SPecIAL - Alu-web.de

SPecIAL - Alu-web.de

SPecIAL - Alu-web.de

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

E c o n o M i c s<br />

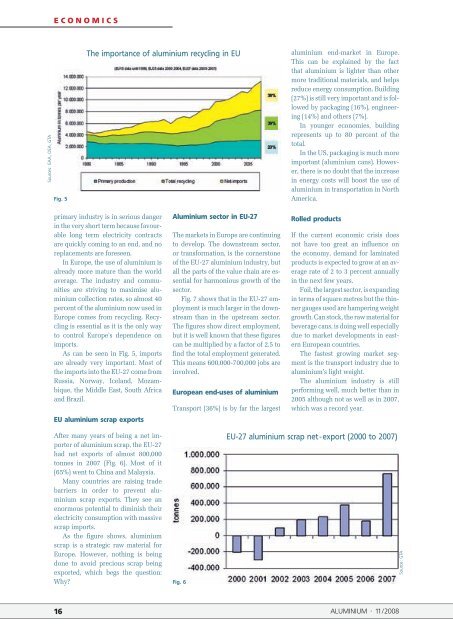

Sources: EAA, OEA, GTA<br />

Fig. 5<br />

The importance of aluminium recycling in EU<br />

aluminium endmarket in Europe.<br />

This can be explained by the fact<br />

that aluminium is lighter than other<br />

more traditional materials, and helps<br />

reduce energy consumption. Building<br />

(27%) is still very important and is followed<br />

by packaging (16%), engineering<br />

(14%) and others (7%).<br />

In younger economies, building<br />

represents up to 80 percent of the<br />

total.<br />

In the US, packaging is much more<br />

important (aluminium cans). However,<br />

there is no doubt that the increase<br />

in energy costs will boost the use of<br />

aluminium in transportation in North<br />

America.<br />

primary industry is in serious danger<br />

in the very short term because favourable<br />

long term electricity contracts<br />

are quickly coming to an end, and no<br />

replacements are foreseen.<br />

In Europe, the use of aluminium is<br />

already more mature than the world<br />

average. The industry and communities<br />

are striving to maximise aluminium<br />

collection rates, so almost 40<br />

percent of the aluminium now used in<br />

Europe comes from recycling. Recycling<br />

is essential as it is the only way<br />

to control Europe’s <strong>de</strong>pen<strong>de</strong>nce on<br />

imports.<br />

As can be seen in Fig. 5, imports<br />

are already very important. Most of<br />

the imports into the EU27 come from<br />

Russia, Norway, Iceland, Mozambique,<br />

the Middle East, South Africa<br />

and Brazil.<br />

EU aluminium scrap exports<br />

<strong>Alu</strong>minium sector in EU-27<br />

The markets in Europe are continuing<br />

to <strong>de</strong>velop. The downstream sector,<br />

or transformation, is the cornerstone<br />

of the EU27 aluminium industry, but<br />

all the parts of the value chain are essential<br />

for harmonious growth of the<br />

sector.<br />

Fig. 7 shows that in the EU27 employment<br />

is much larger in the downstream<br />

than in the upstream sector.<br />

The figures show direct employment,<br />

but it is well known that these figures<br />

can be multiplied by a factor of 2.5 to<br />

find the total employment generated.<br />

This means 600,000700,000 jobs are<br />

involved.<br />

European end-uses of aluminium<br />

Transport (36%) is by far the largest<br />

Rolled products<br />

If the current economic crisis does<br />

not have too great an influence on<br />

the economy, <strong>de</strong>mand for laminated<br />

products is expected to grow at an average<br />

rate of 2 to 3 percent annually<br />

in the next few years.<br />

Foil, the largest sector, is expanding<br />

in terms of square metres but the thinner<br />

gauges used are hampering weight<br />

growth. Can stock, the raw material for<br />

beverage cans, is doing well especially<br />

due to market <strong>de</strong>velopments in eastern<br />

European countries.<br />

The fastest growing market segment<br />

is the transport industry due to<br />

aluminium’s light weight.<br />

The aluminium industry is still<br />

performing well, much better than in<br />

2005 although not as well as in 2007,<br />

which was a record year.<br />

After many years of being a net importer<br />

of aluminium scrap, the EU27<br />

had net exports of almost 800,000<br />

tonnes in 2007 (Fig. 6). Most of it<br />

(65%) went to China and Malaysia.<br />

Many countries are raising tra<strong>de</strong><br />

barriers in or<strong>de</strong>r to prevent aluminium<br />

scrap exports. They see an<br />

enormous potential to diminish their<br />

electricity consumption with massive<br />

scrap imports.<br />

As the figure shows, aluminium<br />

scrap is a strategic raw material for<br />

Europe. However, nothing is being<br />

done to avoid precious scrap being<br />

exported, which begs the question:<br />

Why?<br />

Fig. 6<br />

EU-27 aluminium scrap net - export (2000 to 2007)<br />

Source: GTA<br />

16 ALUMINIUM · 11/2008