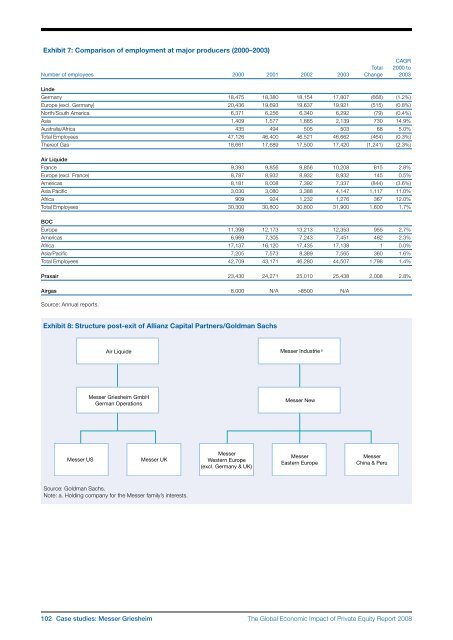

Exhibit 7: Comparison <strong>of</strong> employment at major producers (2000–2003)CAGRTotal 2000 toNumber <strong>of</strong> employees 2000 2001 2002 2003 Change 2003LindeGermany 18,475 18,380 18,154 17,807 (668) (1.2%)Europe (excl. Germany) 20,436 19,693 19,637 19,921 (515) (0.8%)North/South America 6,371 6,256 6,340 6,292 (79) (0.4%)Asia 1,409 1,577 1,885 2,139 730 14.9%Australia/Africa 435 494 505 503 68 5.0%Total Employees 47,126 46,400 46,521 46,662 (464) (0.3%)<strong>The</strong>re<strong>of</strong> Gas 18,661 17,689 17,500 17,420 (1,241) (2.3%)Air LiquideFrance 9,393 9,856 9,856 10,208 815 2.8%Europe (excl. France) 8,787 8,932 8,932 8,932 145 0.5%Americas 8,181 8,008 7,392 7,337 (844) (3.6%)Asia Pacific 3,030 3,080 3,388 4,147 1,117 11.0%Africa 909 924 1,232 1,276 367 12.0%Total Employees 30,300 30,800 30,800 31,900 1,600 1.7%BOCEurope 11,398 12,173 13,213 12,353 955 2.7%Americas 6,969 7,305 7,243 7,451 482 2.3%Africa 17,137 16,120 17,435 17,138 1 0.0%Asia/Pacific 7,205 7,573 8,389 7,565 360 1.6%Total Employees 42,709 43,171 46,280 44,507 1,798 1.4%Praxair 23,430 24,271 25,010 25,438 2,008 2.8%Airgas 8,000 N/A >8500 N/ASource: Annual reports.Exhibit 8: Structure post-exit <strong>of</strong> Allianz Capital Partners/Goldman SachsAir LiquideMesser Industrie aMesser Griesheim GmbHGerman OperationsMesser NewMesser USMesser UKMesserWestern Europe(excl. Germany & UK)MesserEastern EuropeMesserChina & PeruSource: Goldman Sachs.Note: a. Holding company for the Messer family’s interests.102 Case studies: Messer Griesheim<strong>The</strong> <strong>Global</strong> <strong>Economic</strong> <strong>Impact</strong> <strong>of</strong> <strong>Private</strong> <strong>Equity</strong> <strong>Report</strong> <strong>2008</strong>

