- Page 2 and 3: The Globalization of Alternative In

- Page 5: ContributorsCo-editorsAnuradha Guru

- Page 9 and 10: PrefaceKevin SteinbergChief Operati

- Page 11 and 12: Letter on behalf of the Advisory Bo

- Page 13 and 14: Executive summaryJosh lernerHarvard

- Page 15 and 16: • Private equity-backed companies

- Page 17 and 18: C. Indian casesThe two India cases,

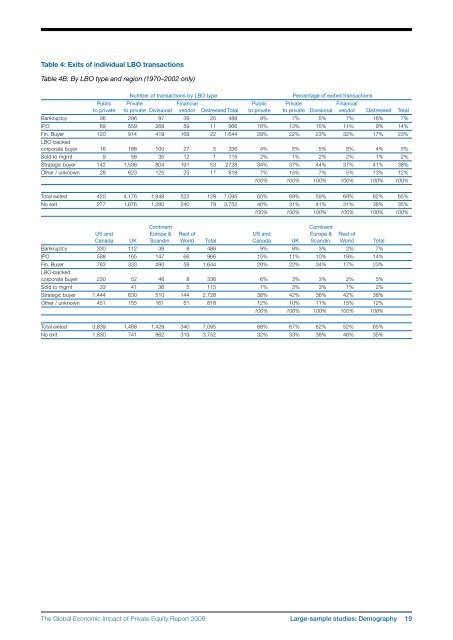

- Page 19 and 20: Part 1Large-sample studiesThe Globa

- Page 21 and 22: The new demography of private equit

- Page 23 and 24: among US publicly traded firms, it

- Page 25 and 26: should be fairly complete. While th

- Page 27 and 28: according to Moody’s (Hamilton et

- Page 29 and 30: draining public markets of firms. I

- Page 31 and 32: FIguresFigure 1A: LBO transactions

- Page 33 and 34: TablesTable 1: Capital IQ 1980s cov

- Page 35: Table 2: Magnitude and growth of LB

- Page 39 and 40: Table 6: Determinants of exit succe

- Page 41 and 42: Table 7: Ultimate staying power of

- Page 43 and 44: Appendix 1: Imputed enterprise valu

- Page 45 and 46: Private equity and long-run investm

- Page 47 and 48: alternative names associated with t

- Page 49 and 50: 4. Finally, we explore whether firm

- Page 51 and 52: When we estimate these regressions,

- Page 53 and 54: cutting back on the number of filin

- Page 55 and 56: Table 1: Summary statisticsPanel D:

- Page 57 and 58: Table 4: Relative citation intensit

- Page 59 and 60: figuresFigure 1: Number of private

- Page 61 and 62: Private equity and employment*steve

- Page 63 and 64: Especially when taken together, our

- Page 65 and 66: centred on the transaction year ide

- Page 67 and 68: and Vartia 1985.) Aggregate employm

- Page 69 and 70: sectors. In Retail Trade, the cumul

- Page 71 and 72: employment-weighted acquisition rat

- Page 73 and 74: FIguresFigure 1: Matches of private

- Page 75 and 76: Figure 6:Figure 6A: Comparison of n

- Page 77 and 78: Figure 8:Figure 8A: Comparison of j

- Page 79 and 80: Figure 11: Variation in impact in e

- Page 81 and 82: Figure 12: Differences in impact on

- Page 83 and 84: Private equity and corporate govern

- Page 85 and 86: et al (2007) track the evolution of

- Page 87 and 88:

groups aim to improve firm performa

- Page 89 and 90:

distribution of the LBO sponsors, m

- Page 91 and 92:

the most difficult cases. This stor

- Page 93 and 94:

to see whether these changes of CEO

- Page 95 and 96:

Figure 3:This figure represents the

- Page 97 and 98:

TablesTable 1: Company size descrip

- Page 99 and 100:

Table 5: Changes in the board size,

- Page 101 and 102:

Table 7: Board turnoverPanel A: Siz

- Page 103 and 104:

Part 2Case studiesThe Global Econom

- Page 105 and 106:

European private equity cases: intr

- Page 107 and 108:

Exhibit 1: Private equity fund size

- Page 109 and 110:

Messer Griesheimann-kristin achleit

- Page 111 and 112:

ealized it was not possible to grow

- Page 113 and 114:

The deal with Allianz Capital partn

- Page 115 and 116:

the deal, the private equity invest

- Page 117 and 118:

Exhibit 1: The Messer Griesheim dea

- Page 119 and 120:

Exhibit 5: Post buyout structureMes

- Page 121 and 122:

New Lookann-kristin achleitnerTechn

- Page 123 and 124:

feet. This restricted store space w

- Page 125 and 126:

institutional investors why this in

- Page 127 and 128:

Although a public listing did not a

- Page 129 and 130:

Exhibit 5: Employment development a

- Page 131 and 132:

Chinese private equity cases: intro

- Page 133 and 134:

Hony Capital and China Glass Holdin

- Page 135 and 136:

Hony’s Chinese name means ambitio

- Page 137 and 138:

Establishing early agreement on pos

- Page 139 and 140:

Executing the IPOEach of the initia

- Page 141 and 142:

Exhibit 1A: Summary of Hony Capital

- Page 143 and 144:

Exhibit 4: Members of the China Gla

- Page 145 and 146:

Exhibit 6A: China Glass post‐acqu

- Page 147 and 148:

Exhibit 8: China Glass stock price

- Page 149 and 150:

3i Group plc and Little Sheep*Lily

- Page 151 and 152:

y an aggressive franchise strategy,

- Page 153 and 154:

soul” of the business. But there

- Page 155 and 156:

Exhibit 1: Summary information on 3

- Page 157 and 158:

Exhibit 6: An excerpt from the 180-

- Page 159 and 160:

Indian private equity cases: introd

- Page 161 and 162:

ICICI Venture and Subhiksha *Lily F

- Page 163 and 164:

investment,” recalled Deshpande.

- Page 165 and 166:

2005 - 2007: Moderator, protector a

- Page 167 and 168:

Exhibit 3: Subhiksha’s board comp

- Page 169 and 170:

Warburg Pincus and Bharti Tele‐Ve

- Page 171 and 172:

founded two companies at this time

- Page 173 and 174:

By 2003 this restructuring task was

- Page 175 and 176:

Exhibit 1C: Private equity investme

- Page 177 and 178:

Exhibit 4B: Bharti cellular footpri

- Page 179 and 180:

Exhibit 6: Summary of Bharti’s fi

- Page 181 and 182:

Exhibit 7: Bharti’s board structu

- Page 183 and 184:

In the 1993‐94 academic year, he

- Page 185 and 186:

consumer products. She was also a R

- Page 187 and 188:

AcknowledgementsJosh LernerHarvard

- Page 189:

The World Economic Forum is an inde