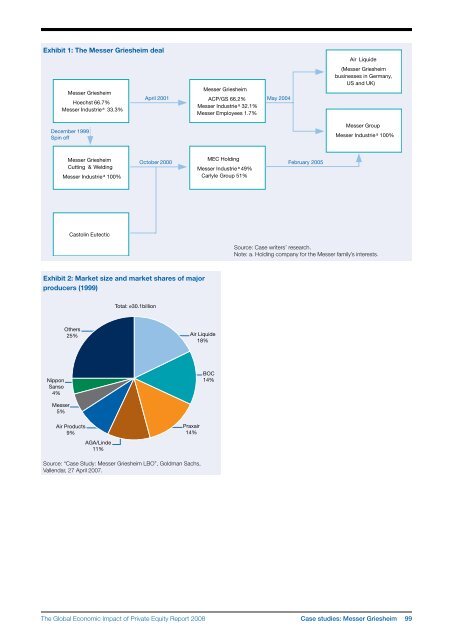

leveraged and in a difficult situation. Further, one‐third <strong>of</strong>an employee’s annual income was a huge investment formost managers – many were afraid to risk such a largesum. Messer Griesheim’s top management spent a greatdeal <strong>of</strong> time in one‐on‐one meetings with the managers toexplain the programme, and that its level <strong>of</strong> risk was in factless than imagined given the participation <strong>of</strong> the privateequity investors. In the end, about 85%–90% <strong>of</strong> MesserGriesheim managers participated, some investing a greatdeal <strong>of</strong> their money. One manager invested €1 million.Exit: empowerment <strong>of</strong> the family<strong>The</strong> exit agreement stipulated a window for a MesserGriesheim IPO for which agreement from all parties wasrequired up until 30 June 2003. Between 1 April 2003 and30 September 2003, the Messer family could exercise its calloption and buy back the Allianz Capital Partners/GoldmanSachs shares. As <strong>of</strong> 1 January 2004, the investors then hadthe right to pursue an IPO or sell their shares to the highestbidder. A “drag along” right existed that would also haveforced the family to sell their shares to the same bidder.It became clear that strategic buyers were willing to paystrategic premiums, and, therefore, an IPO was unlikely to<strong>of</strong>fer the same value potential as a trade sale. In the secondhalf <strong>of</strong> 2003, the pressure on the Messer family to exercisetheir call option increased and initial talks with potentialbuyers were initiated. <strong>The</strong> Messer family was not able to buyback the whole entity and, therefore, aimed at gaining controlat least over parts <strong>of</strong> the business. At first they hoped tokeep at least half <strong>of</strong> the German operations and additionalparts <strong>of</strong> the business from Allianz Capital Partners andGoldman Sachs while selling the rest <strong>of</strong> the company to astrategic buyer. Germany was the home country and seenas the heart <strong>of</strong> the company. S. Messer had proposed AirLiquide as a possible buyer; the investors had considereda public auction. However, as Goldman Sachs initiated theauction for half <strong>of</strong> the Messer Griesheim German concernsand additional businesses in the UK and the US, incomingbids were too low. Goldman Sachs advised that as the corebusiness the German concerns were the most attractivepart for any buyer, and the team realized they had to sellthe German operations in their entirety. A second auction,including the entire German business, was set up; againonly a few bids came in. In March 2004, with an additional€100 million added to their <strong>of</strong>fer, Air Liquide acquired MesserGriesheim’s German activities, as well as its US and UKconcerns, for €2.7 billion. <strong>The</strong> other parts <strong>of</strong> MesserGriesheim were bought back by the Messer family. Mostfelt Air Liquide did not overpay; the sales multiple wascomparable to other deals. Some felt a higher price mighthave been gained for the entire company, but this mighthave raised anti‐trust issues.<strong>The</strong> final exit was in May 2004. Messer Griesheim’s German,UK and US operations were sold to Air Liquide. <strong>The</strong> Messerfamily bought back the remaining interests in WesternEurope, Eastern Europe, China and Peru. <strong>The</strong> deal wasclosed after the end <strong>of</strong> the call window, however, asthe investors were able to see the company’s positivedevelopment and a successful exit seemed on the horizon;they therefore decided to extend the call period. S. Messerwas installed as CEO, and subsidiaries in Germany, UK andthe US were sold to Air Liquide. A holding company was setup, trading under the name Messer Group, encompassing allremaining subsidiaries in Europe, China and Peru (see Exhibit8). Schmieder joined the management board <strong>of</strong> Air Liquideafter the exit <strong>of</strong> Allianz Capital Partners/Goldman Sachs andS. Messer took over the position as CEO in the newlyfounded Messer Group.Coming full circle, in 2005, the Messer family purchased theoutstanding MEC Holding shares held by the Carlyle Group,acquiring all the shares in the company’s welding and cuttingdivision; in 2006, both businesses <strong>of</strong> the Messer Grouppassed the €1 billion sales mark and looked to expandactivities in Europe and Asia.Postscript: <strong>The</strong> Messer Griesheim deal – a loss leaderfor investors?<strong>The</strong> Messer Griesheim deal represents a unique casewhere the break‐up <strong>of</strong> a company was not motivated byinvestors, but rather was initiated by the family who sawthe opportunity to regain control over attractive parts <strong>of</strong>the business, albeit not the favoured German operations.For the investors, the strategy did not maximize their return;a higher return could probably have been realized by sellingthe company in its entirety to the highest bidder. By allowingthe Messer family to partly buy back their company, theinvestors gave away further return potential, since a strategicbuyer might have paid a higher price.<strong>The</strong>re were two rationales behind this: the Air Liquide dealwas highly pr<strong>of</strong>itable, so the investors were able to achieve ahigh return on that side <strong>of</strong> the deal (8x EBITDA exit multiple);and it enhanced the relationship <strong>of</strong> trust between the familyand investors. Goldman Sachs/Allianz Capital Partnersprovided the company with the required equity financing tobuy out Hoechst and they developed and maintained a goodrelationship with the family; Goldman Sachs/Allianz CapitalPartners enhanced this trust by helping the family regainpower over parts <strong>of</strong> Messer Griesheim businesses. Ratherthan emphasizing the effort to maximize returns, the regain<strong>of</strong> control over various parts <strong>of</strong> the Messer family’sbusinesses enhanced the good reputation <strong>of</strong> both GoldmanSachs and Allianz Capital Partners in the market – particularlyas the Air Liquide deal was already providing a high return.As a commentator in <strong>The</strong> Economist noted, “Goldman Sachsand Allianz Capital [Partners] would love it to be known, fromthis example, that although they might have made moremoney if they had found an industrial buyer [for the wholeentity], they can be fairy godmothers to family firms whomight be wary <strong>of</strong> using private equity.” 2222“Face value. <strong>Private</strong> equity and family fortunes”. <strong>The</strong> Economist, 10 July 2004.98 Case studies: Messer Griesheim<strong>The</strong> <strong>Global</strong> <strong>Economic</strong> <strong>Impact</strong> <strong>of</strong> <strong>Private</strong> <strong>Equity</strong> <strong>Report</strong> <strong>2008</strong>

