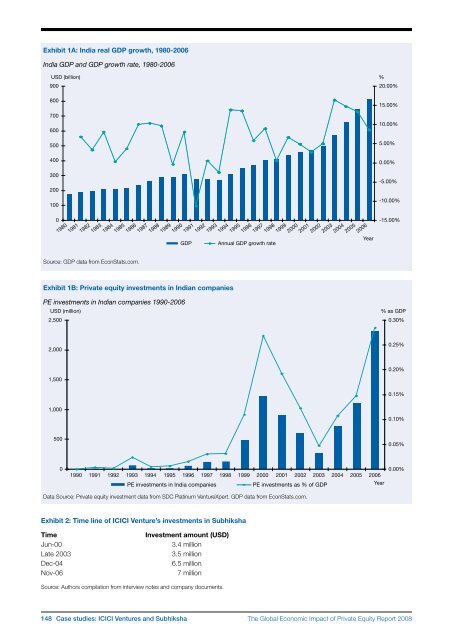

Exhibit 1A: India real GDP growth, 1980-2006India GDP and GDP growth rate, 1980-2006USD (billion) %90020.00%80015.00%70060010.00%5005.00%4000.00%3002001000Source: GDP data from EconStats.com.198019811982198319841985198619871988198919901991GDP199219931994Exhibit 1B: <strong>Private</strong> equity investments in Indian companies1995Annual GDP growth rate19961997199819992000200120022003200420052006Year-5.00%-10.00%-15.00%PE investments in Indian companies 1990-2006USD (million)% as GDP2,5000.30%2,0000.25%0.20%1,5000.15%1,0000.10%5000.05%01990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006PE investments in India companies PE investments as % <strong>of</strong> GDP Year0.00%Data Source: <strong>Private</strong> equity investment data from SDC Platinum VentureXpert. GDP data from EconStats.com.Exhibit 2: Time line <strong>of</strong> ICICI Venture’s investments in SubhikshaTimeJun-00Late 2003Dec-04Nov-06Investment amount (USD)3.4 million3.5 million6.5 million7 millionSource: Authors compilation from interview notes and company documents.148 Case studies: ICICI Ventures and Subhiksha<strong>The</strong> <strong>Global</strong> <strong>Economic</strong> <strong>Impact</strong> <strong>of</strong> <strong>Private</strong> <strong>Equity</strong> <strong>Report</strong> <strong>2008</strong>

