In little more than a year this new proactive strategytransformed the pr<strong>of</strong>ile <strong>of</strong> Little Sheep’s franchise system.<strong>The</strong> company moved from having 40 directly owned storesversus over 500 franchises before the 3i investment to amore balanced mix <strong>of</strong> 101 to 260 by late 2007. Even with adramatically decreased total store count, these fundamentalchanges resulted in year‐on‐year revenue growth <strong>of</strong> closeto 40%, double the industry average <strong>of</strong> about 20%.Shelving the international expansion planPrior to 3i’s investment, Little Sheep had an ambitious planfor international expansion. With successful restaurantsalready operating in Toronto and Hong Kong, managementwas eager to accelerate the pace <strong>of</strong> overseas growth andestablish the Little Sheep brand name globally. Each regionalVP was designated to lead expansion efforts in differentoverseas regions – North America, North Asia and SouthEast Asia – even though they were already stretched thinmanaging their domestic operations.Little Sheep’s overseas ambitions were quite commonamong the new generation <strong>of</strong> Chinese private enterprises.On this issue, however, 3i and Little Sheep management haddifferent views. Even though 3i was well placed to provideintroductions and on‐the‐ground support for an overseasexpansion, it strongly recommended that Little Sheep initiallyfocus on strengthening domestic operations rather thanrushing into overseas expansion. “Given the vast and yetuntapped opportunities in China’s restaurant industry, it isstrategically important for Little Sheep to leverage the leadingmarket share and brand name it has already established tosecure a dominant market position at home beforeexpanding its operations overseas,” Cheung explained.ConclusionsAt first glance the pairing <strong>of</strong> 3i, a global private equity groupwith almost no track record in China, and a restaurant chainwith origins in remote Mongolia, might seem like an odd andunlikely match. But the story <strong>of</strong> their relationship conforms tomany <strong>of</strong> the fundamental characteristics <strong>of</strong> successful privateequity transactions, especially in emerging markets. First, theinitial driver that allowed 3i to win the mandate after an intensecontest with better‐known competitors was chemistry, or theability to make the founder comfortable with its industryexpertise, commitment to the company and approach topost‐investment value-creation. Money was secondary.Second, Little Sheep’s founder had the foresight and selfconfidenceto recognize the value <strong>of</strong> accepting an activeinvestor into his company. Even though he had never heard<strong>of</strong> 3i before meeting Daizong Wang, he and his seniormanagement team exhibited an openness and eagerness tolearn from outsiders, which is not always the case, especiallywith closely held family‐run firms in emerging market countries.And third, this is a textbook case <strong>of</strong> the positive results thatstem from closely aligned interests between a private equityinvestor and the management <strong>of</strong> a portfolio company. Fromthe beginning, the 3i team was exceptionally hands‐on,working closely with the company’s senior management teamon a continuous basis to make significant changes in thecompany, always with an eye to building value and movingcloser to the day when Little Sheep would be positioned tosuccessfully execute an IPO. <strong>The</strong> combination <strong>of</strong> these threefactors goes far to explain the ingredients required forsuccessful private equity transactions in emerging markets,or anywhere.Although management initially resisted this 3i recommendation,Zhang later conceded that this was a sensible approach.Looking back on the incident, one <strong>of</strong> the independent directorsviewed the outcome as one more example <strong>of</strong> the company’sfundamental strength: “<strong>The</strong>y [Little Sheep management] areopen‐minded, and very willing to listen,” remarked Yuka Yeung,“which is really remarkable. It is a learning company.”Early resultsFrom the time <strong>of</strong> 3i’s investment in mid‐2006 until the end<strong>of</strong> 2007, Little Sheep opened 37 new stores and achievedyear‐on‐year revenue growth <strong>of</strong> 40%, far in excess <strong>of</strong> the15%‐20% average growth in China’s food sector. <strong>The</strong> strongrevenue growth was also fueled by the evolution <strong>of</strong> LittleSheep from a pure restaurant business into a more diversifiedfood and beverages group with two meat processingfacilities, a packaged‐seasoning plant, a logistics companyand a number <strong>of</strong> regional subsidiary companies. <strong>The</strong>company also completed its search for new senior executivetalent: Daizong Wang validated his confidence in Little Sheepby resigning from 3i in October 2007 to become LittleSheep’s new CFO, and Yuka Yeung, one <strong>of</strong> the independentdirectors and the former CEO <strong>of</strong> KFC’s Hong Kong franchise,became the new COO.136 Case studies: 3i Group plc and Little Sheep<strong>The</strong> <strong>Global</strong> <strong>Economic</strong> <strong>Impact</strong> <strong>of</strong> <strong>Private</strong> <strong>Equity</strong> <strong>Report</strong> <strong>2008</strong>