Exhibit 1: <strong>The</strong> Messer Griesheim dealMesser GriesheimHoechst 66.7%Messer Industrie a 33.3%December 1999Spin <strong>of</strong>fMesser GriesheimApril 2001 ACP/GS 66.2% May 2004Messer Industrie a 32.1%Messer Employees 1.7%Air Liquide(Messer Griesheimbusinesses in Germany,US and UK)Messer GroupMesser Industrie a 100%Messer GriesheimCutting & WeldingMesser Industrie a 100%October 2000MEC HoldingMesser Industriea49%Carlyle Group 51%February 2005Castolin EutecticSource: Case writers’ research.Note: a. Holding company for the Messer family’s interests.Exhibit 2: Market size and market shares <strong>of</strong> majorproducers (1999)Total: e30.1billionOthers25%Air Liquide18%NipponSanso4%BOC14%Messer5%Air Products9%AGA/Linde11%Praxair14%Source: “Case Study: Messer Griesheim LBO”, Goldman Sachs,Vallendar, 27 April 2007.<strong>The</strong> <strong>Global</strong> <strong>Economic</strong> <strong>Impact</strong> <strong>of</strong> <strong>Private</strong> <strong>Equity</strong> <strong>Report</strong> <strong>2008</strong> Case studies: Messer Griesheim 99

- Page 2 and 3:

The Globalization of Alternative In

- Page 5:

ContributorsCo-editorsAnuradha Guru

- Page 9 and 10:

PrefaceKevin SteinbergChief Operati

- Page 11 and 12:

Letter on behalf of the Advisory Bo

- Page 13 and 14:

Executive summaryJosh lernerHarvard

- Page 15 and 16:

• Private equity-backed companies

- Page 17 and 18:

C. Indian casesThe two India cases,

- Page 19 and 20:

Part 1Large-sample studiesThe Globa

- Page 21 and 22:

The new demography of private equit

- Page 23 and 24:

among US publicly traded firms, it

- Page 25 and 26:

should be fairly complete. While th

- Page 27 and 28:

according to Moody’s (Hamilton et

- Page 29 and 30:

draining public markets of firms. I

- Page 31 and 32:

FIguresFigure 1A: LBO transactions

- Page 33 and 34:

TablesTable 1: Capital IQ 1980s cov

- Page 35 and 36:

Table 2: Magnitude and growth of LB

- Page 37 and 38:

