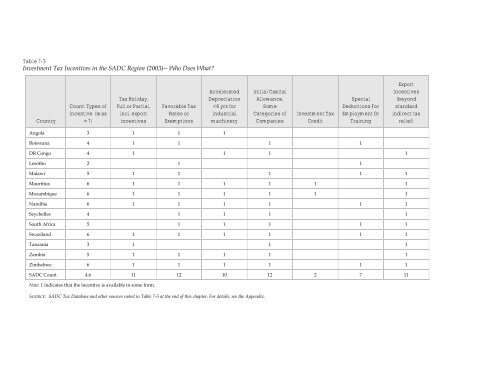

Table 7-3 Investment <strong>Tax</strong> <strong>Incentives</strong> <strong>in</strong> <strong>the</strong> <strong>SADC</strong> Region (2003)-- Who Does What? Country Angola Botswana DR Congo Lesotho Malawi Mauritius Mozambique Namibia Seychelles South Africa Swazil<strong>and</strong> Tanzania Zambia Zimbabwe <strong>SADC</strong> Count Count: Types <strong>of</strong> Incentive (max = 7) <strong>Tax</strong> Holiday, Full or Partial, <strong>in</strong>cl. export <strong>in</strong>centives Favorable <strong>Tax</strong> Rates or Exemptions Accelerated Depreciation

TAX SYSTEMS AND INCENTIVES IN THE <strong>SADC</strong> REGION 7-9 Exhibit 7-1 Strategic Industrial Projects Program <strong>in</strong> South Africa In November 2001, <strong>the</strong> government <strong>of</strong> South Africa issued regulations def<strong>in</strong><strong>in</strong>g a new regime <strong>of</strong> tax <strong>in</strong>centives for Strategic Industrial Projects (SIP) to encourage selected <strong>in</strong>dustrial <strong>in</strong>vestments <strong>and</strong> stimulate growth, development, <strong>and</strong> competitiveness. Compared to many <strong>in</strong>centive programs, <strong>the</strong> SIP is well designed. The favorable features <strong>in</strong>clude: • Coherent Target<strong>in</strong>g. The sectors targeted by <strong>the</strong> SIP program are not atypical: new projects <strong>in</strong> manufactur<strong>in</strong>g, computer technology, <strong>and</strong> research <strong>and</strong> development. But <strong>the</strong> screen<strong>in</strong>g system applies a scor<strong>in</strong>g system that is highly coherent with <strong>the</strong> policy goals. Po<strong>in</strong>t are allotted for new products or processes, for fill<strong>in</strong>g a critical gap <strong>in</strong> an <strong>in</strong>dustrial cluster, for value added <strong>of</strong> at least 35 percent, for procurement from small, medium <strong>and</strong> micro enterprises, for <strong>in</strong>frastructure provision, <strong>and</strong> for full-time jobs created per million R<strong>and</strong> <strong>of</strong> <strong>in</strong>vestment. The po<strong>in</strong>t score determ<strong>in</strong>es qualify<strong>in</strong>g status <strong>and</strong> <strong>the</strong> level <strong>of</strong> benefits. Job creation can account for up to 4 po<strong>in</strong>ts on a scale <strong>of</strong> 10. • Attractive Benefits that Still Generate Revenue. The sole tax benefit is an <strong>in</strong>itial capital allowance (ICA) <strong>of</strong> 50 or 100 percent, depend<strong>in</strong>g on <strong>the</strong> qualify<strong>in</strong>g po<strong>in</strong>t score. The ICA is additional to normal accelerated depreciation. This is very attractive to <strong>in</strong>vestors <strong>and</strong> yet fiscally reasonable. That is to say, <strong>the</strong> <strong>in</strong>itial allowance substantially lowers <strong>the</strong> METR for most projects, while yield<strong>in</strong>g significant revenue <strong>in</strong> <strong>the</strong> medium run. SOURCE: Section 12G <strong>of</strong> <strong>the</strong> Income <strong>Tax</strong> Act, <strong>and</strong> DTI promotional documents. • Cost Limits. The program sets a ceil<strong>in</strong>g (up to R600 million) on <strong>the</strong> cost <strong>of</strong> <strong>the</strong> <strong>in</strong>dustrial assets that may qualify for <strong>the</strong> ICA for any one project. Separately, <strong>the</strong> law sets a ceil<strong>in</strong>g <strong>of</strong> R10 billion on <strong>the</strong> cumulative amount <strong>of</strong> ICA benefits that can be granted under <strong>the</strong> program. • Transparency. Under <strong>the</strong> SIP program, <strong>the</strong> qualify<strong>in</strong>g criteria are explicit <strong>and</strong> substantive, applications are to be gazetted promptly, awards are to be reported annually, <strong>and</strong> revenue costs are to be monitored. • Clawback Provisions. In addition to st<strong>and</strong>ard provisions for cancel<strong>in</strong>g benefits due to noncompliance with performance or report<strong>in</strong>g requirements, <strong>the</strong> program provides for possible tax penalties <strong>in</strong> <strong>the</strong> event that benefits are disallowed. To be sure, <strong>the</strong> program has weakness. First, <strong>the</strong> M<strong>in</strong>ister <strong>of</strong> Trade Industry must take <strong>in</strong>to account, but not necessarily heed, <strong>the</strong> recommendations <strong>of</strong> <strong>the</strong> adjudication committee. Thus, decisions may still be discretionary. Second, <strong>the</strong> critical job criterion <strong>in</strong>cludes “<strong>in</strong>direct jobs,” for which figures are easy to manipulate <strong>and</strong> difficult to substantiate. Third, <strong>the</strong> benefits strongly favor projects with a rapid payback period, <strong>and</strong> projects run by companies with o<strong>the</strong>r <strong>in</strong>dustrial <strong>in</strong>come aga<strong>in</strong>st which to <strong>of</strong>fset tax losses <strong>in</strong> early years. For st<strong>and</strong>alone projects with a long payback period, <strong>the</strong> present value <strong>of</strong> <strong>the</strong> allowance may be small.

