Section One

Section One

Section One

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

98<br />

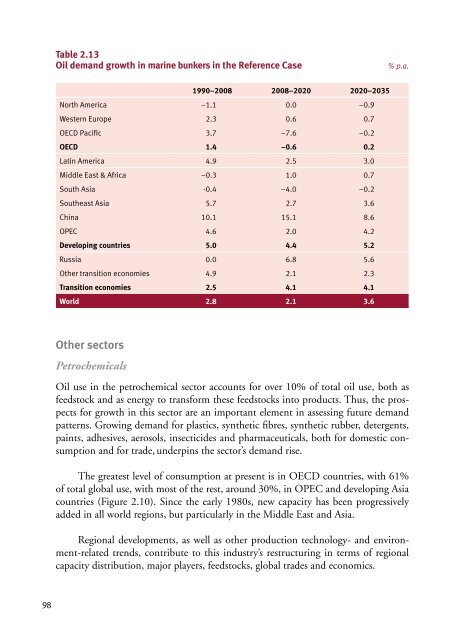

Table 2.13<br />

Oil demand growth in marine bunkers in the Reference Case % p.a.<br />

1990–2008 2008–2020 2020–2035<br />

North America –1.1 0.0 –0.9<br />

Western Europe 2.3 0.6 0.7<br />

OECD Pacific 3.7 –7.6 –0.2<br />

OECD 1.4 –0.6 0.2<br />

Latin America 4.9 2.5 3.0<br />

Middle East & Africa –0.3 1.0 0.7<br />

South Asia -0.4 –4.0 –0.2<br />

Southeast Asia 5.7 2.7 3.6<br />

China 10.1 15.1 8.6<br />

OPEC 4.6 2.0 4.2<br />

Developing countries 5.0 4.4 5.2<br />

Russia 0.0 6.8 5.6<br />

Other transition economies 4.9 2.1 2.3<br />

Transition economies 2.5 4.1 4.1<br />

World 2.8 2.1 3.6<br />

Other sectors<br />

Petrochemicals<br />

Oil use in the petrochemical sector accounts for over 10% of total oil use, both as<br />

feedstock and as energy to transform these feedstocks into products. Thus, the prospects<br />

for growth in this sector are an important element in assessing future demand<br />

patterns. Growing demand for plastics, synthetic fibres, synthetic rubber, detergents,<br />

paints, adhesives, aerosols, insecticides and pharmaceuticals, both for domestic consumption<br />

and for trade, underpins the sector’s demand rise.<br />

The greatest level of consumption at present is in OECD countries, with 61%<br />

of total global use, with most of the rest, around 30%, in OPEC and developing Asia<br />

countries (Figure 2.10). Since the early 1980s, new capacity has been progressively<br />

added in all world regions, but particularly in the Middle East and Asia.<br />

Regional developments, as well as other production technology- and environment-related<br />

trends, contribute to this industry’s restructuring in terms of regional<br />

capacity distribution, major players, feedstocks, global trades and economics.