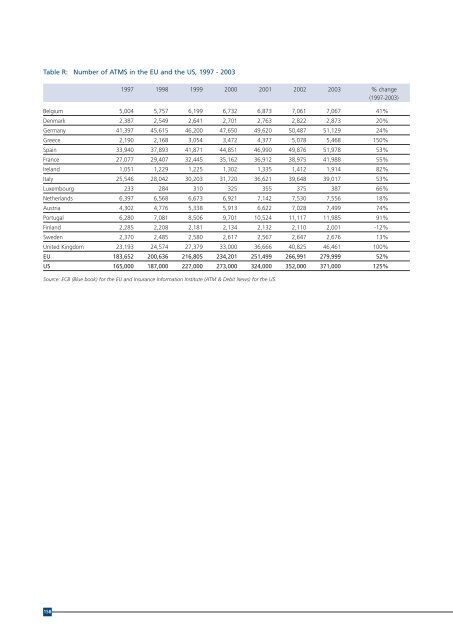

Table R: Number <strong>of</strong> ATMS in <strong>the</strong> <strong>EU</strong> <strong>and</strong> <strong>the</strong> <strong>US</strong>, 1997 - 2003 1997 1998 1999 2000 2001 2002 2003 % change (1997-2003) Belgium 5,004 5,757 6,199 6,732 6,873 7,061 7,067 41% Denmark 2,387 2,549 2,641 2,701 2,763 2,822 2,873 20% Germany 41,397 45,615 46,200 47,650 49,620 50,487 51,129 24% Greece 2,190 2,168 3,054 3,472 4,377 5,078 5,468 150% Spain 33,940 37,893 41,871 44,851 46,990 49,876 51,978 53% France 27,077 29,407 32,445 35,162 36,912 38,975 41,988 55% Irel<strong>and</strong> 1,051 1,229 1,225 1,302 1,335 1,412 1,914 82% Italy 25,546 28,042 30,203 31,720 36,621 39,648 39,017 53% Luxembourg 233 284 310 325 355 375 387 66% Ne<strong>the</strong>rl<strong>and</strong>s 6,397 6,568 6,673 6,921 7,142 7,530 7,556 18% Austria 4,302 4,776 5,338 5,913 6,622 7,028 7,499 74% Portugal 6,280 7,081 8,506 9,701 10,524 11,117 11,985 91% Finl<strong>and</strong> 2,285 2,208 2,181 2,134 2,132 2,110 2,001 -12% Sweden 2,370 2,485 2,580 2,617 2,567 2,647 2,676 13% United Kingdom 23,193 24,574 27,379 33,000 36,666 40,825 46,461 100% <strong>EU</strong> 183,652 200,636 216,805 234,201 251,499 266,991 279,999 52% <strong>US</strong> 165,000 187,000 227,000 273,000 324,000 352,000 371,000 125% Source: ECB (Blue book) for <strong>the</strong> <strong>EU</strong> <strong>and</strong> Insurance Information Institute (ATM & Debit News) for <strong>the</strong> <strong>US</strong>. 158