New Lookann-kristin achleitnerTechnische Universität Müncheneva nathusiusTechnische Universität MünchenKerry hermanHarvard Business Schooljosh lernerHarvard Business SchoolExecutive SummaryIn July 2003, UK fashion retailer New Look was taken privatewith the support <strong>of</strong> Apax Partners/Permira. <strong>The</strong> management<strong>of</strong> New Look, originally listed publicly in 1998, wanted totransform the company to improve performance and takeadvantage <strong>of</strong> several opportunities they believed the UK andEuropean retail sector <strong>of</strong>fered. <strong>The</strong>se transformations wouldincrease business risk and require substantial investmentsand patience from investors. Given the pressures a listedcompany faced to meet expectations on short‐termperformance, management felt the public markets wouldnot provide the right environment for their ambitious newplans. Apax Partners also believed that New Look wouldbe better positioned to take advantage <strong>of</strong> these long‐termopportunities if taken private. Apax Partners partnered withPermira to do the deal. In April 2004, Apax Partners/Permiraeach invested £100 million in a buy‐out vehicle thatpurchased New Look; each assumed 30.1% stake, founderTom Singh held 23.3% and other management held 13.4%(3.1% was assumed by Dubai‐based retail giant Landmark).<strong>The</strong> deal represented a growth story: under the buyoutmanagement’s investment, New Look grew EBITDA annuallyby an average <strong>of</strong> 14.6% between 2004 and 2007 andincreased its full‐time equivalent headcount by 7.7% per yearon average in the same period. As active shareholders, theprivate equity partners supported New Look in making thelong‐term investments required in the transformation processand helped both to strengthen its management team aroundCEO Phil Wrigley and to increase its capital efficiency. <strong>The</strong>transformation process had three key initiatives. First wasinvestment in a new larger distribution centre, and re‐locatingit more centrally in England. Second was a continued andaccelerated roll‐out <strong>of</strong> larger store formats, enabling NewLook to <strong>of</strong>fer a wider product range in a more conduciveretail environment and to include men’s and children’s wearas counterweights to the cyclicality associated with women’sfashion. When the company found itself in a strong enoughposition to expand to markets beyond the UK, itimplemented the third key initiative: pursuing internationalexpansion in France, Belgium, Ireland, Kuwait, and Dubai.<strong>The</strong> New Look case presents an example <strong>of</strong> a company thatpursued an ambitious growth plan with the support <strong>of</strong> privateequity partners. <strong>The</strong> envisioned transformation processturned out to be highly successful with increasing efficienciesand pr<strong>of</strong>its as well as an increase <strong>of</strong> over 3,500 employeesover four years.<strong>The</strong> UK Retail Sector: 1998–2004By the late 1990s, clothing retailers typically benefited fromhealthy margins and positive cash flow and generated highreturns on capital, making them fundamentally attractive toinvestors. Yet the sector came with risks as well; fashion wasnotoriously cyclical – even a warm month during the wintercould spell disaster – and for trend‐setting brands, oneseason’s miss could represent tremendous losses. Analystsnoted that clothing markets were naturally fragmented dueto the fact that customers drive demand for niche concepts.Low barriers to entry into the industry meant competitionwas high. In the UK there were three significant full‐pricedselling cycles: Christmas, back‐to‐school and Easter.Like‐for‐like (LFL) sales, or same‐store sales, were dependentmainly on three things: the company’s local consumerenvironment (the store’s location); merchandising, essentiallythe appeal <strong>of</strong> the retailer’s clothing <strong>of</strong>ferings; and the maturity<strong>of</strong> the retailer’s stores. LFL sales growth drove a retailer’sability to leverage annual operating cost increases, soopportunities for space expansion and growth in marketshare determined sustainable growth.<strong>The</strong> late 1990s saw several significant forces affectingthe retail consumer. 1 Work and leisure patterns had changed,and a “money rich, time poor” consumer had emerged, witha concomitant increase in spending on leisure. Demographicshad also changed with a decline in younger people, a largeportion in their middle age, and an increase in single‐personhouseholds; all <strong>of</strong> which had implications for spending patterns.<strong>The</strong> retail sector witnessed an increase in consolidation <strong>of</strong> salesand a decrease in shop units. According to one study, thenumber <strong>of</strong> small, single independent retailers fell in the UKin tandem with their market share.1<strong>The</strong> following section draws in part on Tim Dixon and Andrew Marston, “<strong>The</strong> impact <strong>of</strong> e-commerce on retail real estate in the UK,” Journal <strong>of</strong> RealEstate Portfolio Management, 1 May 2002, vol. 8, no. 2, p. 153.<strong>The</strong> <strong>Global</strong> <strong>Economic</strong> <strong>Impact</strong> <strong>of</strong> <strong>Private</strong> <strong>Equity</strong> <strong>Report</strong> <strong>2008</strong> Case studies: New Look 103

- Page 2 and 3:

The Globalization of Alternative In

- Page 5:

ContributorsCo-editorsAnuradha Guru

- Page 9 and 10:

PrefaceKevin SteinbergChief Operati

- Page 11 and 12:

Letter on behalf of the Advisory Bo

- Page 13 and 14:

Executive summaryJosh lernerHarvard

- Page 15 and 16:

• Private equity-backed companies

- Page 17 and 18:

C. Indian casesThe two India cases,

- Page 19 and 20:

Part 1Large-sample studiesThe Globa

- Page 21 and 22:

The new demography of private equit

- Page 23 and 24:

among US publicly traded firms, it

- Page 25 and 26:

should be fairly complete. While th

- Page 27 and 28:

according to Moody’s (Hamilton et

- Page 29 and 30:

draining public markets of firms. I

- Page 31 and 32:

FIguresFigure 1A: LBO transactions

- Page 33 and 34:

TablesTable 1: Capital IQ 1980s cov

- Page 35 and 36:

Table 2: Magnitude and growth of LB

- Page 37 and 38:

Table 4: Exits of individual LBO tr

- Page 39 and 40:

Table 6: Determinants of exit succe

- Page 41 and 42:

Table 7: Ultimate staying power of

- Page 43 and 44:

Appendix 1: Imputed enterprise valu

- Page 45 and 46:

Private equity and long-run investm

- Page 47 and 48:

alternative names associated with t

- Page 49 and 50:

4. Finally, we explore whether firm

- Page 51 and 52:

When we estimate these regressions,

- Page 53 and 54:

cutting back on the number of filin

- Page 55 and 56:

Table 1: Summary statisticsPanel D:

- Page 57 and 58:

Table 4: Relative citation intensit

- Page 59 and 60:

figuresFigure 1: Number of private

- Page 61 and 62:

Private equity and employment*steve

- Page 63 and 64:

Especially when taken together, our

- Page 65 and 66:

centred on the transaction year ide

- Page 67 and 68:

and Vartia 1985.) Aggregate employm

- Page 69 and 70: sectors. In Retail Trade, the cumul

- Page 71 and 72: employment-weighted acquisition rat

- Page 73 and 74: FIguresFigure 1: Matches of private

- Page 75 and 76: Figure 6:Figure 6A: Comparison of n

- Page 77 and 78: Figure 8:Figure 8A: Comparison of j

- Page 79 and 80: Figure 11: Variation in impact in e

- Page 81 and 82: Figure 12: Differences in impact on

- Page 83 and 84: Private equity and corporate govern

- Page 85 and 86: et al (2007) track the evolution of

- Page 87 and 88: groups aim to improve firm performa

- Page 89 and 90: distribution of the LBO sponsors, m

- Page 91 and 92: the most difficult cases. This stor

- Page 93 and 94: to see whether these changes of CEO

- Page 95 and 96: Figure 3:This figure represents the

- Page 97 and 98: TablesTable 1: Company size descrip

- Page 99 and 100: Table 5: Changes in the board size,

- Page 101 and 102: Table 7: Board turnoverPanel A: Siz

- Page 103 and 104: Part 2Case studiesThe Global Econom

- Page 105 and 106: European private equity cases: intr

- Page 107 and 108: Exhibit 1: Private equity fund size

- Page 109 and 110: Messer Griesheimann-kristin achleit

- Page 111 and 112: ealized it was not possible to grow

- Page 113 and 114: The deal with Allianz Capital partn

- Page 115 and 116: the deal, the private equity invest

- Page 117 and 118: Exhibit 1: The Messer Griesheim dea

- Page 119: Exhibit 5: Post buyout structureMes

- Page 123 and 124: feet. This restricted store space w

- Page 125 and 126: institutional investors why this in

- Page 127 and 128: Although a public listing did not a

- Page 129 and 130: Exhibit 5: Employment development a

- Page 131 and 132: Chinese private equity cases: intro

- Page 133 and 134: Hony Capital and China Glass Holdin

- Page 135 and 136: Hony’s Chinese name means ambitio

- Page 137 and 138: Establishing early agreement on pos

- Page 139 and 140: Executing the IPOEach of the initia

- Page 141 and 142: Exhibit 1A: Summary of Hony Capital

- Page 143 and 144: Exhibit 4: Members of the China Gla

- Page 145 and 146: Exhibit 6A: China Glass post‐acqu

- Page 147 and 148: Exhibit 8: China Glass stock price

- Page 149 and 150: 3i Group plc and Little Sheep*Lily

- Page 151 and 152: y an aggressive franchise strategy,

- Page 153 and 154: soul” of the business. But there

- Page 155 and 156: Exhibit 1: Summary information on 3

- Page 157 and 158: Exhibit 6: An excerpt from the 180-

- Page 159 and 160: Indian private equity cases: introd

- Page 161 and 162: ICICI Venture and Subhiksha *Lily F

- Page 163 and 164: investment,” recalled Deshpande.

- Page 165 and 166: 2005 - 2007: Moderator, protector a

- Page 167 and 168: Exhibit 3: Subhiksha’s board comp

- Page 169 and 170: Warburg Pincus and Bharti Tele‐Ve

- Page 171 and 172:

founded two companies at this time

- Page 173 and 174:

By 2003 this restructuring task was

- Page 175 and 176:

Exhibit 1C: Private equity investme

- Page 177 and 178:

Exhibit 4B: Bharti cellular footpri

- Page 179 and 180:

Exhibit 6: Summary of Bharti’s fi

- Page 181 and 182:

Exhibit 7: Bharti’s board structu

- Page 183 and 184:

In the 1993‐94 academic year, he

- Page 185 and 186:

consumer products. She was also a R

- Page 187 and 188:

AcknowledgementsJosh LernerHarvard

- Page 189:

The World Economic Forum is an inde