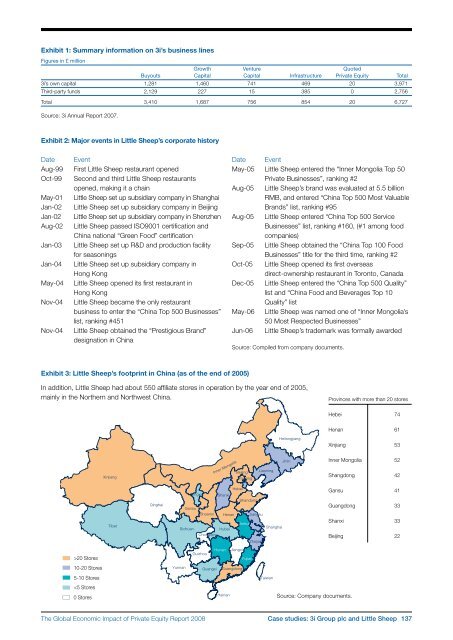

Exhibit 1: Summary information on 3i’s business linesFigures in £ millionGrowth Venture QuotedBuyouts Capital Capital Infrastructure <strong>Private</strong> <strong>Equity</strong> Total3i’s own capital 1,281 1,460 741 469 20 3,971Third‐party funds 2,129 227 15 385 0 2,756Total 3,410 1,687 756 854 20 6,727Source: 3i Annual <strong>Report</strong> 2007.Exhibit 2: Major events in Little Sheep’s corporate historyDateAug-99Oct-99May-01Jan-02Jan-02Aug-02Jan-03Jan-04May-04Nov-04Nov-04EventFirst Little Sheep restaurant openedSecond and third Little Sheep restaurantsopened, making it a chainLittle Sheep set up subsidiary company in ShanghaiLittle Sheep set up subsidiary company in BeijingLittle Sheep set up subsidiary company in ShenzhenLittle Sheep passed ISO9001 certification andChina national “Green Food” certificationLittle Sheep set up R&D and production facilityfor seasoningsLittle Sheep set up subsidiary company inHong KongLittle Sheep opened its first restaurant inHong KongLittle Sheep became the only restaurantbusiness to enter the “China Top 500 Businesses”list, ranking #451Little Sheep obtained the “Prestigious Brand”designation in ChinaDate EventMay-05 Little Sheep entered the “Inner Mongolia Top 50<strong>Private</strong> Businesses”, ranking #2Aug-05 Little Sheep’s brand was evaluated at 5.5 billionRMB, and entered “China Top 500 Most ValuableBrands” list, ranking #95Aug-05 Little Sheep entered “China Top 500 ServiceBusinesses” list, ranking #160, (#1 among foodcompanies)Sep-05 Little Sheep obtained the “China Top 100 FoodBusinesses” title for the third time, ranking #2Oct-05 Little Sheep opened its first overseasdirect‐ownership restaurant in Toronto, CanadaDec-05 Little Sheep entered the “China Top 500 Quality”list and “China Food and Beverages Top 10Quality” listMay-06 Little Sheep was named one <strong>of</strong> “Inner Mongolia’s50 Most Respected Businesses”Jun-06 Little Sheep’s trademark was formally awardedSource: Compiled from company documents.Exhibit 3: Little Sheep’s footprint in China (as <strong>of</strong> the end <strong>of</strong> 2005)In addition, Little Sheep had about 550 affiliate stores in operation by the year end <strong>of</strong> 2005,mainly in the Northern and Northwest China.Provinces with more than 20 storesHebei 74Henan 61HeilongjiangXinjiang 53XinjiangInner MongoliaBeijingTianjingLiaoningJininInner Mongolia 52Shangdong 42TibetQinghaiHebeiNingxia ShanxiShandongGansuShaanxi Henan JiangsuAnhuiSichuanHubeiChongqingZhejianShanghaiGansu 41Guangdong 33Shanxi 33Beijing 22>20 StoresGuizhouHunanJiangxiFujian10-20 StoresYunnanGuangxiGuangdong5-10 StoresTaiwan

- Page 2 and 3:

The Globalization of Alternative In

- Page 5:

ContributorsCo-editorsAnuradha Guru

- Page 9 and 10:

PrefaceKevin SteinbergChief Operati

- Page 11 and 12:

Letter on behalf of the Advisory Bo

- Page 13 and 14:

Executive summaryJosh lernerHarvard

- Page 15 and 16:

• Private equity-backed companies

- Page 17 and 18:

C. Indian casesThe two India cases,

- Page 19 and 20:

Part 1Large-sample studiesThe Globa

- Page 21 and 22:

The new demography of private equit

- Page 23 and 24:

among US publicly traded firms, it

- Page 25 and 26:

should be fairly complete. While th

- Page 27 and 28:

according to Moody’s (Hamilton et

- Page 29 and 30:

draining public markets of firms. I

- Page 31 and 32:

FIguresFigure 1A: LBO transactions

- Page 33 and 34:

TablesTable 1: Capital IQ 1980s cov

- Page 35 and 36:

Table 2: Magnitude and growth of LB

- Page 37 and 38:

Table 4: Exits of individual LBO tr

- Page 39 and 40:

Table 6: Determinants of exit succe

- Page 41 and 42:

Table 7: Ultimate staying power of

- Page 43 and 44:

Appendix 1: Imputed enterprise valu

- Page 45 and 46:

Private equity and long-run investm

- Page 47 and 48:

alternative names associated with t

- Page 49 and 50:

4. Finally, we explore whether firm

- Page 51 and 52:

When we estimate these regressions,

- Page 53 and 54:

cutting back on the number of filin

- Page 55 and 56:

Table 1: Summary statisticsPanel D:

- Page 57 and 58:

Table 4: Relative citation intensit

- Page 59 and 60:

figuresFigure 1: Number of private

- Page 61 and 62:

Private equity and employment*steve

- Page 63 and 64:

Especially when taken together, our

- Page 65 and 66:

centred on the transaction year ide

- Page 67 and 68:

and Vartia 1985.) Aggregate employm

- Page 69 and 70:

sectors. In Retail Trade, the cumul

- Page 71 and 72:

employment-weighted acquisition rat

- Page 73 and 74:

FIguresFigure 1: Matches of private

- Page 75 and 76:

Figure 6:Figure 6A: Comparison of n

- Page 77 and 78:

Figure 8:Figure 8A: Comparison of j

- Page 79 and 80:

Figure 11: Variation in impact in e

- Page 81 and 82:

Figure 12: Differences in impact on

- Page 83 and 84:

Private equity and corporate govern

- Page 85 and 86:

et al (2007) track the evolution of

- Page 87 and 88:

groups aim to improve firm performa

- Page 89 and 90:

distribution of the LBO sponsors, m

- Page 91 and 92:

the most difficult cases. This stor

- Page 93 and 94:

to see whether these changes of CEO

- Page 95 and 96:

Figure 3:This figure represents the

- Page 97 and 98:

TablesTable 1: Company size descrip

- Page 99 and 100:

Table 5: Changes in the board size,

- Page 101 and 102:

Table 7: Board turnoverPanel A: Siz

- Page 103 and 104: Part 2Case studiesThe Global Econom

- Page 105 and 106: European private equity cases: intr

- Page 107 and 108: Exhibit 1: Private equity fund size

- Page 109 and 110: Messer Griesheimann-kristin achleit

- Page 111 and 112: ealized it was not possible to grow

- Page 113 and 114: The deal with Allianz Capital partn

- Page 115 and 116: the deal, the private equity invest

- Page 117 and 118: Exhibit 1: The Messer Griesheim dea

- Page 119 and 120: Exhibit 5: Post buyout structureMes

- Page 121 and 122: New Lookann-kristin achleitnerTechn

- Page 123 and 124: feet. This restricted store space w

- Page 125 and 126: institutional investors why this in

- Page 127 and 128: Although a public listing did not a

- Page 129 and 130: Exhibit 5: Employment development a

- Page 131 and 132: Chinese private equity cases: intro

- Page 133 and 134: Hony Capital and China Glass Holdin

- Page 135 and 136: Hony’s Chinese name means ambitio

- Page 137 and 138: Establishing early agreement on pos

- Page 139 and 140: Executing the IPOEach of the initia

- Page 141 and 142: Exhibit 1A: Summary of Hony Capital

- Page 143 and 144: Exhibit 4: Members of the China Gla

- Page 145 and 146: Exhibit 6A: China Glass post‐acqu

- Page 147 and 148: Exhibit 8: China Glass stock price

- Page 149 and 150: 3i Group plc and Little Sheep*Lily

- Page 151 and 152: y an aggressive franchise strategy,

- Page 153: soul” of the business. But there

- Page 157 and 158: Exhibit 6: An excerpt from the 180-

- Page 159 and 160: Indian private equity cases: introd

- Page 161 and 162: ICICI Venture and Subhiksha *Lily F

- Page 163 and 164: investment,” recalled Deshpande.

- Page 165 and 166: 2005 - 2007: Moderator, protector a

- Page 167 and 168: Exhibit 3: Subhiksha’s board comp

- Page 169 and 170: Warburg Pincus and Bharti Tele‐Ve

- Page 171 and 172: founded two companies at this time

- Page 173 and 174: By 2003 this restructuring task was

- Page 175 and 176: Exhibit 1C: Private equity investme

- Page 177 and 178: Exhibit 4B: Bharti cellular footpri

- Page 179 and 180: Exhibit 6: Summary of Bharti’s fi

- Page 181 and 182: Exhibit 7: Bharti’s board structu

- Page 183 and 184: In the 1993‐94 academic year, he

- Page 185 and 186: consumer products. She was also a R

- Page 187 and 188: AcknowledgementsJosh LernerHarvard

- Page 189: The World Economic Forum is an inde