Annex 3: Bibliography A - American Bankers Association <strong>and</strong> <strong>the</strong> Conference <strong>of</strong> State Bank Supervisors “The benefits <strong>of</strong> charter choice – <strong>the</strong> dual <strong>banking</strong> system as a case study”, June 24, 2005 - America’s Community Bankers (ACB), Policy Positions, 2005 - Avery R.B.<strong>and</strong> Samolyk K. “Bank Consolidation <strong>and</strong> <strong>the</strong> Provision <strong>of</strong> Banking Services: The Case <strong>of</strong> Small Commercial Loans”, Working Paper 2000-01, Federal Deposit Insurance Corporation - Ayadi R. <strong>and</strong> Pujals G. “Banking Consolidation in <strong>the</strong> <strong>EU</strong>: Overviews <strong>and</strong> Prospects”, May 2004 B - Banco de España “Boletín Estadístico” - Bassett, William F. <strong>and</strong> Thomas F. Brady, “The Economic Performance <strong>of</strong> Small Banks, 1985-2000”, November 2001, Federal Reserve Bulletin - Berger A. <strong>and</strong> Udell “Small Business Credit Availability <strong>and</strong> Relationship Lending: The Importance <strong>of</strong> Bank Organisational Structure”, 2002, Economic Journal - Berger A., Goldberg L. G. <strong>and</strong> White L. J., “The Effects <strong>of</strong> Dynamic Changes in Bank Competition on <strong>the</strong> Supply <strong>of</strong> Small Business Credit”, 2001, European Finance Review C - Carnevali F. (Dr) “Europe's Advantage: Banks <strong>and</strong> Small Firms in Europe <strong>and</strong> Britain” - CEPS Research Report in Finance <strong>and</strong> Banking, No 34 - CESR <strong>and</strong> <strong>the</strong> European Central Bank Report “St<strong>and</strong>ards for Securities Clearing <strong>and</strong> Settlement in <strong>the</strong> European Union”, September 2004 (CESR/04-561) - CESR “Recommendations for <strong>the</strong> consistent implementation <strong>of</strong> <strong>the</strong> European Commission’s Regulation on Prospectuses nº 809/2004”, February 2005 - Colantuoni J.A. “Mutual to stock conversions, problems with <strong>the</strong> pricing <strong>of</strong> IPOs”, FDIC Banking Review - CSFI Study “Europe’s new banks – The “non-bank” phenomenon”, June 2000 D - DeYoung R. <strong>and</strong> Duffy D., “The challenges facing community banks: in <strong>the</strong>ir own words”, 4Q 2002 - De Young R., Hunter W. <strong>and</strong> Udell G. “The Past, Present, <strong>and</strong> Probable Future for Community Banks”, 2004 - Deutsche Bank Research, “Transatlantic financial market integration: Ambition needed”, 29 November 2005 E - The Economist “Trust me, I’m a banker: survey on international <strong>banking</strong>”, 15th April 2004 - EIB Papers “SME Finance in Europe: introduction <strong>and</strong> overview”, 2003, volume 8 n°2 - European Central Bank (ECB) “Role <strong>of</strong> Central Banks in Prudential Supervision”, March 2001 - European Central Bank (ECB) “Banking Integration in <strong>the</strong> Euro Area”, December 2002 - European Central Bank (ECB) “<strong>EU</strong> Banking Sector Stability”, February 2003 - European Central Bank (ECB) Occasional Paper Series Nr.20, August 2004 - European Central Bank (ECB) “Report on <strong>EU</strong> <strong>banking</strong> structure”, November 2004 - European Central Bank (ECB) “Blue Book Addendum incorporating 2003 figures”, August 2005 - European Commission Staff Working Document “Cross-border consolidation in <strong>the</strong> <strong>EU</strong> financial sector”, September 2005 - European Commission “Final report <strong>of</strong> <strong>the</strong> Committee <strong>of</strong> wise men on <strong>the</strong> regulation <strong>of</strong> European securities <strong>markets</strong>”, 15 February 2001, Brussels - European Commission Staff Working Paper “Enterprises’ access to finance”, October 2001 - European Commission consultation document “Mutual societies in an enlarged Europe”, 3.10.2003 - European Commission “Microcredit for small businesses <strong>and</strong> business creation: bridging a market gap”, December 2003 - European Commission, Forum Group on Mortgage Credit Report, “The integration <strong>of</strong> <strong>the</strong> <strong>EU</strong> mortgage credit <strong>markets</strong>”, 2004 - European Credit Research Institute “Briefing on consumer credit, indebtedness <strong>and</strong> over indebtedness in <strong>the</strong> <strong>EU</strong>”, April 2003 - European Financial Roundtable “EFR recommendations on regulation <strong>and</strong> supervision”, 28 Oct 2003 - European Financial Roundtable “EFR report 'Towards a lead supervisor for cross border financial institutions in <strong>the</strong> <strong>EU</strong>'”, 15 Jun 2004 - European Financial Roundtable “Third EFR report on lead supervisor concept”, 29 Jun 2005 - European Mortgage Federation, “Hypostat 2003: European Housing Finance Review”, September 2004 - European Savings Banks Group “Perspectives 44: The Future Organisation <strong>of</strong> Financial Regulation <strong>and</strong> Supervision in <strong>the</strong> European Union - Position <strong>of</strong> <strong>the</strong> European Savings Banks Group”, August 2002 - European Savings Banks Group study “The Future <strong>of</strong> European Retail Banking Markets”, June 2003 - European Savings Banks Group “Perspectives 48: The Legal Environment <strong>of</strong> <strong>the</strong> Savings Banks in Europe”, June 2005 159

- Page 1:

September 2006 RESEARCH A COMPARATI

- Page 4 and 5:

IE UK FR BE NL LU DK DE SE CZ AT SL

- Page 6 and 7:

The following WSBI/ESBG committees

- Page 8 and 9:

4 Regulation and supervision compar

- Page 10 and 11:

