- Page 1 and 2: ECONOMIC REPORT OF THE PRESIDENT To

- Page 4: C O N T E N T S ECONOMIC REPORT OF

- Page 8 and 9: economic report of the president To

- Page 10 and 11: year-old. In the meantime, I’m go

- Page 12: the annual report of the council of

- Page 16 and 17: C O N T E N T S CHAPTER 1. PROMOTIN

- Page 18 and 19: APPENDIX 1: COMPONENTS OF THE RECOV

- Page 20 and 21: THE OBAMA ADMINISTRATION’S RECORD

- Page 22 and 23: 2.15. Housing Starts, 1960-2013....

- Page 24 and 25: 3.1. Forecasted and Actual Real GDP

- Page 26 and 27: C H A P T E R 1 PROMOTING OPPORTUNI

- Page 28 and 29: Opportunity, Growth, and Security i

- Page 32 and 33: Figure 1-4 Real GDP Per Working-Age

- Page 34 and 35: Figure 1-6 Change in Poverty Rate F

- Page 36 and 37: Figure 1-7 Domestic Crude Oil Produ

- Page 38 and 39: Figure 1-8 Growth in Real Per Capit

- Page 40 and 41: Figure 1-9 Unemployment Rate by Dur

- Page 42 and 43: e needed to make up for a decades-l

- Page 44 and 45: Annual percent change 2.50 15-year

- Page 46 and 47: Figure 1-14 Share of National Incom

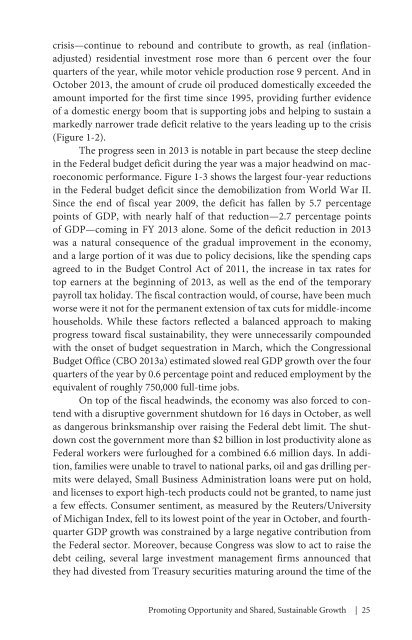

- Page 48: Along with steps that create jobs,

- Page 51 and 52: corner, with purchases increasing d

- Page 53 and 54: the four quarters of 2013, or enoug

- Page 55 and 56: Percent of GDP 12 10 8 6 4 2 0 -2 -

- Page 57 and 58: Percent 5.0 4.0 3.0 2.0 Figure 2-3

- Page 59 and 60: In the euro area, the unemployment

- Page 61 and 62: Figure 2-6 Cumulative Flows into Mu

- Page 63 and 64: Figure 2-7 Household Deleveraging,

- Page 65 and 66: Box 2-1: The 2013 Comprehensive Rev

- Page 67 and 68: Percent 25 20 15 10 5 0 -5 Figure 2

- Page 69 and 70: Figure 2-11 State and Local Pension

- Page 71 and 72: Percent of GDP 2 1 0 Figure 2-14 Cu

- Page 73 and 74: Box 2-2. Administration Trade Polic

- Page 75 and 76: Upon completion, the TPP and T-TIP

- Page 77 and 78: percent of households report that i

- Page 79 and 80: Figure 2-18 Petroleum Net Imports,

- Page 81 and 82:

Figure 2-21 U.S. Per Capita Consump

- Page 83 and 84:

Percent 11 Figure 2-22 Unemployment

- Page 85 and 86:

Figure 2-25 Predicted vs. Actual Ma

- Page 87 and 88:

Box 2-4: Unemployment Duration and

- Page 89 and 90:

The Long-Term Outlook The 11-Year F

- Page 91 and 92:

Growth in GDP over the Long Term As

- Page 93 and 94:

Box 2-5: Immigration Reform and Pot

- Page 95 and 96:

Even with this growth, however, the

- Page 97 and 98:

families. The other half was for in

- Page 99 and 100:

ecause of rapidly declining stock a

- Page 101 and 102:

Obama Administration and the 111th

- Page 103 and 104:

Figure 3-1 Recovery Act Programs by

- Page 105 and 106:

other cases, new measures expanded

- Page 107 and 108:

Figure 3-2 Recovery Act and Subsequ

- Page 109 and 110:

Box 3-1: Other Administration Polic

- Page 111 and 112:

challenges, and how economists have

- Page 113 and 114:

Table 3-5 Estimated Output Multipli

- Page 115 and 116:

Figure 3-7 Quarterly Effect of the

- Page 117 and 118:

Table 3-6 Estimates of the Effects

- Page 119 and 120:

International Comparison The 2008 c

- Page 121 and 122:

Box 3-2: The U.S. Recovery in Compa

- Page 123 and 124:

Table 3-7 Tax Relief and Income Sup

- Page 125 and 126:

traditionally been jointly financed

- Page 127 and 128:

downturn in the economy. Even thoug

- Page 129 and 130:

Figure 3-11 Recovery Act Cumulative

- Page 131 and 132:

The Recovery Act also invested in r

- Page 133 and 134:

helped individuals who chose to ret

- Page 135 and 136:

the period, even though total power

- Page 137 and 138:

average—then the resulting increa

- Page 139 and 140:

Alternative Minimum Tax relief, bus

- Page 141 and 142:

Through the end of a Individual Tax

- Page 143 and 144:

y Poterba (1994), states and locali

- Page 145 and 146:

Table 3-11 Fiscal Support for the E

- Page 147 and 148:

spells. Because the resulting unemp

- Page 149 and 150:

literature uses two different appro

- Page 151 and 152:

Table 3-12 Summary of Cross-Section

- Page 153 and 154:

the CMS projections show real per-c

- Page 155 and 156:

will accrue to workers as higher wa

- Page 157 and 158:

Box 4-1: Two Measures of Growth in

- Page 159 and 160:

Figure 4-1 Growth in Real Per Capit

- Page 161 and 162:

in particular may not exactly track

- Page 163 and 164:

find that even those seniors who di

- Page 165 and 166:

the slowdown in real (that is, infl

- Page 167 and 168:

health care costs for an individual

- Page 169 and 170:

estimate for the ACA found that its

- Page 171 and 172:

Figure 4-4 Medicare 30-Day, All-Con

- Page 173 and 174:

agreements among the providers them

- Page 175 and 176:

payment for physician services, the

- Page 177 and 178:

Box 4-3: The Cost Slowdown and ACA

- Page 179 and 180:

2010a; 2011; 2012c; 2013a; 2014), w

- Page 181 and 182:

Figure 4-6 Recent CBO Projections o

- Page 183 and 184:

Conclusion The evidence is clear th

- Page 185 and 186:

facilitated this private-sector tec

- Page 187 and 188:

esulting gap between the actual gro

- Page 189 and 190:

Table 5-1 Sources of Productivity I

- Page 191 and 192:

Table 5-2 Nonfarm Private Business

- Page 193 and 194:

of the productivity improvement res

- Page 195 and 196:

Figure 5-3 Growth in Productivity a

- Page 197 and 198:

improving and college completion ra

- Page 199 and 200:

Box 5-2: Does Inequality Affect Pro

- Page 201 and 202:

Percent 3.5 Figure 5-5 Composition

- Page 203 and 204:

• Just two of the largest U.S. te

- Page 205 and 206:

Box 5-3: Just-in-Time Manufacturing

- Page 207 and 208:

Figure 5-7 Exclusive and Shared All

- Page 209 and 210:

Box 5-4: Spectrum Investment Polici

- Page 211 and 212:

To stimulate investment in more adv

- Page 213 and 214:

Because current uses of technology

- Page 215 and 216:

Box 5-5: Electronic Health Records

- Page 217 and 218:

about the array of services and sup

- Page 219 and 220:

and, in such cases, provides partie

- Page 221 and 222:

Box 5-6: The Leahy-Smith America In

- Page 223 and 224:

Box 5-7: Pay-For-Delay Settlements

- Page 226 and 227:

C H A P T E R 6 THE WAR ON POVERTY

- Page 228 and 229:

Measuring Poverty: Who is Poor in A

- Page 230 and 231:

thresholds ever since. These dollar

- Page 232 and 233:

of necessary items, including food,

- Page 234 and 235:

Table 6-1 Poverty Rates by Selected

- Page 236 and 237:

Box 6-3: Women and Poverty While wo

- Page 238 and 239:

However, this reflects smaller decl

- Page 240 and 241:

Percent 25 Figure 6-1 Trends in the

- Page 242 and 243:

Box 6-4: Social Programs Serve All

- Page 244 and 245:

of low- and middle-income workers a

- Page 246 and 247:

particularly valuable since they es

- Page 248 and 249:

Figure 6-4 Official vs Anchored Sup

- Page 250 and 251:

deep market poverty driven by the b

- Page 252 and 253:

work: in 2010, for example, unemplo

- Page 254 and 255:

out of poverty through job training

- Page 256 and 257:

e noted that researchers have found

- Page 258 and 259:

2012). Among the children of low-ea

- Page 260 and 261:

Education appears to be one of the

- Page 262 and 263:

Friedman, and Rockoff (2011) find t

- Page 264 and 265:

including an additional $25 a week

- Page 266 and 267:

Figure 6-11 Recovery Act and Subseq

- Page 268 and 269:

Empowering Every Child with a Quali

- Page 270 and 271:

modernize America’s high schools

- Page 272 and 273:

low-income Americans and their chil

- Page 274 and 275:

C H A P T E R 7 EVALUATION AS A TOO

- Page 276 and 277:

program evaluation efforts. For exa

- Page 278 and 279:

went to preschool would have had if

- Page 280 and 281:

y adopting successful interventions

- Page 282 and 283:

Box 7-2: Using Behavioral Economics

- Page 284 and 285:

Box 7-3: “Rapid Cycle” Evaluati

- Page 286 and 287:

Figure 7-1 Outlays for Grants to St

- Page 288 and 289:

performance data, fewer than half o

- Page 290 and 291:

Investment Act programs. The PROMIS

- Page 292 and 293:

Figure 7-2 Inventory of Beds for Ho

- Page 294 and 295:

example, included a nondiscretionar

- Page 296 and 297:

Other benefits of considering evalu

- Page 298 and 299:

with the treatment effect and thus

- Page 300 and 301:

unemployment insurance wage and ben

- Page 302 and 303:

hard for researchers to access for

- Page 304 and 305:

REFERENCES Chapter 1 Almunia, Migue

- Page 306 and 307:

____. 2014. “Press Release: Janua

- Page 308 and 309:

and the TPP at the Peterson Institu

- Page 310 and 311:

Increase Employment Evidence from t

- Page 312 and 313:

___. 2010b. “The Economic Impact

- Page 314 and 315:

___. 2012. World Economic Outlook A

- Page 316 and 317:

Polak Annual Research Conference. W

- Page 318 and 319:

Baicker, Katherine and Amitabh Chan

- Page 320 and 321:

Daly, Mary, Bart Hobijn, and Brian

- Page 322 and 323:

Nominal Wages,” International Jou

- Page 324 and 325:

Learning: A Meta-Analysis and Revie

- Page 326 and 327:

Chien, Colleen V. 2012. “Reformin

- Page 328 and 329:

GAO (Government Accountability Offi

- Page 330 and 331:

Jorgenson, Dale. 2001. “Informati

- Page 332 and 333:

Integration in Economic Development

- Page 334 and 335:

_____. 2007. “Improving the Safet

- Page 336 and 337:

Dahl, Gordon B. and Lance Lochner.

- Page 338 and 339:

Heckman, James J. and Dimitriy V. M

- Page 340 and 341:

Ludwig, Jens and Douglas Miller. 20

- Page 342 and 343:

Sharkey, Patrick. 2009. “Neighbor

- Page 344 and 345:

_____. 2013. “Practical Evaluatio

- Page 346 and 347:

www.nij.gov/topics/corrections/comm

- Page 348:

Stock, James H., and Mark Watson. 2

- Page 352 and 353:

letter of transmittal Council of Ec

- Page 354:

Council Members and Their Dates of

- Page 357 and 358:

The Members of the Council Betsey S

- Page 359 and 360:

Act has had on reducing health care

- Page 361 and 362:

Statistical Office The Statistical

- Page 364:

A P P E N D I X B STATISTICAL TABLE

- Page 367 and 368:

INTEREST RATES, MONEY STOCK, AND GO

- Page 369 and 370:

2013-to-2014 TABLE NUMBER MATCH 201

- Page 371 and 372:

Year or quarter Table B-1. Percent

- Page 373 and 374:

Table B-2. Gross domestic product,

- Page 375 and 376:

Table B-3. Quantity and price index

- Page 377 and 378:

Table B-5. Real exports and imports

- Page 379 and 380:

Year Total 2 Table B-7. Real farm i

- Page 381 and 382:

Table B-9. Median money income (in

- Page 383 and 384:

Year or month Civilian noninstituti

- Page 385 and 386:

Year or month All civilian workers

- Page 387 and 388:

Table B-14. Employees on nonagricul

- Page 389 and 390:

Table B-15. Hours and earnings in p

- Page 391 and 392:

Year and month Interest Rates, Mone

- Page 393 and 394:

Year and month Table B-18. Money st

- Page 395 and 396:

Table B-20. Federal receipts, outla

- Page 397 and 398:

Table B-22. Federal receipts, outla

- Page 399 and 400:

Table B-24. State and local governm

- Page 401 and 402:

End of month Table B-26. Estimated

- Page 403 and 404:

B-7. Chain-type price indexes for g

- Page 405 and 406:

B-28. National income by type of in

- Page 407 and 408:

B-48. Employment cost index, privat

- Page 409 and 410:

B-65. Producer price indexes by sta

- Page 411 and 412:

B-81. Federal receipts, outlays, su

- Page 413 and 414:

B-99. Farm output and productivity

- Page 415:

B-111. International reserves Inter