Exhibit 3: Subhiksha’s board composition andbrief biographiesBoard Chairman: S B Mathur, age 52, an Indian national,is the Chairman and an independent director <strong>of</strong> ourcompany. He is a fellow <strong>of</strong> the Institute <strong>of</strong> CharteredAccountants <strong>of</strong> India and the Institute <strong>of</strong> Cost Accountants<strong>of</strong> India. He has worked with the Life Insurance Corporation<strong>of</strong> India from 1967 to 2004, when he retired as its chairman.During his tenure at the Life Insurance Corporation <strong>of</strong> India,he has held several positions, including those <strong>of</strong> the seniordivisional manager, Gwalior division, chief <strong>of</strong> corporateplanning, general manager <strong>of</strong> LIC (International) EC, zonalmanager for the western zone and the executive director.Managing Director: R Subramanian, age 41, an Indiannational, is the Managing Director <strong>of</strong> our company.Subramanian is a founder director <strong>of</strong> our company. Heholds a master’s in Engineering from the Indian Institute<strong>of</strong> Technology, Madras and a Post Graduate Diplomain Business Administration from the Indian Institute<strong>of</strong> Management, Ahmedabad. He was a gold medalistat the Indian Institute <strong>of</strong> Management, Ahmedabad.Director: Bala Deshpande, age 41, an Indian national,has been nominated to our board by ICICI Venture FundsManagement Company Limited. She holds a Master’s in<strong>Economic</strong>s from Bombay University and a Master’s inManagement Studies from the Jamnalal Bajaj Institute <strong>of</strong>Management Studies. Bala Deshpande has over 17 years <strong>of</strong>work experience, including seven years in the private equityfield. Prior to ICICI Venture Funds Management CompanyLimited, she has had multi‐industry exposure and hasworked with leading multinational companies, includingBest Foods, Cadburys and ICI. She was part <strong>of</strong> the strategicplanning team at Best Foods and was nominated for theWomen Leadership Forum held at Best Foods, New York.Apart from the company, Deshpande is on the board <strong>of</strong>directors <strong>of</strong> several companies, including Air Deccan Limited,Nagarjuna Constructions, Welspun, TechProcess Solutionsand Naukri.com. She currently focuses on sectors such asretail, media, IT, ITES, telecoms and construction as well assome manufacturing-related industries.Director: Renuka Ramnath, age 45, an Indian national,has been nominated to our Board by ICICI Venture FundsManagement Company Limited. She holds a bachelor’s inEngineering and a Master’s in Business Administration(Finance) from Bombay University. She is the managingdirector and chief executive <strong>of</strong>ficer <strong>of</strong> ICICI Venture FundsManagement Company Limited, a wholly‐owned subsidiary<strong>of</strong> ICICI Bank Limited. Renuka Ramnath has over 21 years <strong>of</strong>work experience with the ICICI Bank Group. She has workedwith the merchant banking division <strong>of</strong> the group and headedthe corporate finance and equities businesses at ICICISecurities Limited. She moved back to ICICI in 1997 toset up the structured finance business. She has alsobeen involved in setting up the e‐commerce initiatives forthe ICICI Bank Group. Ramnath has featured in the Top25 Most Powerful Women in Indian Business list publishedby Business Today and in the list <strong>of</strong> India’s Most PowerfulCEOs published by the <strong>Economic</strong> Times.Director: Rama Bijapurkar, age 50, an Indian national, is anindependent director <strong>of</strong> the company. Bijapurkar holds a PostGraduate Diploma in Business Administration from the IndianInstitute <strong>of</strong> Management, Ahmedabad. Presently, she teachesas a visiting pr<strong>of</strong>essor and serves on the board <strong>of</strong> governors<strong>of</strong> the Indian Institute <strong>of</strong> Management, Ahmedabad. She alsohas a market strategy consulting practice and works withIndian and global companies to develop their business‐marketstrategies. She serves as an independent director on theboards <strong>of</strong> several Indian companies. Bijapurkar has over30 years <strong>of</strong> work experience, including at McKinsey &Company, MARG (now AC Nielsen India). She has beena full‐time consultant with Hindustan Lever Limited. She haspublications on market and consumer‐related issues bothwithin and outside India and writes columns for the <strong>Economic</strong>Times and Business <strong>World</strong>.Director: Kannan Srinivasan, is an independent director<strong>of</strong> the company. Srinivasan is HJ Heinz II Pr<strong>of</strong>essor <strong>of</strong>Management, Marketing and Information Systems atCarnegie Mellon University. He earned his undergraduatedegree in Engineering (1978) and Post‐Graduate Diplomain Management (1980) from India. Prior to earning hisPhD (1986) at the University <strong>of</strong> California at Los Angeles,Srinivasan worked as a product manager at Procter &Gamble (India). He has published over 50 papers in leadingbusiness and statistics academic journals and shoulderseditorial responsibilities <strong>of</strong> several top‐tier journals. Srinivasanhas been nominated several times for the Leland BachTeaching Award. He has also taught at the graduateschools <strong>of</strong> business at <strong>The</strong> University <strong>of</strong> Chicago andStanford University. He has worked on numerous consultingprojects and executive teaching engagements with firmssuch as General Motors, Asea‐Brown Boveri, Kodak,Chrysler, Fujitsu, IBM, Calgon Carbon, CIBA Vision, KraftFoods, IKEA, Management Science Associates, McKinsey&Co., Pricewaterhouse Coopers, United Technologiesand Wipro. Recently, he has worked with multinationalsin the US to develop their India strategy. He is also thedirector <strong>of</strong> the Center for E‐Business Innovation (eBI) atCarnegie Mellon University.Source: Company documents.<strong>The</strong> <strong>Global</strong> <strong>Economic</strong> <strong>Impact</strong> <strong>of</strong> <strong>Private</strong> <strong>Equity</strong> <strong>Report</strong> <strong>2008</strong> Case studies: ICICI Ventures and Subhiksha 149

- Page 2 and 3:

The Globalization of Alternative In

- Page 5:

ContributorsCo-editorsAnuradha Guru

- Page 9 and 10:

PrefaceKevin SteinbergChief Operati

- Page 11 and 12:

Letter on behalf of the Advisory Bo

- Page 13 and 14:

Executive summaryJosh lernerHarvard

- Page 15 and 16:

• Private equity-backed companies

- Page 17 and 18:

C. Indian casesThe two India cases,

- Page 19 and 20:

Part 1Large-sample studiesThe Globa

- Page 21 and 22:

The new demography of private equit

- Page 23 and 24:

among US publicly traded firms, it

- Page 25 and 26:

should be fairly complete. While th

- Page 27 and 28:

according to Moody’s (Hamilton et

- Page 29 and 30:

draining public markets of firms. I

- Page 31 and 32:

FIguresFigure 1A: LBO transactions

- Page 33 and 34:

TablesTable 1: Capital IQ 1980s cov

- Page 35 and 36:

Table 2: Magnitude and growth of LB

- Page 37 and 38:

Table 4: Exits of individual LBO tr

- Page 39 and 40:

