Grain Legumes and Green Manures for Soil Fertility in ... - cimmyt

Grain Legumes and Green Manures for Soil Fertility in ... - cimmyt

Grain Legumes and Green Manures for Soil Fertility in ... - cimmyt

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

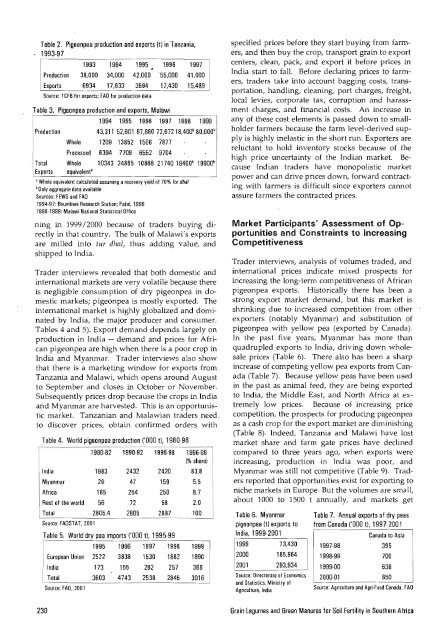

Table 2. Pigeonpea production <strong>and</strong> exports (t) <strong>in</strong> Tanzania,<br />

1993·97<br />

1993 1994<br />

Production 38,000 34,000<br />

1995 1996<br />

42,000 '55,000<br />

Exports 6934 17,633 3594 17,430<br />

Source: TCFB <strong>for</strong> exports; FAD <strong>for</strong> production data<br />

Table 3. Pigeonpea production <strong>and</strong> exports, Malawi<br />

1997<br />

41,000<br />

15,489<br />

1994 1995 1996 1997 1998 1999<br />

Production 43,311 52,601 87,880 72.67218,400b 80,000b<br />

Whole 1209 13852 1506 7877<br />

Processed 6394 7709 6552 9704<br />

Total Whole 10343 24865 10866 21740 18400 b 19600 b<br />

Exports equivalent'<br />

• Whole equivalent calculated assum<strong>in</strong>g arecovery yield of 70% <strong>for</strong> dhill<br />

b Only aggregate data available<br />

Sources: FEWS <strong>and</strong> FAD<br />

1994·97: Bvumbwe Research Station; Patel, 1998<br />

1998·1999: Malawi National Statistical Office<br />

n<strong>in</strong>g <strong>in</strong> 1999/2000 because of traders buy<strong>in</strong>g directly<br />

<strong>in</strong> that country. The bulk of Malawi's exports<br />

are milled <strong>in</strong>to fur dhal, thus add<strong>in</strong>g value, <strong>and</strong><br />

shipped to India.<br />

Trader <strong>in</strong>terviews revealed that both domestic <strong>and</strong><br />

<strong>in</strong>ternational markets are very volatile because there<br />

is negligible consumption of dry pigeonpea <strong>in</strong> domestic<br />

markets; pigeonpea is mostly exported. The<br />

<strong>in</strong>ternational market is highly globalized <strong>and</strong> dom<strong>in</strong>ated<br />

by India, the major producer <strong>and</strong> consumer.<br />

Tables 4 <strong>and</strong> 5). Export dem<strong>and</strong> depends largely on<br />

production <strong>in</strong> India -- dem<strong>and</strong> <strong>and</strong> prices <strong>for</strong> African<br />

pigeonpea are high when there is a poor crop <strong>in</strong><br />

India <strong>and</strong> Myanmar. Trader <strong>in</strong>terviews also show<br />

that there is a market<strong>in</strong>g w<strong>in</strong>dow <strong>for</strong> exports from<br />

Tanzania <strong>and</strong> Malawi, which opens around August<br />

to September <strong>and</strong> closes <strong>in</strong> October or November.<br />

Subsequently prices drop because the crops <strong>in</strong> India<br />

<strong>and</strong> Myanmar are harvested. This is an opportunistic<br />

market. Tanzanian <strong>and</strong> 'Malawian traders need.<br />

to discover prices, obta<strong>in</strong> confirmed orders with<br />

Table 4. World pigeonpea production ('000 t), 1980·98<br />

1980·82 1990·92 1996·98 1996·98<br />

1% share)<br />

India 1983 2432 2420 83.8<br />

Myanmar 29 47 159 5.5<br />

Africa 165 254 250 8.7<br />

Rest of the world 56 72 58 2.0<br />

Total 2805.4 2805 2887 100<br />

Source: FADSTAT. 2001<br />

Table 5. World dry pea imports ('000 t), 1995·99<br />

1995 1996 1997 1998 1999<br />

European Union 2522 3838 1530 1882 1890<br />

India 173 155 282 257 366<br />

Total 3603 4743 2538 2845 3016<br />

Source: FAD. 2001<br />

specified prices be<strong>for</strong>e they start buy<strong>in</strong>g from farmers,<br />

