Section One

Section One

Section One

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

60<br />

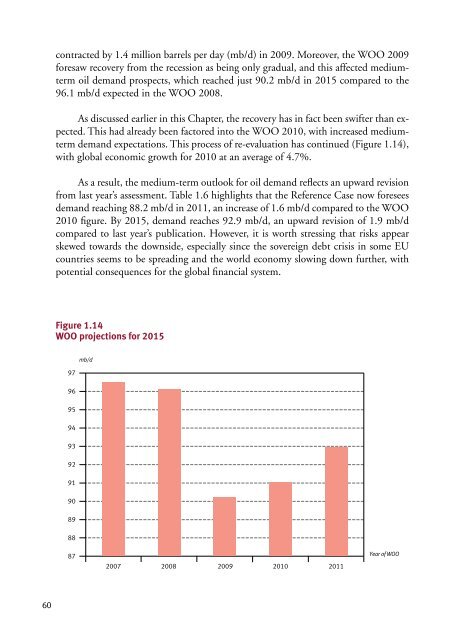

contracted by 1.4 million barrels per day (mb/d) in 2009. Moreover, the WOO 2009<br />

mboe/d<br />

foresaw recovery from the recession as being only gradual, and this affected medium-<br />

30<br />

term oil demand prospects, which reached just 90.2 mb/d OECD in 2015 compared to the<br />

96.1 mb/d expected in the WOO 2008.<br />

Developing countries<br />

25<br />

As discussed earlier in this Chapter, the recovery has in fact been swifter than expected.<br />

20 This had already been factored into the WOO 2010, with increased mediumterm<br />

demand expectations. This process of re-evaluation has continued (Figure 1.14),<br />

with global economic growth for 2010 at an average of 4.7%.<br />

15<br />

As a result, the medium-term outlook for oil demand reflects an upward revision<br />

from 10 last year’s assessment. Table 1.6 highlights that the Reference Case now foresees<br />

demand reaching 88.2 mb/d in 2011, an increase of 1.6 mb/d compared to the WOO<br />

2010 figure. By 2015, demand reaches 92.9 mb/d, an upward revision of 1.9 mb/d<br />

5<br />

compared to last year’s publication. However, it is worth stressing that risks appear<br />

skewed towards the downside, especially since the sovereign debt crisis in some EU<br />

countries 0 seems to be spreading and the world economy slowing down further, with<br />

1971 1990 2010 2035<br />

potential consequences for the global financial system.<br />

Figure 1.14<br />

WOO projections for 2015<br />

97<br />

96<br />

95<br />

94<br />

93<br />

92<br />

91<br />

90<br />

89<br />

88<br />

87<br />

mb/d<br />

Figure 1.13<br />

Figure 1.14<br />

2007 2008 2009 2010 2011<br />

Year of WOO