Effectiveness and Economic Impact of Tax Incentives in the SADC ...

Effectiveness and Economic Impact of Tax Incentives in the SADC ...

Effectiveness and Economic Impact of Tax Incentives in the SADC ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

7-6 EFFECTIVENESS AND IMPACT OF TAX INCENTIVES IN THE <strong>SADC</strong> REGION<br />

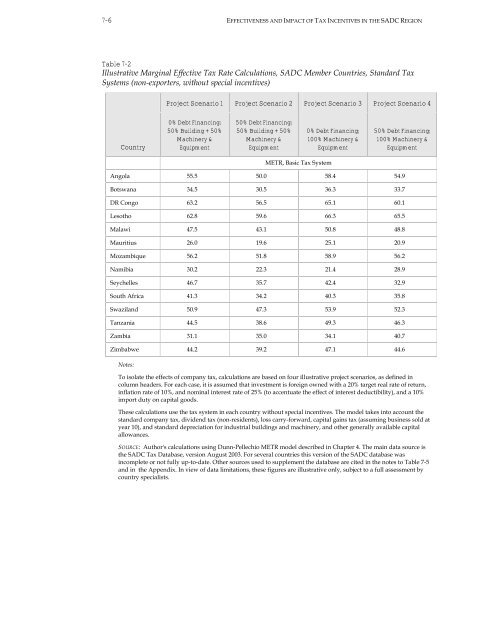

Table 7-2<br />

Illustrative Marg<strong>in</strong>al Effective <strong>Tax</strong> Rate Calculations, <strong>SADC</strong> Member Countries, St<strong>and</strong>ard <strong>Tax</strong><br />

Systems (non-exporters, without special <strong>in</strong>centives)<br />

Country<br />

Project Scenario 1 Project Scenario 2 Project Scenario 3 Project Scenario 4<br />

0% Debt F<strong>in</strong>anc<strong>in</strong>g;<br />

50% Build<strong>in</strong>g + 50%<br />

Mach<strong>in</strong>ery &<br />

Equipment<br />

50% Debt F<strong>in</strong>anc<strong>in</strong>g;<br />

50% Build<strong>in</strong>g + 50%<br />

Mach<strong>in</strong>ery &<br />

Equipment<br />

METR, Basic <strong>Tax</strong> System<br />

0% Debt F<strong>in</strong>anc<strong>in</strong>g;<br />

100% Mach<strong>in</strong>ery &<br />

Equipment<br />

50% Debt F<strong>in</strong>anc<strong>in</strong>g;<br />

100% Mach<strong>in</strong>ery &<br />

Equipment<br />

Angola 55.5 50.0 58.4 54.9<br />

Botswana 34.5 30.5 36.3 33.7<br />

DR Congo 63.2 56.5 65.1 60.1<br />

Lesotho 62.8 59.6 66.3 65.5<br />

Malawi 47.5 43.1 50.8 48.8<br />

Mauritius 26.0 19.6 25.1 20.9<br />

Mozambique 56.2 51.8 58.9 56.2<br />

Namibia 30.2 22.3 21.4 28.9<br />

Seychelles 46.7 35.7 42.4 32.9<br />

South Africa 41.3 34.2 40.3 35.8<br />

Swazil<strong>and</strong> 50.9 47.3 53.9 52.3<br />

Tanzania 44.5 38.6 49.3 46.3<br />

Zambia 31.1 35.0 34.1 40.7<br />

Zimbabwe 44.2 39.2 47.1 44.6<br />

Notes:<br />

To isolate <strong>the</strong> effects <strong>of</strong> company tax, calculations are based on four illustrative project scenarios, as def<strong>in</strong>ed <strong>in</strong><br />

column headers. For each case, it is assumed that <strong>in</strong>vestment is foreign owned with a 20% target real rate <strong>of</strong> return,<br />

<strong>in</strong>flation rate <strong>of</strong> 10%, <strong>and</strong> nom<strong>in</strong>al <strong>in</strong>terest rate <strong>of</strong> 25% (to accentuate <strong>the</strong> effect <strong>of</strong> <strong>in</strong>terest deductibility), <strong>and</strong> a 10%<br />

import duty on capital goods.<br />

These calculations use <strong>the</strong> tax system <strong>in</strong> each country without special <strong>in</strong>centives. The model takes <strong>in</strong>to account <strong>the</strong><br />

st<strong>and</strong>ard company tax, dividend tax (non-residents), loss carry-forward, capital ga<strong>in</strong>s tax (assum<strong>in</strong>g bus<strong>in</strong>ess sold at<br />

year 10), <strong>and</strong> st<strong>and</strong>ard depreciation for <strong>in</strong>dustrial build<strong>in</strong>gs <strong>and</strong> mach<strong>in</strong>ery, <strong>and</strong> o<strong>the</strong>r generally available capital<br />

allowances.<br />

SOURCE: Author's calculations us<strong>in</strong>g Dunn-Pellechio METR model described <strong>in</strong> Chapter 4. The ma<strong>in</strong> data source is<br />

<strong>the</strong> <strong>SADC</strong> <strong>Tax</strong> Database, version August 2003. For several countries this version <strong>of</strong> <strong>the</strong> <strong>SADC</strong> database was<br />

<strong>in</strong>complete or not fully up-to-date. O<strong>the</strong>r sources used to supplement <strong>the</strong> database are cited <strong>in</strong> <strong>the</strong> notes to Table 7-5<br />

<strong>and</strong> <strong>in</strong> <strong>the</strong> Appendix. In view <strong>of</strong> data limitations, <strong>the</strong>se figures are illustrative only, subject to a full assessment by<br />

country specialists.