- Page 1:

TECHNICAL REPORT Effectiveness and

- Page 5 and 6:

Contents Executive Summary xi 1. In

- Page 7 and 8:

Contents (continued) ILLUSTRATIONS

- Page 9 and 10:

Glossary ACT additional company tax

- Page 11 and 12:

Preface The Scope of Work (SOW) for

- Page 13:

PREFACE IX Export Development & Inv

- Page 16 and 17:

XII EFFECTIVENESS AND IMPACT OF TAX

- Page 18 and 19:

XIV EFFECTIVENESS AND IMPACT OF TAX

- Page 20 and 21:

XVI EFFECTIVENESS AND IMPACT OF TAX

- Page 22 and 23:

XVIII EFFECTIVENESS AND IMPACT OF T

- Page 25 and 26:

1. Introduction Why should schemes

- Page 27 and 28:

INTRODUCTION 1-3 well administered.

- Page 29 and 30:

INTRODUCTION 1-5 from selective to

- Page 31 and 32:

2. Taxation, Investment, and Growth

- Page 33 and 34:

TAXATION, INVESTMENT, AND GROWTH 2-

- Page 35 and 36:

TAXATION, INVESTMENT, AND GROWTH 2-

- Page 37 and 38:

TAXATION, INVESTMENT, AND GROWTH 2-

- Page 39 and 40:

TAXATION, INVESTMENT, AND GROWTH 2-

- Page 41 and 42:

TAXATION, INVESTMENT, AND GROWTH 2-

- Page 43:

TAXATION, INVESTMENT, AND GROWTH 2-

- Page 46 and 47:

3-2 EFFECTIVENESS AND IMPACT OF TAX

- Page 48 and 49:

3-4 EFFECTIVENESS AND IMPACT OF TAX

- Page 50 and 51:

3-6 EFFECTIVENESS AND IMPACT OF TAX

- Page 52 and 53:

3-8 EFFECTIVENESS AND IMPACT OF TAX

- Page 54 and 55:

3-10 EFFECTIVENESS AND IMPACT OF TA

- Page 56 and 57:

3-12 EFFECTIVENESS AND IMPACT OF TA

- Page 58 and 59:

3-14 EFFECTIVENESS AND IMPACT OF TA

- Page 60 and 61:

3-16 EFFECTIVENESS AND IMPACT OF TA

- Page 62 and 63:

3-18 EFFECTIVENESS AND IMPACT OF TA

- Page 64 and 65:

3-20 EFFECTIVENESS AND IMPACT OF TA

- Page 66 and 67: 4-2 EFFECTIVENESS AND IMPACT OF TAX

- Page 68 and 69: 4-4 EFFECTIVENESS AND IMPACT OF TAX

- Page 70 and 71: 4-6 EFFECTIVENESS AND IMPACT OF TAX

- Page 72 and 73: 4-8 EFFECTIVENESS AND IMPACT OF TAX

- Page 74 and 75: 4-10 EFFECTIVENESS AND IMPACT OF TA

- Page 76 and 77: 4-12 EFFECTIVENESS AND IMPACT OF TA

- Page 78 and 79: 4-14 EFFECTIVENESS AND IMPACT OF TA

- Page 80 and 81: 5-2 EFFECTIVENESS AND IMPACT OF TAX

- Page 82 and 83: 5-4 EFFECTIVENESS AND IMPACT OF TAX

- Page 84 and 85: 5-6 EFFECTIVENESS AND IMPACT OF TAX

- Page 86 and 87: 5-8 EFFECTIVENESS AND IMPACT OF TAX

- Page 88 and 89: 5-10 EFFECTIVENESS AND IMPACT OF TA

- Page 90 and 91: 5-12 EFFECTIVENESS AND IMPACT OF TA

- Page 92 and 93: 5-14 EFFECTIVENESS AND IMPACT OF TA

- Page 95 and 96: 6. Economics of Harmful Tax Competi

- Page 97 and 98: ECONOMICS OF HARMFUL TAX COMPETITIO

- Page 99 and 100: ECONOMICS OF HARMFUL TAX COMPETITIO

- Page 101 and 102: ECONOMICS OF HARMFUL TAX COMPETITIO

- Page 103 and 104: ECONOMICS OF HARMFUL TAX COMPETITIO

- Page 105 and 106: ECONOMICS OF HARMFUL TAX COMPETITIO

- Page 107 and 108: ECONOMICS OF HARMFUL TAX COMPETITIO

- Page 109 and 110: 7. Tax Systems and Tax Incentives i

- Page 111 and 112: TAX SYSTEMS AND INCENTIVES IN THE S

- Page 113 and 114: TAX SYSTEMS AND INCENTIVES IN THE S

- Page 115: TAX SYSTEMS AND INCENTIVES IN THE S

- Page 119 and 120: TAX SYSTEMS AND INCENTIVES IN THE S

- Page 121 and 122: TAX SYSTEMS AND INCENTIVES IN THE S

- Page 123 and 124: TAX SYSTEMS AND INCENTIVES IN THE S

- Page 125 and 126: TAX SYSTEMS AND INCENTIVES IN THE S

- Page 127 and 128: TAX SYSTEMS AND INCENTIVES IN THE S

- Page 129 and 130: TAX SYSTEMS AND INCENTIVES IN THE S

- Page 131 and 132: Table 7-5 Elements of Tax Structure

- Page 133 and 134: Table 7-5 (continued) Sheet 3 of 4

- Page 135 and 136: Notes a Mozambique information Coun

- Page 137 and 138: 8. Conclusions and Recommendations

- Page 139 and 140: CONCLUSIONS AND RECOMMENDATIONS 8-3

- Page 141 and 142: CONCLUSIONS AND RECOMMENDATIONS 8-5

- Page 143 and 144: CONCLUSIONS AND RECOMMENDATIONS 8-7

- Page 145: CONCLUSIONS AND RECOMMENDATIONS 8-9

- Page 148 and 149: R-2 EFFECTIVENESS AND IMPACT OF TAX

- Page 150 and 151: R-4 EFFECTIVENESS AND IMPACT OF TAX

- Page 152 and 153: R-6 EFFECTIVENESS AND IMPACT OF TAX

- Page 154 and 155: A-2 APPENDIX The present investment

- Page 156 and 157: A-4 APPENDIX Democratic Republic of

- Page 158 and 159: A-6 APPENDIX Government revenue in

- Page 160 and 161: A-8 APPENDIX income tax payable by

- Page 162 and 163: A-10 APPENDIX (though they are obli

- Page 164 and 165: A-12 APPENDIX • • • Asset All

- Page 166 and 167:

A-14 APPENDIX also get zero import

- Page 168 and 169:

A-16 APPENDIX EPZ measure was motiv