Table 6: Determinants of exit succe

- Page 41 and 42:

Table 7: Ultimate staying power of

- Page 43 and 44:

Appendix 1: Imputed enterprise valu

- Page 45 and 46:

Private equity and long-run investm

- Page 47 and 48:

alternative names associated with t

- Page 49 and 50:

4. Finally, we explore whether firm

- Page 51 and 52:

When we estimate these regressions,

- Page 53 and 54:

cutting back on the number of filin

- Page 55 and 56:

Table 1: Summary statisticsPanel D:

- Page 57 and 58:

Table 4: Relative citation intensit

- Page 59 and 60:

figuresFigure 1: Number of private

- Page 61 and 62:

Private equity and employment*steve

- Page 63 and 64:

Especially when taken together, our

- Page 65 and 66:

centred on the transaction year ide

- Page 67 and 68:

and Vartia 1985.) Aggregate employm

- Page 69 and 70:

sectors. In Retail Trade, the cumul

- Page 71 and 72:

employment-weighted acquisition rat

- Page 73 and 74:

FIguresFigure 1: Matches of private

- Page 75 and 76:

Figure 6:Figure 6A: Comparison of n

- Page 77 and 78:

Figure 8:Figure 8A: Comparison of j

- Page 79 and 80:

Figure 11: Variation in impact in e

- Page 81 and 82:

Figure 12: Differences in impact on

- Page 83 and 84:

Private equity and corporate govern

- Page 85 and 86:

et al (2007) track the evolution of

- Page 87 and 88:

groups aim to improve firm performa

- Page 89 and 90:

distribution of the LBO sponsors, m

- Page 91 and 92:

the most difficult cases. This stor

- Page 93 and 94:

to see whether these changes of CEO

- Page 95 and 96:

Figure 3:This figure represents the

- Page 97 and 98:

TablesTable 1: Company size descrip

- Page 99 and 100:

Table 5: Changes in the board size,

- Page 101 and 102:

Table 7: Board turnoverPanel A: Siz

- Page 103 and 104:

Part 2Case studiesThe Global Econom

- Page 105 and 106:

European private equity cases: intr

- Page 107 and 108:

Exhibit 1: Private equity fund size

- Page 109 and 110:

Messer Griesheimann-kristin achleit

- Page 111 and 112:

ealized it was not possible to grow

- Page 113 and 114:

The deal with Allianz Capital partn

- Page 115 and 116: the deal, the private equity invest

- Page 117 and 118: Exhibit 1: The Messer Griesheim dea

- Page 119 and 120: Exhibit 5: Post buyout structureMes

- Page 121 and 122: New Lookann-kristin achleitnerTechn

- Page 123 and 124: feet. This restricted store space w

- Page 125 and 126: institutional investors why this in

- Page 127 and 128: Although a public listing did not a

- Page 129 and 130: Exhibit 5: Employment development a

- Page 131 and 132: Chinese private equity cases: intro

- Page 133 and 134: Hony Capital and China Glass Holdin

- Page 135 and 136: Hony’s Chinese name means ambitio

- Page 137 and 138: Establishing early agreement on pos

- Page 139 and 140: Executing the IPOEach of the initia

- Page 141 and 142: Exhibit 1A: Summary of Hony Capital

- Page 143 and 144: Exhibit 4: Members of the China Gla

- Page 145 and 146: Exhibit 6A: China Glass post‐acqu

- Page 147 and 148: Exhibit 8: China Glass stock price

- Page 149 and 150: 3i Group plc and Little Sheep*Lily

- Page 151 and 152: y an aggressive franchise strategy,

- Page 153 and 154: soul” of the business. But there

- Page 155 and 156: Exhibit 1: Summary information on 3

- Page 157 and 158: Exhibit 6: An excerpt from the 180-

- Page 159 and 160: Indian private equity cases: introd

- Page 161 and 162: ICICI Venture and Subhiksha *Lily F

- Page 163 and 164: investment,” recalled Deshpande.

- Page 165: 2005 - 2007: Moderator, protector a

- Page 169 and 170: Warburg Pincus and Bharti Tele‐Ve

- Page 171 and 172: founded two companies at this time

- Page 173 and 174: By 2003 this restructuring task was

- Page 175 and 176: Exhibit 1C: Private equity investme

- Page 177 and 178: Exhibit 4B: Bharti cellular footpri

- Page 179 and 180: Exhibit 6: Summary of Bharti’s fi

- Page 181 and 182: Exhibit 7: Bharti’s board structu

- Page 183 and 184: In the 1993‐94 academic year, he

- Page 185 and 186: consumer products. She was also a R

- Page 187 and 188: AcknowledgementsJosh LernerHarvard

- Page 189: The World Economic Forum is an inde