<strong>and</strong> then buy the crop, transport gra<strong>in</strong> to export<br />

centers, clean, pack, <strong>and</strong> export it be<strong>for</strong>e prices <strong>in</strong><br />

India start to fall. Be<strong>for</strong>e declar<strong>in</strong>g prices to farmers,<br />

traders take <strong>in</strong>to account bagg<strong>in</strong>g costs, transportation,<br />

h<strong>and</strong>l<strong>in</strong>g, clean<strong>in</strong>g, port charges, freight,<br />

local levies, corporate tax, corruption <strong>and</strong> harassment<br />

charges, <strong>and</strong> f<strong>in</strong>ancial costs. An <strong>in</strong>crease <strong>in</strong><br />

any of these cost elements is passed down to smallholder<br />

farmers because the farm level-derived supply<br />

is highly <strong>in</strong>elastic <strong>in</strong> the short run. Exporters are<br />

reluctant to hold <strong>in</strong>ventory stocks because of the<br />

high price uncerta<strong>in</strong>ty of the Indian market. Because<br />

Indian traders have monopolistic market<br />

power <strong>and</strong> can drive prices down, <strong>for</strong>ward contract<strong>in</strong>g<br />

with farmers is difficult s<strong>in</strong>ce exporters cannot<br />

assure farmers the contracted prices.<br />

Market Participants' Assessment of Opportunities<br />

<strong>and</strong> Constra<strong>in</strong>ts to Increas<strong>in</strong>g<br />

Competitiveness<br />

Trader <strong>in</strong>terviews, analysis of volumes traded, <strong>and</strong><br />

<strong>in</strong>ternational prices <strong>in</strong>dicate mixed prospects <strong>for</strong><br />

<strong>in</strong>creas<strong>in</strong>g the long-term competitiveness of African<br />

pigeonpea exports. Historically there has been a<br />

strong export market dem<strong>and</strong>, but this market is<br />

shr<strong>in</strong>k<strong>in</strong>g due to <strong>in</strong>creased competition from other<br />

exporters (notably Myanmar) <strong>and</strong> substitution of<br />

pigeonpea with yellow pea (exported by Canada).<br />

In the past five years, Myanmar has more than<br />

quadrupled exports to India, driv<strong>in</strong>g down wholesale<br />

prices (Table 6). There also has been a sharp<br />

<strong>in</strong>crease of compet<strong>in</strong>g yellow pea exports from Canada<br />

(Table 7). Because yellow peas have been used<br />

<strong>in</strong> the past as animal feed, they are be<strong>in</strong>g exported<br />

to India, the Middle East, <strong>and</strong> North Africa at extremely<br />

low prices. Because of. <strong>in</strong>creas<strong>in</strong>g price<br />

competition, the prospects <strong>for</strong> produc<strong>in</strong>g pigeon pea<br />

as a cash crop <strong>for</strong> the export market are dim<strong>in</strong>ish<strong>in</strong>g<br />

(Table 8). hldeed, Tanzania <strong>and</strong> Malawi have lost<br />

market share <strong>and</strong> farm gate prices have decl<strong>in</strong>ed<br />

compared to three years ago, when exports were<br />

<strong>in</strong>creas<strong>in</strong>g, production <strong>in</strong> India was poor, <strong>and</strong><br />

Myanmar was still not competitive (Table 9). Traders<br />

reported that opportunities exist <strong>for</strong> export<strong>in</strong>g to<br />

niche markets <strong>in</strong> Europe. But the volumes are small,<br />

about 1000 to 1500 t annually, <strong>and</strong> markets get<br />

Table 6. Myanmar Table 7. Annual exports of dry peas<br />

pigeonpea (I) exports to from Canada ('000 t), 1997·2001<br />

India, 1999·2001<br />

Canada to Asia<br />

1999 73,430 1997·98 395 <br />

2000 185,964 1998·99 700 <br />

2001 293,934 1999·00 638<br />

Source: Directorate of Economics 2000·01 850<br />

<strong>and</strong> Statistics. M<strong>in</strong>istry of<br />

Agriculture, India<br />

Source: Agriculture <strong>and</strong> Agri·Food Canada, FAO<br />

230<br />

<strong>Gra<strong>in</strong></strong> <strong>Legumes</strong> <strong>and</strong> <strong>Green</strong> <strong>Manures</strong> <strong>for</strong> <strong>Soil</strong> <strong>Fertility</strong> <strong>in</strong> Southern Africa