Regional Markets

56ec00c44c641_local-markets-book_complete_LR

56ec00c44c641_local-markets-book_complete_LR

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Regional</strong> <strong>Markets</strong> for Local Development<br />

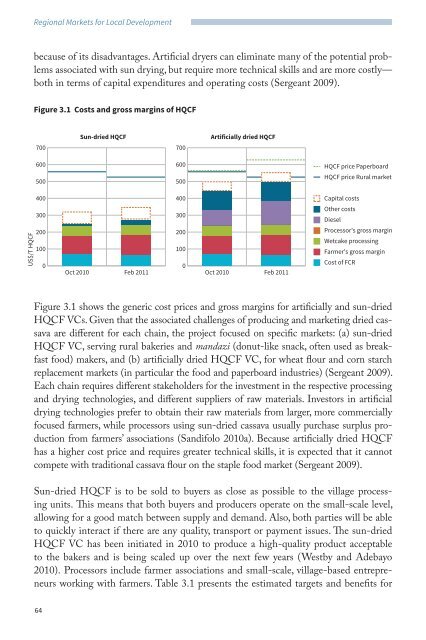

because of its disadvantages. Artificial dryers can eliminate many of the potential problems<br />

associated with sun drying, but require more technical skills and are more costly—<br />

both in terms of capital expenditures and operating costs (Sergeant 2009).<br />

Figure 3.1 Costs and gross margins of HQCF<br />

700<br />

Sun-dried HQCF<br />

700<br />

Artificially dried HQCF<br />

600<br />

500<br />

600<br />

500<br />

HQCF price Paperboard<br />

HQCF price Rural market<br />

US$/T HQCF<br />

400<br />

300<br />

200<br />

100<br />

0<br />

Oct 2010<br />

Feb 2011<br />

400<br />

300<br />

200<br />

100<br />

0<br />

Oct 2010<br />

Feb 2011<br />

Capital costs<br />

Other costs<br />

Diesel<br />

Processor's gross margin<br />

Wetcake processing<br />

Farmer's gross margin<br />

Cost of FCR<br />

Figure 3.1 shows the generic cost prices and gross margins for artificially and sun-dried<br />

HQCF VCs. Given that the associated challenges of producing and marketing dried cassava<br />

are different for each chain, the project focused on specific markets: (a) sun-dried<br />

HQCF VC, serving rural bakeries and mandazi (donut-like snack, often used as breakfast<br />

food) makers, and (b) artificially dried HQCF VC, for wheat flour and corn starch<br />

replacement markets (in particular the food and paperboard industries) (Sergeant 2009).<br />

Each chain requires different stakeholders for the investment in the respective processing<br />

and drying technologies, and different suppliers of raw materials. Investors in artificial<br />

drying technologies prefer to obtain their raw materials from larger, more commercially<br />

focused farmers, while processors using sun-dried cassava usually purchase surplus production<br />

from farmers’ associations (Sandifolo 2010a). Because artificially dried HQCF<br />

has a higher cost price and requires greater technical skills, it is expected that it cannot<br />

compete with traditional cassava flour on the staple food market (Sergeant 2009).<br />

Sun-dried HQCF is to be sold to buyers as close as possible to the village processing<br />

units. This means that both buyers and producers operate on the small-scale level,<br />

allowing for a good match between supply and demand. Also, both parties will be able<br />

to quickly interact if there are any quality, transport or payment issues. The sun-dried<br />

HQCF VC has been initiated in 2010 to produce a high-quality product acceptable<br />

to the bakers and is being scaled up over the next few years (Westby and Adebayo<br />

2010). Processors include farmer associations and small-scale, village-based entrepreneurs<br />

working with farmers. Table 3.1 presents the estimated targets and benefits for<br />

64