- Page 1 and 2:

Bouygues Construction Bouygues Immo

- Page 3 and 4:

Contents Interview with Martin Bouy

- Page 5 and 6:

A good year in 2011 Interview with

- Page 7 and 8:

The Group BOUYGUES • 2011 Registr

- Page 9 and 10:

Group profile strategy. Its two lar

- Page 11 and 12:

Flagship projects 1 2 3 4 5 BOUYGUE

- Page 13 and 14:

The Board of Directors at 28 Februa

- Page 15 and 16:

2011 key figures The Bouygues group

- Page 17 and 18:

caSh flow € million 3,244 e3,325

- Page 19 and 20:

Highlights Privée, included the re

- Page 21 and 22:

factS and fiGureS for 2011 (continu

- Page 23 and 24:

Highlights since 1 January 2012 aga

- Page 25 and 26:

Bouygues and its shareholders THE B

- Page 27 and 28:

Corporate, social and environmental

- Page 29 and 30:

Governance and dialogue with stakeh

- Page 31 and 32:

Respect "Our people are the most pr

- Page 33 and 34:

the work/perSonal life balance in G

- Page 35 and 36:

Trust "We believe in laying the gro

- Page 37 and 38:

headcount by reGion Scope: global H

- Page 39 and 40:

Fairness "All HR decisions in matte

- Page 41 and 42:

Gender equality Equal treatment of

- Page 43 and 44:

Investing in training "Within the G

- Page 45 and 46:

Low-carbon solutions The energy/car

- Page 47 and 48:

IMPROVING PRODUCTS AND SERVICES FOR

- Page 49 and 50:

GROUP-WIDE CSR ACTIONS Shared and G

- Page 51 and 52:

Sharing knowledge with BYpedia The

- Page 53 and 54:

Business activities and CSR BOUYGUE

- Page 55 and 56:

Full-service contractor Operating i

- Page 57 and 58:

Energy and services Bouygues Constr

- Page 59 and 60:

Performance Contract in Vitry-sur-S

- Page 61 and 62:

the Research & Development and Inno

- Page 63 and 64:

aims to make itself more attractive

- Page 65 and 66:

In all the countries where it opera

- Page 67 and 68:

CSR: challenges and key indicators

- Page 69 and 70:

Extra-financial indicators at 31 De

- Page 71 and 72:

France's leading property developer

- Page 73 and 74:

Hikari, the first positive-energy,

- Page 75 and 76:

RESIDENTIAL PROPERTY: BOUYGUES IMMO

- Page 77 and 78:

The other element is a highly perso

- Page 79 and 80:

For the Solid'R Community Day, empl

- Page 81 and 82:

dialogue wiTH sTaKeHolders - bouygu

- Page 83 and 84:

CSR: challenges and key indicators

- Page 85 and 86:

The world's leading roadbuilder Wit

- Page 87 and 88:

in some countries. Upstream, the gr

- Page 89 and 90:

in capital spending by local author

- Page 91 and 92:

Construction of the Port-Louis bypa

- Page 93 and 94:

Securing acceptance of production s

- Page 95 and 96:

vibration and working posture. Dust

- Page 97 and 98:

Colas is rehabilitating pathways in

- Page 99 and 100:

Extra-financial indicators at 31 De

- Page 101 and 102:

The leading private television grou

- Page 103 and 104:

TF1 has also created a broad range

- Page 105 and 106:

Net financial debt came to €40 mi

- Page 107 and 108:

Editorial staff mobilised The total

- Page 109 and 110:

Supplier commitment to the Responsi

- Page 111 and 112:

Extra-financial indicators at 31 De

- Page 113 and 114:

Mobile, fixed, TV and internet serv

- Page 115 and 116:

Bouygues Telecom's mobile phone net

- Page 117 and 118:

MVNOs accounted for 79% of new cust

- Page 119 and 120:

Optimised packaging for Bouygues Te

- Page 121 and 122:

SUPPORTING OUR PEOPLE Like other Gr

- Page 123 and 124:

Responsible site management Sustain

- Page 125 and 126:

CSR: challenges and key indicators

- Page 127 and 128:

Extra-financial indicators at 31 De

- Page 129 and 130:

Bouygues SA Key figures 2011 sales

- Page 131 and 132:

At the heart of sustainable develop

- Page 133 and 134:

Power transmission Orders worth €

- Page 135 and 136:

Risk factors BOUYGUES • 2011 Regi

- Page 137 and 138:

Risk factors Operational risks asso

- Page 139 and 140:

with good future prospects is fuell

- Page 141 and 142:

ased on reporting tools, serves to

- Page 143 and 144:

For several years, Colas has been c

- Page 145 and 146:

The current labour climate brings a

- Page 147 and 148:

in order to anticipate and neutrali

- Page 149 and 150:

Market value of hedging instruments

- Page 151 and 152:

Colas Île-de-France Normandie is c

- Page 153 and 154:

commitments in terms of broadcastin

- Page 155 and 156:

Mobile phone base stations > The ch

- Page 157 and 158:

Legal and financial information BOU

- Page 159 and 160:

Information on directors and non-vo

- Page 161 and 162:

François Bertière 3 boulevard Gal

- Page 163 and 164:

Patrick kron 3 avenue Malraux, 9230

- Page 165 and 166:

sandra noMBret 1 avenue Eugène Fre

- Page 167 and 168:

NON-VOTING DIRECTOR Michèle vilain

- Page 169 and 170:

Chairman’s report on corporate go

- Page 171 and 172:

Name Age a Accounts Committee Remun

- Page 173 and 174:

The Board will seek to increase the

- Page 175 and 176:

est or invest in a company, whether

- Page 177 and 178:

as well as forward transactions on

- Page 179 and 180:

of the company in charge of the fin

- Page 181 and 182:

12 • WORK OF THE BOARD AND ITS CO

- Page 183 and 184:

In case of internal fraud or miscon

- Page 185 and 186:

focus was on monitoring the action

- Page 187 and 188:

developing all processes and proced

- Page 189 and 190:

17.7 Information and communication

- Page 191 and 192:

Remuneration of corporate officers

- Page 193 and 194:

1.4 Table 3 - Directors’ fees The

- Page 195 and 196:

2 • 2011 REPORT ON STOCK OPTIONS

- Page 197 and 198:

2.2.1 Table 4 - Options granted to

- Page 199 and 200:

2.5 Stock options granted to or exe

- Page 201 and 202:

Significant changes in share owners

- Page 203 and 204:

3 • STOCK MARKET RULES AND PREVEN

- Page 205 and 206:

Share capital 1 • GENERAL INFORMA

- Page 207 and 208:

2 • FINANCIAL AUTHORISATIONS SUBM

- Page 209 and 210:

5.2 Description of the new share bu

- Page 211 and 212: Legal information 1 • GENERAL INF

- Page 213 and 214: Agreements entered into by Bouygues

- Page 215 and 216: Financial statements BOUYGUES • 2

- Page 217 and 218: Consolidated financial statements C

- Page 219 and 220: CHANGES IN CONSOLIDATED SHAREHOLDER

- Page 221 and 222: Notes to the consolidated financial

- Page 223 and 224: Network Operators (MVNOs). This aut

- Page 225 and 226: Subsequently, goodwill is carried a

- Page 227 and 228: Broadcasting rights are recognised

- Page 229 and 230: of rights (for external productions

- Page 231 and 232: Non-current provisions are not usua

- Page 233 and 234: 2.14 Cash flow statement The cash f

- Page 235 and 236: 3.2.2 Intangible assets 1,209 Devel

- Page 237 and 238: 3.2.4 Non-current financial assets

- Page 239 and 240: 3.2.4.2 Investments in non-consolid

- Page 241 and 242: 4.2 Advances and down-payments on o

- Page 243 and 244: NOTE 5 • CONSOLIDATED SHAREHOLDER

- Page 245 and 246: 6.2 Current provisions 831 Provisio

- Page 247 and 248: NOTE 8 • NON-CURRENT AND CURRENT

- Page 249 and 250: NOTE 9 • MAIN COMPONENTS OF CHANG

- Page 251 and 252: NOTE 12 • OPERATING PROFIT 1,857

- Page 253 and 254: NOTE 16 • SEGMENT INFORMATION Seg

- Page 255 and 256: 16.3 Analysis by geographical area

- Page 257 and 258: NOTE 17 • FINANCIAL INSTRUMENTS T

- Page 259 and 260: NOTE 18 • OFF BALANCE SHEET COMMI

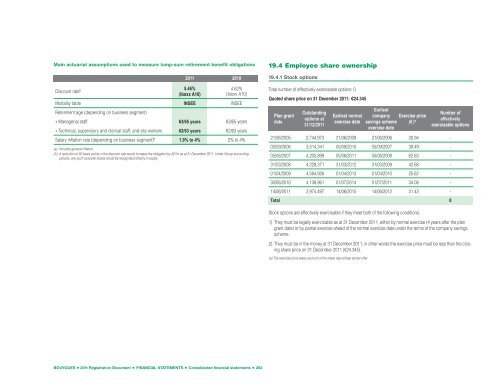

- Page 261: NOTE 19 • HEADCOUNT, EMPLOYEE BEN

- Page 265 and 266: NOTE 21 • ADDITIONAL CASH FLOW ST

- Page 267 and 268: NOTE 23 • PRINCIPAL EXCHANGE RATE

- Page 269 and 270: Proportionate consolidation Constru

- Page 271 and 272: INCOME STATEMENT - YEAR ENDED 31 DE

- Page 273 and 274: NOTE 1 • SIGNIFICANT EVENTS OF TH

- Page 275 and 276: NOTE 3 • NON-CURRENT ASSETS Balan

- Page 277 and 278: NOTE 11 • DETAILS OF AMOUNTS INVO

- Page 279 and 280: NOTE 18 • AVERAGE NUMBER OF EMPLO

- Page 281 and 282: Combined Annual General Meeting of

- Page 283 and 284: Agenda 1. ORDINARY GENERAL MEETING

- Page 285 and 286: Martin Bouygues was born on 3 May 1

- Page 287 and 288: BOARD OF DIRECTOR’S MANAGEMENT RE

- Page 289 and 290: AUDITORS’ REPORT ON THE CONSOLIDA

- Page 291 and 292: AUDITORS’ SPECIAL REPORT ON REGUL

- Page 293 and 294: SCDM may also supply Bouygues with

- Page 295 and 296: Agreements and commitments approved

- Page 297 and 298: Draft resolutions 1. ORDINARY GENER

- Page 299 and 300: 3. delegates to the Board of Direct

- Page 301 and 302: Glossary CONSTRUCTION 3E ® Aggrega

- Page 303 and 304: Rehagreen ® A service package crea

- Page 305 and 306: High-density area HSPA Interactivit

- Page 307 and 308: CSR According to the ISO 26000 stan

- Page 309 and 310: CSR and environmental indicators: n

- Page 311 and 312: Concordance Headings of Annex 1, EU

- Page 313 and 314:

FULL-YEAR FINANCIAL REVIEW The 2011

- Page 315 and 316:

STATEMENT BY THE PERSON RESPONSIBLE

- Page 317:

BOUYGUES GROUP Headquarters 32 aven