6.5 Issues of competition in retail

- Page 12 and 13:

To finish, if we had to pick from a

- Page 14 and 15:

In the US, credit institutions have

- Page 16 and 17:

Following the same logic, the EU co

- Page 18 and 19:

In that context, it is tempting to

- Page 21 and 22:

3. INSTITUTIONAL COMPARISON 3.1 Sec

- Page 23 and 24:

The market share of the US banking

- Page 25 and 26:

FDIC-insured commercial banks are i

- Page 27 and 28:

The subsidiary stock institution is

- Page 29 and 30:

Regulatory reform over the past thi

- Page 31 and 32:

State credit unions were first exem

- Page 33 and 34:

There has however been much effort

- Page 35 and 36:

3.2.2.2.2.2 Ownership and corporate

- Page 37 and 38:

Hermann Schulze-Delitzsch and Fried

- Page 39 and 40:

In contrast, building societies in

- Page 41 and 42:

The commitment of savings banks is

- Page 43 and 44:

4. REGULATION AND SUPERVISION COMPA

- Page 45 and 46:

In addition, for regulations define

- Page 47 and 48:

The European Parliament has to be k

- Page 49 and 50:

In fact, it should be mentioned her

- Page 51 and 52:

As far as coordination at the feder

- Page 53 and 54:

Despite the trend towards the estab

- Page 55 and 56:

Another important factor in the cho

- Page 57 and 58:

In the European Union, contrary to

- Page 59 and 60:

Although younger than CESR, both CE

- Page 61 and 62:

4.2.5.1.1.1.1 Limitation of the geo

- Page 63 and 64:

4.2.5.1.1.3 Recent trend: regulatio

- Page 65 and 66:

Another important common feature be

- Page 67 and 68:

The best execution rule was first m

- Page 69 and 70:

4.3.2.2.4 National Market System ru

- Page 71 and 72:

The ISD set a basis for the develop

- Page 73:

Best execution rules exist in both

- Page 76 and 77:

The decline of savings institutions

- Page 78 and 79:

Relative to population, the Europea

- Page 80 and 81:

5.2.2 Size of credit institutions 5

- Page 82 and 83:

5.2.2.2 European Union In Europe, t

- Page 84 and 85:

5.2.3 Concentration and consolidati

- Page 86 and 87:

5.2.3.2 European Union Average CR5

- Page 88 and 89:

In terms of the nature of consolida

- Page 90 and 91:

100% Graph 9: Structure of the asse

- Page 92 and 93:

In terms of growth of the volume of

- Page 94 and 95:

5.3.2 Efficiency of credit institut

- Page 96 and 97:

Table 16: Evolution of the Return o

- Page 98 and 99:

Finally, looking at cost-income rat

- Page 100 and 101:

9. The last couple of decades have

- Page 102 and 103:

102

- Page 104 and 105:

Furthermore, the average outstandin

- Page 106 and 107:

Under an open-end credit, the credi

- Page 108 and 109: Table 19: Evolution of outstanding

- Page 110 and 111: 6.2.1.2.2 Regulatory framework over

- Page 112 and 113: 6.2.1.3 Comparison 6.2.1.3.1 Size o

- Page 114 and 115: In terms of market competition, the

- Page 116 and 117: The residential mortgage market in

- Page 118 and 119: Funding by retail deposits represen

- Page 120 and 121: In sharp contrast, the US mortgage

- Page 122 and 123: 6.2.3.1.2 Lenders to small business

- Page 124 and 125: The securitisation process requires

- Page 126 and 127: Factoring is also continuously gain

- Page 128 and 129: 6.2.3.2.4 Securitisation of small b

- Page 130 and 131: The above fears can hardly be allay

- Page 132 and 133: - ACH credits and debits: the stati

- Page 134 and 135: 6.3.2.1.2 Financial intermediaries

- Page 136 and 137: It should be noted that two of the

- Page 138 and 139: Assuming that technology, globalisa

- Page 140 and 141: The report adds: “although it bou

- Page 142 and 143: Graph 19: Use of different distribu

- Page 144 and 145: In terms of funding of the business

- Page 146 and 147: Since then, established banks have

- Page 148 and 149: 148

- Page 150 and 151: MoU Memorandum of Understanding OTC

- Page 152 and 153: Annex 2: Statistical appendix Table

- Page 154 and 155: Table F: Share of US banking indust

- Page 156 and 157: Table L: Structure of the liabiliti

- Page 160 and 161: F - Federal Deposit Insurance Corpo

- Page 162 and 163: 162