You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Parte II: Régimen Especial<br />

PARTE II: RÉGIMEN ESPECIAL<br />

1. ASPECTOS GENERALES<br />

1.1 Concepto <strong><strong>de</strong>l</strong> Régimen Especial<br />

El Régimen Especial <strong><strong>de</strong>l</strong> <strong>Impuesto</strong> a <strong>la</strong> <strong>Renta</strong> (RER) es un régimen<br />

tributario dirigido a personas naturales y jurídicas, socieda<strong>de</strong>s<br />

conyugales y sucesiones indivisas domiciliadas en el país que<br />

obtengan rentas <strong>de</strong> tercera categoría, es <strong>de</strong>cir rentas <strong>de</strong> naturaleza<br />

empresarial o <strong>de</strong> negocio.<br />

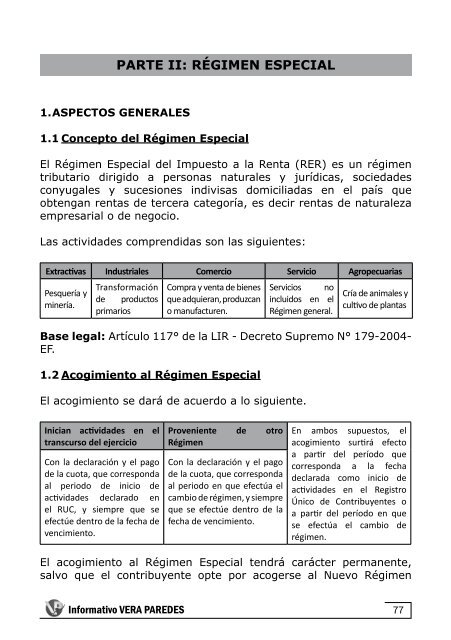

Las activida<strong>de</strong>s comprendidas son <strong>la</strong>s siguientes:<br />

Extractivas Industriales Comercio Servicio Agropecuarias<br />

Transformación Compra y venta <strong>de</strong> bienes Servicios no<br />

Pesquería y<br />

Cría <strong>de</strong> animales y<br />

<strong>de</strong> productos que adquieran, produzcan incluidos en el<br />

minería.<br />

cultivo <strong>de</strong> p<strong>la</strong>ntas<br />

primarios o manufacturen. Régimen general.<br />

Base legal: Artículo 117° <strong>de</strong> <strong>la</strong> LIR - Decreto Supremo N° 179-2004-<br />

EF.<br />

1.2 Acogimiento al Régimen Especial<br />

El acogimiento se dará <strong>de</strong> acuerdo a lo siguiente.<br />

Inician activida<strong>de</strong>s en el<br />

transcurso <strong><strong>de</strong>l</strong> ejercicio<br />

Con <strong>la</strong> <strong>de</strong>c<strong>la</strong>ración y el pago<br />

<strong>de</strong> <strong>la</strong> cuota, que corresponda<br />

al periodo <strong>de</strong> inicio <strong>de</strong><br />

activida<strong>de</strong>s <strong>de</strong>c<strong>la</strong>rado en<br />

el RUC, y siempre que se<br />

efectúe <strong>de</strong>ntro <strong>de</strong> <strong>la</strong> fecha <strong>de</strong><br />

vencimiento.<br />

Proveniente <strong>de</strong> otro<br />

Régimen<br />

Con <strong>la</strong> <strong>de</strong>c<strong>la</strong>ración y el pago<br />

<strong>de</strong> <strong>la</strong> cuota, que corresponda<br />

al periodo en que efectúa el<br />

cambio <strong>de</strong> régimen, y siempre<br />

que se efectúe <strong>de</strong>ntro <strong>de</strong> <strong>la</strong><br />

fecha <strong>de</strong> vencimiento.<br />

En ambos supuestos, el<br />

acogimiento surtirá efecto<br />

a partir <strong><strong>de</strong>l</strong> período que<br />

corresponda a <strong>la</strong> fecha<br />

<strong>de</strong>c<strong>la</strong>rada como inicio <strong>de</strong><br />

activida<strong>de</strong>s en el Registro<br />

Único <strong>de</strong> Contribuyentes o<br />

a partir <strong><strong>de</strong>l</strong> período en que<br />

se efectúa el cambio <strong>de</strong><br />

régimen.<br />

El acogimiento al Régimen Especial tendrá carácter permanente,<br />

salvo que el contribuyente opte por acogerse al Nuevo Régimen<br />

Informativo VERA PAREDES<br />

77