You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Parte I: Régimen general <strong><strong>de</strong>l</strong> <strong>Impuesto</strong> a <strong>la</strong> <strong>Renta</strong> <strong>de</strong> <strong>Empresas</strong><br />

artículo 37° menciona que serán <strong>de</strong>ducibles los intereses provenientes<br />

<strong>de</strong> en<strong>de</strong>udamientos <strong>de</strong> contribuyentes con partes vincu<strong>la</strong>das cuando<br />

dicho en<strong>de</strong>udamiento no exceda <strong><strong>de</strong>l</strong> resultado <strong>de</strong> aplicar el coeficiente<br />

que se <strong>de</strong>termine mediante <strong>de</strong>creto supremo sobre el patrimonio<br />

<strong><strong>de</strong>l</strong> contribuyente; los intereses que se obtengan por el exceso <strong>de</strong><br />

en<strong>de</strong>udamiento que resulte <strong>de</strong> <strong>la</strong> aplicación <strong><strong>de</strong>l</strong> coeficiente no serán<br />

<strong>de</strong>ducibles.<br />

A su vez, el artículo 21° en su numeral 6 <strong><strong>de</strong>l</strong> RLIR, hace referencia<br />

a los límites <strong>de</strong> en<strong>de</strong>udamiento entre empresas vincu<strong>la</strong>das,<br />

seña<strong>la</strong>ndo que el monto máximo <strong>de</strong> en<strong>de</strong>udamiento con sujetos<br />

o empresas vincu<strong>la</strong>das, a que se refiere el último párrafo <strong><strong>de</strong>l</strong><br />

inciso a) <strong><strong>de</strong>l</strong> artículo 37° <strong>de</strong> <strong>la</strong> LIR, se <strong>de</strong>terminará aplicando un<br />

coeficiente <strong>de</strong> 3 (tres) al patrimonio neto <strong><strong>de</strong>l</strong> contribuyente al<br />

cierre <strong><strong>de</strong>l</strong> ejercicio anterior.<br />

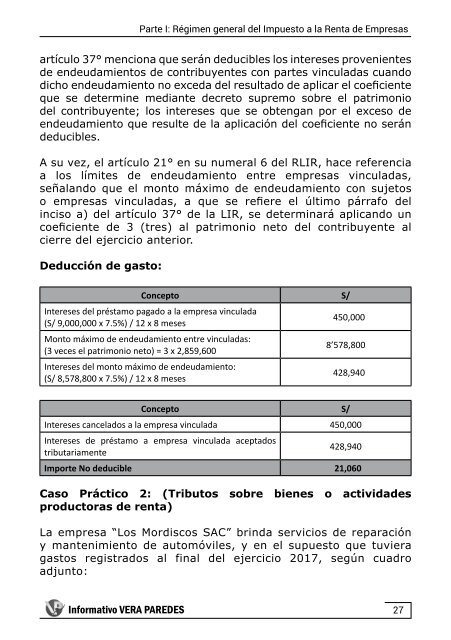

Deducción <strong>de</strong> gasto:<br />

Concepto S/<br />

Intereses <strong><strong>de</strong>l</strong> préstamo pagado a <strong>la</strong> empresa vincu<strong>la</strong>da<br />

(S/ 9,000,000 x 7.5%) / 12 x 8 meses<br />

450,000<br />

Monto máximo <strong>de</strong> en<strong>de</strong>udamiento entre vincu<strong>la</strong>das:<br />

(3 veces el patrimonio neto) = 3 x 2,859,600<br />

8’578,800<br />

Intereses <strong><strong>de</strong>l</strong> monto máximo <strong>de</strong> en<strong>de</strong>udamiento:<br />

(S/ 8,578,800 x 7.5%) / 12 x 8 meses<br />

428,940<br />

Concepto S/<br />

Intereses cance<strong>la</strong>dos a <strong>la</strong> empresa vincu<strong>la</strong>da 450,000<br />

Intereses <strong>de</strong> préstamo a empresa vincu<strong>la</strong>da aceptados<br />

tributariamente<br />

428,940<br />

Importe No <strong>de</strong>ducible 21,060<br />

Caso Práctico 2: (Tributos sobre bienes o activida<strong>de</strong>s<br />

productoras <strong>de</strong> renta)<br />

La empresa “Los Mordiscos SAC” brinda servicios <strong>de</strong> reparación<br />

y mantenimiento <strong>de</strong> automóviles, y en el supuesto que tuviera<br />

gastos registrados al final <strong><strong>de</strong>l</strong> ejercicio <strong>2017</strong>, según cuadro<br />

adjunto:<br />

Informativo VERA PAREDES<br />

27