCEDURE TITLE 6

- Page 191 and 192: Date: __________________ __________

- Page 193 and 194: MARYLAND RULES OF PROCEDURE TITLE 6

- Page 195 and 196: following form: [CAPTION] NOTICE OF

- Page 197 and 198: MARYLAND RULES OF PROCEDURE TITLE 6

- Page 199 and 200: MARYLAND RULES OF PROCEDURE TITLE 6

- Page 201 and 202: MARYLAND RULES OF PROCEDURE TITLE 6

- Page 203 and 204: 3. I acknowledge that I must file a

- Page 205 and 206: Modified Administration, the person

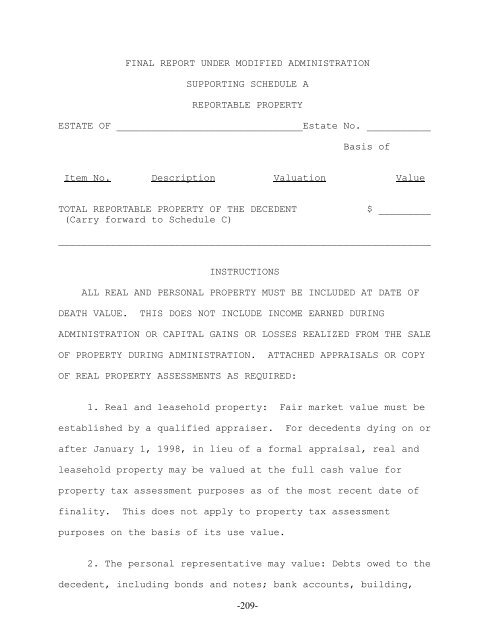

- Page 207: Inventory and Account, as required,

- Page 211 and 212: ATTACH ADDITIONAL SCHEDULES AS NEED

- Page 213 and 214: which qualify the personal represen

- Page 215 and 216: CONSENT TO EXTEND TIME TO FILE FINA

- Page 217 and 218: MARYLAND RULES OF PROCEDURE TITLE 6

- Page 219 and 220: MARYLAND RULES OF PROCEDURE TITLE 6

- Page 221 and 222: MARYLAND RULES OF PROCEDURE TITLE 6

- Page 223 and 224: MARYLAND RULES OF PROCEDURE TITLE 7

- Page 225 and 226: equired for trial or any other proc

- Page 227 and 228: MARYLAND RULES OF PROCEDURE TITLE 7

- Page 229 and 230: REPORTER’S NOTE The Rules Committ

- Page 231 and 232: MARYLAND RULES OF PROCEDURE TITLE 8

- Page 233 and 234: the briefs filed. (6) Any motion fo

- Page 235 and 236: pages in length. Within ten days af

- Page 237 and 238: MARYLAND RULES OF PROCEDURE TITLE 8

- Page 239 and 240: MARYLAND RULES OF PROCEDURE TITLE 8

- Page 241 and 242: the Court of Appeals shall certify,

- Page 243 and 244: proceedings; or (3) in a criminal c

- Page 245 and 246: appellee's brief together with a st

- Page 247 and 248: included in all copies of the recor

- Page 249 and 250: appellant/cross-appellee shall file

- Page 251 and 252: include the circuit court docket en

- Page 253 and 254: (c) Covers color: A brief shall hav

- Page 255 and 256: espect to the case, including an or

- Page 257 and 258: numbered, indicating the legal prop

- Page 259 and 260:

MARYLAND RULES OF PROCEDURE TITLE 8

- Page 261 and 262:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 263 and 264:

Cross reference: Code, Estates and

- Page 265 and 266:

Source: This Rule is derived as fol

- Page 267 and 268:

nature, extent, and probable durati

- Page 269 and 270:

prior to July 1, 2001, but the fact

- Page 271 and 272:

(e) (f) Permitted Disclosure . . .