Table 4: Exits of individual LBO tr

- Page 39 and 40:

Table 6: Determinants of exit succe

- Page 41 and 42:

Table 7: Ultimate staying power of

- Page 43 and 44:

Appendix 1: Imputed enterprise valu

- Page 45 and 46:

Private equity and long-run investm

- Page 47 and 48:

alternative names associated with t

- Page 49 and 50:

4. Finally, we explore whether firm

- Page 51 and 52:

When we estimate these regressions,

- Page 53 and 54:

cutting back on the number of filin

- Page 55 and 56:

Table 1: Summary statisticsPanel D:

- Page 57 and 58:

Table 4: Relative citation intensit

- Page 59 and 60:

figuresFigure 1: Number of private

- Page 61 and 62:

Private equity and employment*steve

- Page 63 and 64:

Especially when taken together, our

- Page 65 and 66: centred on the transaction year ide

- Page 67 and 68: and Vartia 1985.) Aggregate employm

- Page 69 and 70: sectors. In Retail Trade, the cumul

- Page 71 and 72: employment-weighted acquisition rat

- Page 73 and 74: FIguresFigure 1: Matches of private

- Page 75 and 76: Figure 6:Figure 6A: Comparison of n

- Page 77 and 78: Figure 8:Figure 8A: Comparison of j

- Page 79 and 80: Figure 11: Variation in impact in e

- Page 81 and 82: Figure 12: Differences in impact on

- Page 83 and 84: Private equity and corporate govern

- Page 85 and 86: et al (2007) track the evolution of

- Page 87 and 88: groups aim to improve firm performa

- Page 89 and 90: distribution of the LBO sponsors, m

- Page 91 and 92: the most difficult cases. This stor

- Page 93 and 94: to see whether these changes of CEO

- Page 95 and 96: Figure 3:This figure represents the

- Page 97 and 98: TablesTable 1: Company size descrip

- Page 99 and 100: Table 5: Changes in the board size,

- Page 101 and 102: Table 7: Board turnoverPanel A: Siz

- Page 103 and 104: Part 2Case studiesThe Global Econom

- Page 105 and 106: European private equity cases: intr

- Page 107 and 108: Exhibit 1: Private equity fund size

- Page 109 and 110: Messer Griesheimann-kristin achleit

- Page 111 and 112: ealized it was not possible to grow

- Page 113 and 114: The deal with Allianz Capital partn

- Page 115: the deal, the private equity invest

- Page 119 and 120: Exhibit 5: Post buyout structureMes

- Page 121 and 122: New Lookann-kristin achleitnerTechn

- Page 123 and 124: feet. This restricted store space w

- Page 125 and 126: institutional investors why this in

- Page 127 and 128: Although a public listing did not a

- Page 129 and 130: Exhibit 5: Employment development a

- Page 131 and 132: Chinese private equity cases: intro

- Page 133 and 134: Hony Capital and China Glass Holdin

- Page 135 and 136: Hony’s Chinese name means ambitio

- Page 137 and 138: Establishing early agreement on pos

- Page 139 and 140: Executing the IPOEach of the initia

- Page 141 and 142: Exhibit 1A: Summary of Hony Capital

- Page 143 and 144: Exhibit 4: Members of the China Gla

- Page 145 and 146: Exhibit 6A: China Glass post‐acqu

- Page 147 and 148: Exhibit 8: China Glass stock price

- Page 149 and 150: 3i Group plc and Little Sheep*Lily

- Page 151 and 152: y an aggressive franchise strategy,

- Page 153 and 154: soul” of the business. But there

- Page 155 and 156: Exhibit 1: Summary information on 3

- Page 157 and 158: Exhibit 6: An excerpt from the 180-

- Page 159 and 160: Indian private equity cases: introd

- Page 161 and 162: ICICI Venture and Subhiksha *Lily F

- Page 163 and 164: investment,” recalled Deshpande.

- Page 165 and 166: 2005 - 2007: Moderator, protector a

- Page 167 and 168:

Exhibit 3: Subhiksha’s board comp

- Page 169 and 170:

Warburg Pincus and Bharti Tele‐Ve

- Page 171 and 172:

founded two companies at this time

- Page 173 and 174:

By 2003 this restructuring task was

- Page 175 and 176:

Exhibit 1C: Private equity investme

- Page 177 and 178:

Exhibit 4B: Bharti cellular footpri

- Page 179 and 180:

Exhibit 6: Summary of Bharti’s fi

- Page 181 and 182:

Exhibit 7: Bharti’s board structu

- Page 183 and 184:

In the 1993‐94 academic year, he

- Page 185 and 186:

consumer products. She was also a R

- Page 187 and 188:

AcknowledgementsJosh LernerHarvard

- Page 189:

The World Economic Forum is an inde