- Page 273 and 274:

(c) Form of Petition The petition s

- Page 275 and 276:

of the Court of Appeals also shall

- Page 277 and 278:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 279 and 280:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 281 and 282:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 283 and 284:

accordance with Rule 16-752 to hold

- Page 285 and 286:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 287 and 288:

including on a court holiday or aft

- Page 289 and 290:

(c) Refusal to Perform Ceremony A j

- Page 291 and 292:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 293 and 294:

(vi) implementation and enforcement

- Page 295 and 296:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 297 and 298:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 299 and 300:

Rule; (2) within the two-year perio

- Page 301 and 302:

follows: MARYLAND RULES OF PROCEDUR

- Page 303 and 304:

agreement may include provisions st

- Page 305 and 306:

alternative dispute resolution proc

- Page 307 and 308:

Administrative Office of the Courts

- Page 309 and 310:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 311 and 312:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 313 and 314:

REPORTER’S NOTE The Implementatio

- Page 315 and 316:

(C) legislation that may affect the

- Page 317 and 318:

The Executive Committee shall conve

- Page 319 and 320:

exercise, naming the date; and (3)

- Page 321 and 322:

MARYLAND RULES OF PROCEDURE RULES G

- Page 323 and 324:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 325 and 326:

REPORTER’S NOTE See the Reporter

- Page 327 and 328:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 329 and 330:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 331 and 332:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 333 and 334:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 335 and 336:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 337 and 338:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 339 and 340:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 341 and 342:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 343 and 344:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 345 and 346:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 347 and 348:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 349 and 350:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 351 and 352:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 353 and 354:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 355 and 356:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 357 and 358:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 359 and 360:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 361 and 362:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 363 and 364:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 365 and 366:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 367 and 368:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 369 and 370:

MARYLAND RULES OF PROCEDURE TITLE 2

- Page 371 and 372:

MARYLAND RULES OF PROCEDURE TITLE 3

- Page 373 and 374:

MARYLAND RULES OF PROCEDURE TITLE 3

- Page 375 and 376:

MARYLAND RULES OF PROCEDURE TITLE 3

- Page 377 and 378:

MARYLAND RULES OF PROCEDURE TITLE 3

- Page 379 and 380:

MARYLAND RULES OF PROCEDURE TITLE 3

- Page 381 and 382:

MARYLAND RULES OF PROCEDURE TITLE 3

- Page 383 and 384:

MARYLAND RULES OF PROCEDURE TITLE 3

- Page 385 and 386:

MARYLAND RULES OF PROCEDURE TITLE 3

- Page 387 and 388:

MARYLAND RULES OF PROCEDURE TITLE 3

- Page 389 and 390:

MARYLAND RULES OF PROCEDURE TITLE 3

- Page 391 and 392:

MARYLAND RULES OF PROCEDURE TITLE 3

- Page 393 and 394:

MARYLAND RULES OF PROCEDURE TITLE 3

- Page 395 and 396:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 397 and 398:

production to the court upon the re

- Page 399 and 400:

follows: MARYLAND RULES OF PROCEDUR

- Page 401 and 402:

MARYLAND RULES OF PROCEDURE TITLE 3

- Page 403 and 404:

Proof of service and mailing shall

- Page 405 and 406:

Proof of service and mailing shall

- Page 407 and 408:

9 malicious destruction of property

- Page 409 and 410:

peace order” or a “final peace

- Page 411 and 412:

MARYLAND RULES OF PROCEDURE TITLE 5

- Page 413 and 414:

MARYLAND RULES OF PROCEDURE TITLE 9

- Page 415 and 416:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 417 and 418:

circulation in the county in which

- Page 419 and 420:

an affidavit (A) that the person ha

- Page 421 and 422:

MARYLAND RULES OF PROCEDURE TITLE 1

- Page 423 and 424:

Additionally, the amendments requir

- Page 425 and 426:

things, it will prevent the practic

- Page 427:

injuries. Identify all persons with